This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

First of all, we wish all the readers of OneMint a very Happy & Prosperous New Year !! May God give you success in your work and peace in your life and 2016 turns out to be the best year in your life !!! 🙂

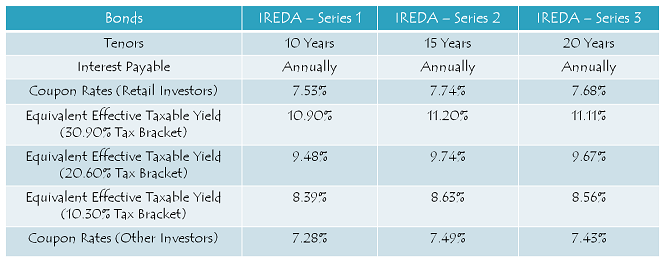

IREDA 7.74% Tax-Free Bonds

Hunger without food is bad for health, so is overeating. Investors were hungry for tax-free bonds, especially a big issue to satisfy their demand, like the NHAI one. But, when such an issue came, they were not able to have full of it. It only got subscribed by 0.86 times in the retail investors category.

Such a big supply or say shortage of demand resulted in poor listing for the IRFC bonds. Investors were expecting some healthy listing gains with IRFC bonds after it received a good response and big oversubscription on the first day itself. But, that did not materialise, probably because NHAI offered slightly higher rate of interest or probably many investors subscribed to IRFC bonds to get its listing gains only.

As the NHAI issue got closed on the last day of 2015, IREDA announced slightly higher rate of interest for its issue which is getting launched on Friday next week i.e. January 8th. It will offer a maximum of 7.74% coupon rate for a period of 15 years, which is 0.14% higher than NHAI’s 7.60%. But, at the same time, this issue is AA+ rated, so it can carry a slightly higher rate of interest.

The issue is officially scheduled to close on January 22, but I think it should get fully subscribed much before than that.

Before we analyse it further, let us first quickly check the salient features of this issue:

Size of the Issue – IREDA is authorized to raise Rs. 2,000 crore from tax free bonds this financial year, out of which the company has already raised Rs. 284 crore by issuing these bonds through a private placement. The company will try to raise the remaining Rs. 1,716 crore in this issue.

Rating of the Issue – ICRA and India Ratings have assigned ‘AA+’ rating to the issue, thus suggesting that these bonds carry very low credit risk and high degree of safety regarding timely payment of financial obligations. As all the previous issues were rated ‘AAA’, this is the first issue this financial year which is rated AA+.

Moreover, these bonds are ‘Secured’ in nature i.e. in case of any default, the bondholders would carry a right to make claim on certain assets of the company.

Coupon Rates on Offer – As this issue is rated AA+, it can offer interest rates which are 10 basis points (or 0.10%) higher than the rates which a AAA-rated issue could have offered. While NHAI 15-year option carried 7.60% rate of interest, IREDA is offering 7.74% for the same duration. For 10-year period, IREDA issue will have 7.53% rate of interest as against 7.39% which NHAI was offering.

As the NHAI issue did not offer 20-year investment period, IREDA offer will be attractive for the long-term institutional investors like insurance companies or pension funds. For 20-year period, IREDA is offering 7.68% to the retail investors and 7.43% for the non-retail investors.

For the non-retail investors, these rates would be lower by 25 basis points (or 0.25%).

NRI/QFI Investment NOT Allowed – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 20% of the issue is reserved i.e. Rs. 343.20 crore

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved i.e. Rs. 343.20 crore

Category III – High Net Worth Individuals including HUFs – 20% of the issue is reserved i.e. Rs. 343.20 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 686.4 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing & Allotment – IREDA has decided to get these bonds listed only on the Bombay Stock Exchange (BSE). The company will allot the bonds and get them listed within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – It is not mandatory to have a demat account to apply for these bonds. Investors have the option to subscribe to these bonds in physical form as well. Whether you apply for these bonds in demat or physical form, the interest payment will still get credited to your bank account through ECS.

Also, even if you get these bonds allotted in your demat account, you have the option to rematerialize your holding in physical/certificate form if you decide to close your demat account in future.

No Lock-In Period – These tax-free bonds are freely tradable and do not carry any lock-in period. The investors may sell them at the market price whenever they want after these bonds get listed on the stock exchanges within 12 working days of the closing date.

Interest on Application Money & Refund – Successful allottees will earn interest at the applicable coupon rates i.e. 7.53% p.a. for 10 years and 7.74% p.a. for 15 years and 7.68% p.a. for 20 years on their application money, from the date of realization of application money up to one day prior to the date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of face value Rs. 1,000 each. There is no upper limit for the investors to invest in this issue. However, an investor investing more than Rs. 10 lakhs will be categorized as a high networth individual (HNI) and will get a lower rate of interest as applicable.

Interest Payment Date – IREDA will make its first interest payment exactly one year after the date of allotment and the date of allotment will be announced just before the listing date. I will update this post as and when it gets announced.

Record Date – For the payment of interest or the maturity amount, record date will be fixed 15 days prior to the date on which such amount is due to be payable.

Should you invest in this issue?

IREDA (Indian Renewable Energy Development Agency), 100% owned by the Government of India, was established in 1987 to promote, develop and extend financial assistance for renewable energy and energy efficiency/conservation projects. As the company has strategic importance in the development of the renewable energy sector, certain special privileges have been provided to the company:

* Regular capital infusion in the company by the Government,

* Sovereign guarantee to the lenders against approximately 58% of IREDA’s total borrowings,

* Rs. 300 crore allocation from the National Clean Energy Fund (NCEF),

* Access to cheaper sources of funding, like these tax-free bonds etc.

Reasons for a lower Credit Rating as ‘AA+’ – Many investors want to know why this issue has been rated ‘AA+’ this time around when last time in February 2014, IREDA issued these bonds and the issue was assigned ‘AAA’ rating by the credit rating agencies. Investors also need to decide whether they should invest in this issue with a higher rate of interest being a AA+ rated issue or wait for HUDCO to announce its interest rates and then take a decision.

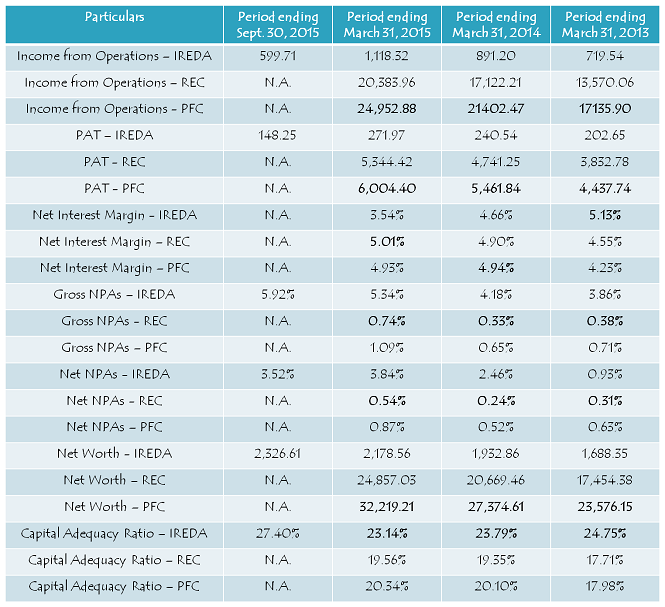

So, as the HUDCO interest rates are yet to get announced and we also don’t know when exactly the issue will be launched, it is difficult to guesstimate its interest rates. That is why I can talk only about this issue at this point in time. As far as the rating is concerned, I think higher NPAs and lower yield on its lending portfolio resulting in a fall in the company’s net interest margins (NIMs) are the two primary reasons for its rating downgrade from AAA to AA+.

IREDA was doing well in terms of managing its asset quality a couple of years back. Its Gross NPAs improved from 19.9% in 2007 to 3.86% in 2013. But, in recent times, its financials have taken a hit and its Gross NPAs have again increased to 5.34% by March 31, 2015 and 5.92% by September 30, 2015.

IREDA vs. REC vs. PFC

(Note: Figures are in Rs. Crore, except figures in %)

Moreover, as per ICRA, lending only to the renewable energy sector, low net worth of the company as compared to some of the bigger players in the power financing business and higher NPAs in the small hydro, cogen and biomass segment are a few other reasons for a lower rating.

However, as IREDA is 100% owned and backed by the Government of India and as the government is committed to encourage the use and development of renewable sources of energy, I think the company should be able to improve its financials going forward. Its capital adequacy ratio (CAR) is quite comfortable at 27.40% on September 30, 2015 and its debt-to-equity ratio is expected to be 3.93% after this issue gets completed. IREDA also plans to go public in the next 2-3 years.

Personally, I am quite comfortable investing in this issue as I think IREDA should be able to improve its balance sheet going forward and the government backing will always be there for a company financing the renewable energy space. However, conservative investors, who need to invest only Rs. 10 lakh or less in these tax-free bonds, should wait for the HUDCO issue or NHAI Tranche II.

Application Form for IREDA Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IREDA tax-free bonds, you can contact me at +919811797407

Hi Shiv,

I bought IRFC (10 yrs – 7.32%) and NHAI bonds( 15 yrs – 7.6%) couple of weeks back.

1) Are these bonds listed in NSE or BSE? Can I sell these bonds in both NSE and BSE?

2) Is there are BSE id or NSE id for these 2 bonds? Can u pls share if any?

3) Is there any website or link to check what TFB bonds & how much volume are traded on daily basis.

4) If there are no buyers in trading, can i break these bonds with any penalty?

5) Can I avail loan facility after couple of years like PPF?

Hi Raja,

1. Both, IRFC bonds and NHAI bonds, are listed on the NSE as well as BSE. You can sell your bonds on both the stock exchanges.

2. You can the Bid IDs of both these issues from their respective posts – IRFC – http://www.onemint.com/2015/12/05/irfc-7-53-tax-free-bonds-december-2015-issue/

NHAI – http://www.onemint.com/2015/12/14/nhai-7-60-tax-free-bonds-tranche-i-december-2015-issue/

3. Here is the link for all the bonds traded on the NSE – http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

4. No, you cannot redeem these bonds back to the issuer before maturity.

5. Yes, you can use these bonds as collateral for taking loan/overdraft facility.

Sir, Could you guide us how to read and understand bonds trading on the NSE ..thanks

Hi P.S.,

Can you pick any one of these bonds and let me know what all you need to understand.?

Hi Shiv,

I bought IRFC (10 yrs – 7.32%) and NHAI bonds( 15 yrs – 7.6%) couple of weeks back.

1) Are these bonds listed in NSE or BSE? Can I sell these bonds in both NSE and BSE?

2) Is there are BSE id or NSE id for these 2 bonds? Can u pls share if any?

3) Is there any website or link to check what TFB bonds & how much volume are traded on daily basis.

4) If there are no buyers for my TFB in trading, Can i break this long term bond with any penalty

5) Can I avail loan facility on my TFB after couple of years?

It is wrong to say that Film stars are rich. There are so many people in films who were rich but now living in penury just because they did not save and planned their life after films. I would say that they have taken correct financial decision in TFB rather then buying cars or investing in property bubble. TFB are win-win situation for everybody- Govt PSU’s and investing public.

I am happy that You recognize this fact. There are so many avenues where this HNI invests. Some are investing directly in some companies and some in startups etc. Middle class is the only one looking at FD, NSC, PPF, Equity, MF , TF bonds etc taking some risk. Many who invested in stocks will find that there net worth is 50% after investing for last 6 months. So it is important that Govt opens up more avenues for investments with a win-win situation like TFB,Gold monetization etc. I do not care which Govt is in power, these are innovative ways to bring idle money into nation building. Paying TF interest to Film stars is no way taking from poor and giving to rich.If some one puts up comments critisizing ET view many a times they do not publish it. I am afraid if we have narrow thinking like this country will develop.

George, you have so brilliantly articulated the views of retail investors. When I read this article today, I immediately thought of Shiv and wished that the guy who had written this story had read Shiv’s blog and realised how small investors like us are so interested in tax free bonds.

Blocking one’s money for 10,15 and even 20 years should be regarded as a great service to the nation. Return of about 7.5% means a lot only to small investors. Let us also not think that investment in these bonds for a period of 15 to 20 years is without risk.

Vin

Hi Shiv,

I heard today that HUDCO Issue is opening on 23 January, but I could not find any reference to it in any newspaper. Have you heard anything.

Vin

Hi Vin,

23rd January is Saturday and it is not possible for an issue to open on a Saturday. So, 23rd Jan is ruled out. But, one of my sources has informed me that it could possibly open from 27th January. However, there is no confirmation about it.

Shiv, I strongly feel that 27th will be the start date. Last article in Economic times on TF bonds is very misleading. It suggests that these bonds help rich people quoting that Film stars are buying. After all film stars are also tax paying citizens and they will also have bad times when money is required. More over ET instead of highlighting how this money can be used for nation development are only focusing on how individuals and organizations are benefited in getting tax free income. After all nothing is free, it comes with some risk taking. Long term commitment to a fixed interest. Where as these idle money which would have been invested in gold or other assets are getting diverted to nation building. Infrastructure development is for whole citizens. After all the tax payers are paying tax and in a country like India they get very little benefits. If some one earns 20 Lakhs per annum and suddenly finds no job and income, he will have to live on his savings if he has done. Absolutely no social security unlike developed countries, where citizen gets benefits at the time of retirement or out of jobs.

I agree with you, George. In fact media should be neutral when reporting something. They should not take their own decision\opinion\judgement on any issues.

Even draft/shelf prospectus isnt filed yet, so how can it be possible this month?

Draft Shelf Prospectus got filed in October. HUDCO now needs to file its final prospectus and launch the issue.

I was searching for it at below link. May be its not the right place to look for then?

http://www.sebi.gov.in/sebiweb/home/list/3/17/38/0/Draft-filed-with-SE

dear shiv ytm of 901hudco34 is shown as 7.52 at this link —–http://www.bseindia.com/markets/debt/debt_corporate_EOD.aspx?curPage=1&expandable=0 and it is shown as 7.66 at this link—-http://www.bseindia.com/NewStockReach/StockReach_Debt.aspx?scripcode=961816

what could be the reason for this difference.i used online ytm calculators and both the yields are being shown by different calculators.which one is correct?should it be calculated using excel spreadsheet?

Hi Dr. Puneet,

These exchange calculators are not reliable, you should do your own calculations using excel spreadsheet.

dear shiv

i used excel(XIRR) and found that both the yields are correct .one assumes that interest received is reinvested at 9.01% and other assumes it to be reinvested at 7.65%.since chances of reinvesting at 9.01 is unlikely in the future so assuming it to be reinvested at current yield is a better option.(being a doctor it was very hard for me to calculate it).

so the correct yield would be 7.52 and not 7.65

YTM calculation assumes that the interest amount gets reinvested at the YTM itself.

thanks a lot for your guidance.

You are welcome Dr. Puneet!

Shiv

With markets crashed will bond yield go up? I am really glad to have followed this blog else I would never have invested in bonds .

Can we expect some post by Manshu or you on alternatives for investors in present situation? Thanks

Hi Harinee,

An economic slowdown results in a fall in bond yield, but a panic results in yield moving higher. So, you need to decide if there is a slowdown or a panic in the markets right now. I’ll ask Manshu if he can do a post on alternate investment options in this market scenario.

Dear Shiv,

Thank you for responding. PFC

Bond Certificate has not arrived so far, hence there is no chance of it going back. In the allotment letter itself they had indicated that it would be issued in March’16.

Any thoughts?

Thank you.

In that case, it really depends on Big Share Services whether they will accept your request for directly crediting your bonds to your demat account or not. You need to take this matter to Big Share itself, only they can clarify it for you. If they do it for you, it will be of mutual benefit.

Dear Mr. Shiv,

There is no response from the numbers given by you for ‘Big Share’.

You may remember my case:

Refer PFC Tax Free Bonds of 5.10.2015. I had applied for Bonds in Physical Mode, since my demat account was under process. However, subsequently, my NEW DEMAT ACCOUNT has been opened recently and I wish that my Tax Free Bonds be DIRECTLY CREDITED to my New Demat Account, instead of sending them in physical mode.

I had submitted all details of my application form and my complete new Demat Account details. Despite this there has been no response from them. Kindly assist please and oblige.

Thank you.

Hi S.K.,

I think only Big Share Services will be able to assist you regarding this. They will first check the status of your bond certificate. If they have received it back, then they will send it back to you first and then you’ll have to send a fresh request through your broker to get it dematerialised. If they have not received your certificate back, then you’ll have to provide them the indemnity bond to reissue the certificate. It really depends on Big Share Services how cooperative they are in such cases.

Shiv, do you know when the IREDA issue was closed. Wants to calculate the allotment and refund.

It got closed on Monday George.

In which case we can expect the refund and allocation by 20th. Hope HUDCO issue starts only after that since we will have at least 1 week lead time from announcement.

Let’s see when HUDCO decides to launch its issue, we have been waiting since September-October for the same.

Looks like Hudco will also offer 7.7%. The Gilt coupon is up.

IRFC and NHAI are still trading at 1001-1003 level. Hope to have HUDCO announcement this week.

Mr Shiv,

If I apply TFBs under Category III but the allotment does not exceed Rs. 10 lakhs in the issue across all series) then, will I be eligible for receiving interest at the higher rate, which is applicable for Category IV investors?

Can retail investors buy the TFBs, which are traded under other category /non-retail category in the secondary market? If yes and total holding across all series does not exceed Rs. 10 lakhs, then what will be the applicable interest rate (retail OR non-retail)?

I also take this opportunity to Thank you for all your efforts in making this blog as most interactive and informative.

Thanks Shubh for your kind & motivating words!

1. You’ll get a lower rate of interest applicable to Category III investors if you apply for these bonds under Category III & allotment you get is below Rs. 10 lakh.

2. Yes, retail investors can buy non-retail bonds in the secondary markets. But, they will get a lower rate of interest if they buy these non-retail bonds.

Yes, REC in your post you have mentioned the interest will be paid on 28th Dec for the first year. That clarifies.

🙂

I am bit surprised to get interest for the REC 7.43 bond for the period 5/11/2015 to 27/12/2015. I thought the interest payment is supposed to be on 01st Dec every year.

nice post

Thanks Ashish!

Thanks a lot for your immediate response.

Is it a fair idea to buy TFB before few days/weeks of interest payment date to reap the benefits of full year interest. I understand that most of them sell their bonds after interest payment date, but atleast few tend to sell TFB few weeks before the interest date due to their personal needs.

Hi Raja,

I don’t think there is a scope of good gains in such an opportunity (buying/selling it just before the ex-interest date). I think it is better to apply for these bonds from the company itself during these public offerings, rather than paying additional 0.5-1% brokerage for buying it from the secondary markets.

Hi Sir,

I have the below list of questions which will be useful for my future planning.

1) When will we get the 5% interest for un allotted amount in TFB. On Dec 8, i purchased IRFC bonds, but only un allocated amount is credited, so wondering when will i get the interest?

2) If I have TFB in my account for 9 months and for some reason I couldnt hold it for 12 months and i sell it on 10th month, will i get any partial interest?

3) I know there is flat 10% interest rate If i sell TFB after one year irrespective of tax slab, will there be any indexation benefits If I hold bonds for more than 3 years

4) If I buy/sell TFB in demat account, i know 0.25 to 1% will be charged as brokerage. Does this means If I buy/sell bonds for 1 Lakh, around

Rs.250/- to Rs.1000/ will be charged.

5) IF I buy TFB in demat account, how long it takes to reflect in my demat account?

Hi Raja,

1. Interest amount must have got credited in your bank account for the allotted bonds as well as refund amount. Please check your bank account once again. If it is not there, you need to contact the Registrar.

2. You will not get any interest if you sell your bonds in the 10th month or before the “Ex-Interest Date”. Ex-interest date falls a couple of days before the Record Date.

3. There is no indexation benefit with the listed bonds.

4. Yes, that’s correct.

5. It takes 2-3 days for the bonds to get credited.

Hi Shiv, what % allocation can one expect in retail category if applied on day 1 (i.e. 8th Jan) of this issue?

Thx!

Hi SG,

Around 55% allotment will happen in the retail category if applied on Day 1.

Dear Sir,

I need a small clarification. How does this “first come first served” basis work? Does it not mean that applications are accepted only upto the available number of bonds on offer and the rest are rejected? Kindly enlighten. Thank you

Hi Satish,

As there is an electronic system of bidding, it is very difficult to accept/reject applications on a time entry basis. So, the exchanges make proportionate allotment to all those applications which get submitted on the day the issue gets oversubscribed. Applications which get submitted before that day get 100% allotment. First come first served basis work on a day-by-day basis. In IREDA’s case, as the retail portion has got oversubscribed on the very first day, all successful applicants will get proportionate allotment of approximately 55%.

Thank you Sir.

You are welcome Satish!

Sir, how did you came to know that if ever we are alloted it would be 55% allotment on FCFB?

Hi Sandhya,

Retail subscription of 1.84 times makes it 55% available for each applicant.

Day 1 (January 8) subscription figures:

Category I – Rs. 2,096 crore as against Rs. 343.20 crore reserved – 6.11 times

Category II – Rs. 1,032.40 crore as against Rs. 343.20 crore reserved – 3.01 times

Category III – Rs. 701.54 crore as against Rs. 343.20 crore reserved – 2.04 times

Category IV – Rs. 1,262.12 crore as against Rs. 686.40 crore reserved – 1.84 times

Total Subscription – Rs. 5,092.05 crore as against total issue size of Rs. 1,716 crore – 2.97 times

This issue is over now. Now, only two issues left – HUDCO & NHAI Tranche II.

What is the size of hudco and nhai tranche 2

HUDCO issue size should be of Rs. 3,711.50 crore and NHAI is allowed to raise an additional Rs. 10,128 crore this financial year.

Thanks sir. Hope we get better allotment on these at least.

When are these issues expected?

HUDCO issue can get announced any time this month and NHAI issue should come in February or March.

Now, waiting for – HUDCO & NHAI Tranche II.

Shiv ji do update about this as early as possible..thanks

Sure P.S., I’ll do that as soon as I have any info about it.

Hi Shiv,

Can you let us know today’s subscription figures and the possible allotment ratio for retail investors.

Thanks in advance.

Regards,

Soumya

Hi SB,

Retail investors will get approximately 55% allotment.

Nothing surprising in retail getting oversubscribed considering that the issue gave best coupon rate so far and retail investor is not much concerned about rating of AAA or AA+. Any way , the issue gave an opportunity for some of them to buy the other issues at a relatively lower price from secondary market. IRFC was still trading on par. I used the opportunity buy few on top of my allotment. Even NTPC was priced reasonable in last few days. We can expect a jump in secondary market for all this recent listed bonds considering the over subscription and only 2 issues left. I am sure HUDCO will not be providing better coupon rate based on current level of Gsec bonds. NHAI will likely issue second trache only by Feb end or Mar beginning.

NHAI Trache -1 will give some small margin in opening sale.

I agree George!

Will there be brokerage if bought in secondary market? If so, how much typically? as that should be added to bond price for net gain.

Yes Chaitanya, brokerage will have to be paid while buying these bonds in the secondary markets. Brokerage varies anywhere between 0.25% to 1% odd.