This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Before leaving for his three-nation tour to China, Mongolia and South Korea from May 14, Prime Minister Mr. Narendra Modi will launch three of his government’s social security schemes on Saturday – Pradhan Mantri Jeevan Jyoti Bima Yojana (Life Insurance), Pradhan Mantri Suraksha Bima Yojana (Accidental Death & Disability Insurance) and Atal Pension Yojana (Pension Scheme).

These schemes would be an extension to Pradhan Mantri Jan-Dhan Yojana (PMJDY) and would be covered under the government’s Jan Suraksha initiative. These schemes are designed to be pro poor and promise to provide protection against the risks of dying too early (Pradhan Mantri Jeevan Jyoti Bima Yojana) or living too long (Atal Pension Yojana) or unable to work & earn due to partial or full disability (Pradhan Mantri Suraksha Bima Yojana).

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Age of the Insured – Bank account holders aged between 18 and 50 years are eligible to apply for this scheme. So, if you are aged more than 50 years, you are not eligible to enroll yourself for this scheme. But, once enrolled, you can continue with this scheme till you attain the age of 55 years.

Premium Amount – Less than Re. 1 a day or an annual premium of Rs. 330 is what you need to pay to get a life cover of Rs. 2 lacs. No matter what your age is, the premium is fixed at Rs. 330 for a life cover of Rs. 2 lacs. This annual premium of Rs. 330 has been fixed for the first three years from June 1, 2015 to May 31, 2018, after which it will again be reviewed based on the insurers’ annual claims experience.

Period of Insurance – June 1st, 2015 to May 31st, 2016 is the period for which this scheme will cover all kind of risks to your life in the first year of operation. Next year onwards as well, the risk cover period will remain June 1 to May 31.

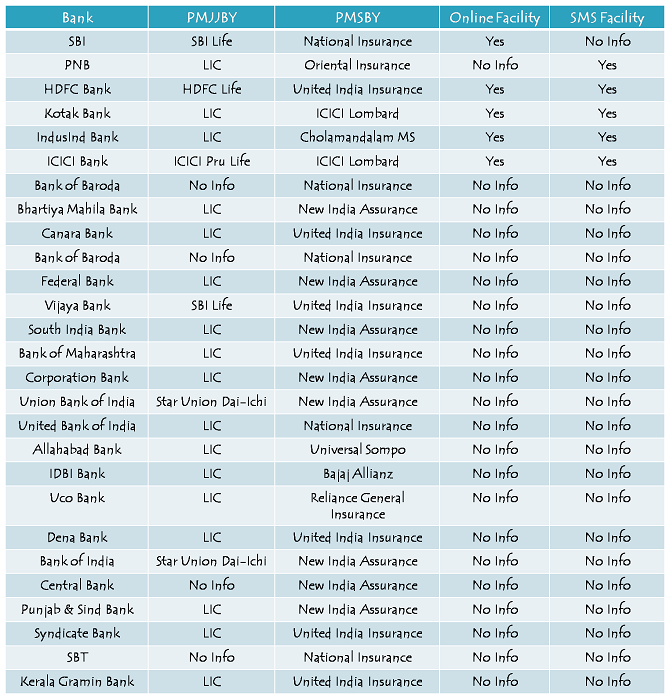

LIC as the Administrator – The scheme would be offered / administered by the Life Insurance Corporation (LIC) and other life insurance companies like SBI, ICICI etc. through their tie ups with the interested banks like SBI, ICICI, Canara Bank etc. Participating banks are free to engage any such life insurance company for implementing this scheme for their subscribers.

Auto Debit Facility – Annual premium of Rs. 330 will get deducted from your savings bank account through auto debit facility. You will have to give your consent for auto debit of premium from any one of your bank accounts at the time of enrolling for this scheme.

Last Date for Enrolment – May 31, 2015 is the last date for getting enrolled for this scheme, but the government has given an extension of three months up to August 31, 2015 for us to get enrolled and give auto-debit consent for this scheme. This enrolment period may be extended by the government for another period of three months, up to November 30, 2015.

Those joining this scheme subsequent to May 31, 2015 will have to pay the full year’s premium of Rs. 330 and submit a self-certificate of good health in the prescribed proforma.

Toll-Free Numbers – 1800 110 001 / 1800 180 1111 – These two are the National Toll-Free Numbers for this scheme. You can check the state-wise toll-free numbers from this link – State-Wise Toll Free Numbers

Service Tax Exempt – Finance Minister Mr. Arun Jaitley has proposed to exempt this scheme from service tax. So, you will not be charged any service tax on the premium payable.

Know Your Customer (KYC) – Aadhaar Card issued by the UIDAI will be the primary requirement for your KYC under this scheme.

Application Form – Here you have the link to the application form for you to enroll yourself for this scheme – Application Form for PMJJBY

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

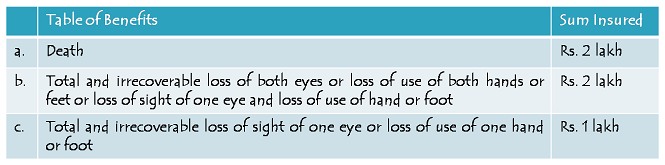

Policy Coverage – The scheme offers to provide you or your family a cover of up to Rs. 2 lacs in case of any mishappening, resulting into death or disability of the insured. In case of death or full disability, you or your family will get Rs. 2 lacs and in case of partial disability, you will get Rs. 1 lac. Full disability means loss of both eyes or both legs or both hands, whereas partial disability means loss of one eye or one leg or one hand.

Age of the Insured – Savings bank account holders aged between 18 years and 70 years are eligible to apply for this scheme. People aged more than 70 years will not be able to get the benefits of this scheme.

Premium Amount – It costs you just Rs. 12 in annual premium for having an accidental death or disability cover of Rs. 2 lacs under this scheme. It works out to be just Re. 1 a month, which is extraordinarily low. Again, your age has nothing to do with the premium payable for your insurance cover under this scheme as the premium is fixed at Rs. 12 for a cover of Rs. 2 lacs.

Period of Insurance – You will remain insured for a period of one year from June 1, 2015 to May 31, 2016. Next year onwards as well, the risk cover period will remain to be June 1 to May 31.

Administrators for PMSBY – The scheme would be offered / administered by many of the general insurance companies, both in the public sector as well as in the private sector. Participating banks will be free to engage any such general insurance company for implementing the scheme for their subscribers. National Insurance Company Limited, Oriental Insurance Company Limited and ICICI Lombard are some of the companies which would be offering this scheme.

Auto Debit Facility – You will be required to provide your consent for auto debit of Rs. 12 as the annual premium from any one of your bank accounts at the time of enrolling for this scheme. This premium of Rs. 12 will get deducted from your savings bank account through auto debit facility every year between May 25 and June 1.

Last Date for Enrolment – May 31, 2015 is the last date for getting enrolled for this scheme, but the government has given an extension of three months up to August 31, 2015 for us to get enrolled and give auto-debit consent for this scheme. This enrolment period may be extended by the government for another period of three months, up to November 30, 2015.

Those joining this scheme subsequent to May 31, 2015 will have to pay the full year’s premium of Rs. 12 and agree to specified terms of this scheme.

Toll-Free Numbers – 1800 110 001 / 1800 180 1111 – These two are the National Toll-Free Numbers for this scheme. You can check the state-wise toll-free numbers from this link – State-Wise Toll Free Numbers

Service Tax Exempt – Yes, Finance Minister Mr. Arun Jaitley has proposed to exempt this scheme from service tax. So, you will not be charged any service tax on the premium payable.

Know Your Customer (KYC) – Aadhaar Card issued by the UIDAI will be the primary requirement for your KYC under this scheme.

Application Form – Here you have the link to the application form for you to enroll yourself for this scheme – Application Form for PMSBY

Should you subscribe to Pradhan Mantri Jeevan Jyoti Bima Yojana?

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is a term life insurance scheme and we all know that a term plan is the cheapest form of covering ourselves against the risks of untimely death. I think the government is doing a wonderful job in taking the initiative to attract low income group people to get themselves covered against the risks of untimely death.

I think the premium is reasonably justified for people in their middle years, probably between the age of 40-50 years. For younger people, you might still find cheaper life cover policies with some of the private insurers, like Max, Aviva, Aegon Religare etc.

I’ll keep on updating this post as and when I have some interesting data to insert into. If any of you has anything to share about this scheme, please feel free to do that, I’ll update that as well here in the post.

I covered Atal Pension Yojana in March this year and I have covered Pradhan Mantri Jeevan Jyoti Bima Yojana in this post. I will cover Pradhan Mantri Suraksha Bima Yojana also as soon as possible.

Application Form for PMJJBY

{kind=link}

{kind=link}