This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Stock markets have turned turbulent again. Every morning I turn on a business channel these days, I see a large number of red ticks and only a few green ticks. Markets have fallen back to the May 2014 levels when Modi government was voted to the power with high hopes of turning things around. While I think the government is working very hard to get things in order, things are taking a very long time to get back on track.

While analysts are pointing fingers towards China, Fed rate hike and tumbling crude oil prices, I think they are taking classes from Kejriwal i.e. blaming others for anything & everything, but not checking what is wrong within. I think Indian markets are not falling only because of China scare, but because the investors have lost hopes of any corporate earnings revival in the foreseeable future.

Moreover, sentiment has also turned negative with respect to the pace of reforms and policy actions. For this, I would like to thank the Congress leadership, for the role they have played in disrupting two consecutive sessions of parliament and blocking passage of some important bills like GST, Land Acquisition Bill, Real Estate Regulatory Bill etc.

But, I think they have no other option, but to do all this in order to survive for a few more months or years. As India is a democratic nation, we all have to bear such dramas year after year and the more they are able to successfully carry it out, the better are their chances for getting voted back to the power again. Chalo, chalta hai… aakhir India hai !!

But, whether markets go up or go down, a retail investor always gets stuck somewhere, either waiting for the markets to come down to make some investments or watching the markets fall like there is no tomorrow. It is easier to advise investors – “Buy when there is a panic and sell when there is a euphoria”, but it is very very difficult to follow it religiously. Small investors are never able to follow it and they do the exact opposite most of the times. That is why, most of them finally end up bearing losses, after which they stop investing in equities forever.

Equity Linked Savings Schemes (ELSS) – Tax Saving Mutual Funds u/s 80C

Tax saving season is gathering pace again. While service class people are required to submit their tax saving investment proofs in offices, others will also wake up soon to take such actions. Whenever the markets jump extraordinarily during a financial year, Equity Linked Savings Schemes, or popularly known as ELSS, become the investors’ favourite investment instrument for tax saving under section 80C.

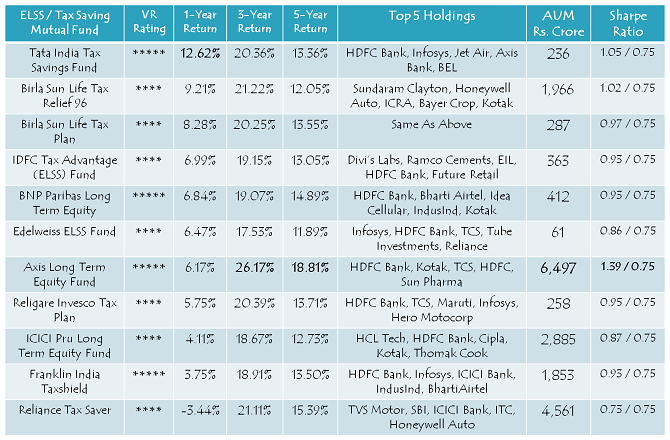

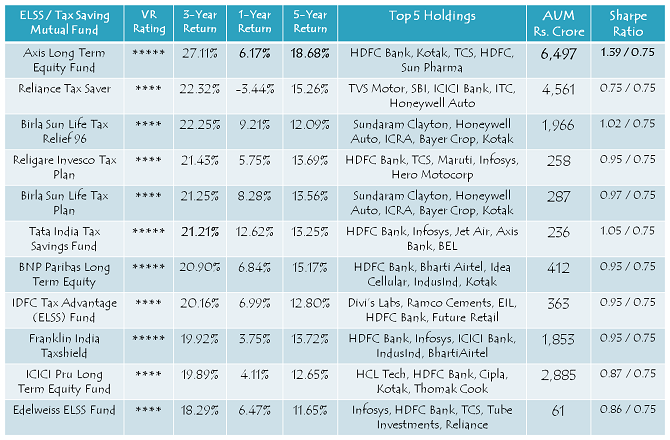

For the last two years or so, investors have been putting a lot of money in these ELSS schemes, but the returns have remained moderately below their expectations. In the three tables below, you can check the best performing ELSS schemes for a period of 1 year, 3 years and 5 years, starting from January 3, 2011 to December 31, 2015.

Best Performing ELSS from January 1, 2015 to December 31, 2015

Best Performing ELSS from January 1, 2013 to December 31, 2015

Best Performing ELSS from January 1, 2011 to December 31, 2015

Personally, I feel these equity linked saving schemes (ELSS) are the best investments to save tax under section 80C. But, conservative investors should prefer PPF, NSC or tax saving fixed deposits (FDs) over these schemes as these funds can have considerably high volatility over your investment period and if any of your financial goals hinge on the returns generated by these funds, you could be fairly disappointed with their returns.

Also, the schemes taken up here in the tables above are not the only good schemes to invest in, there are around 30 more ELSS schemes from which you can pick two or three schemes which suit your investment objectives. You can consult your investment/tax advisor for making such investments.

Please share your views about your investment experience in equity mutual funds and whether you make investments in these funds or not for your tax saving. I think it would be a great topic of discussion here.

Nice post on where to park the funds for future..

10 Differences between Tax Saving Tools like PPF and ELSS.

More info@ https://www.moneydial.com/blogs/10-differences-between-tax-saving-tools-like-ppf-and-elss/

kindly suggest new plan for 1 year baby

ravi

I am 32 years old and looking for investment opportunities, basically for retirement purposes, since I am just 32, I am ready to take bold investment ideas that bring me great rate of returns.

What would you suggest is better, p2p or mutual funds?

Thanks

Hi,

I have invested Rs. 35K each in Franklin and reliance tax saver in march 15, Since there is a lock in period of 3 years for with drawl , can i switch the ELSS fund to another tax saver before 3 years if one of the 2 doesnt perform well ? If yes, what would be the financial implications ?

Investing in ELSS gives tax benefit and better interest rate

http://moneydial.com/investing-in-elss-gives-tax-benefit-and-better-interest-rate/

This is a very good scheme

Thank you so much for this post. It is really useful and great.

Hi Shivji

Greetings.

Could you guide me by listing 10 top Mutual Funds based on the rankings of their EQUITY FUNDS to start SIP from April 2016.

Many thanks for the response to my earlier mail.

Dear Sir,

Though the Axis Long Term is rated the best it did not feature in your recommended three ELSS. Is it because the fund manager has migrated out of Axis MF?

Regards

No Shekhar, that is not the reason for not having Axis Long Term Equity in my preferred list of funds. I have a contrarian approach actually.

I followed the SIP route for investment in Axis Long term fund (ELSS).

In the last one year I have a negative growth as the SIPs generally got triggered at highs.

Is it a pattern or by sheer accident?

warm regrads

SIP investment does not guarantee positive returns. It is a way to avoid timing your investments. SIPs getting triggered at highs could be a coincident, but generally the markets have fallen, so having negative returns is natural.

This article provides us the detailed information about mutual funds. To make any form of investment, you have to save money and you can try an expense manager app that would help you to save money. Here’s the download link: https://play.google.com/store/apps/details?id=com.techahead.ExpenseManager

Hi Shiv,

Ok, if the ratios are similar for all of them, they’re operating the way a cartel would. From an investor’s viewpoint, an expense ratio greater than 2% is actually obscene.

Wouldn’t Quantum tax saving fund be a better bet? Think their expense ratio’s just 1.25%. You could consider mentioning that fact in your blogpost.

Cheers,

S

Hi Sam,

Performance matters more to the investors as compared to the expense ratios. But, I’ll try to cover expense ratios of ELSS in a separate post.

Hi Shiv,

In fact, the performance of a mutual fund is negatively correlated with its expense ratio over a fairly long time horizon. So if an investor cares about performance, he has to care about expense ratios!

Check what John Bogle has to say about high fees:

http://www.marketwatch.com/story/john-bogle-on-why-your-retirement-plan-stinks-2014-10-30

Await your post on expense ratios.

Cheers,

S

Hello Shiv

I need invest for a short term say about 3-4 years specifically for claiming the tax benefit under 80c. I have ELSS as the only option available to me.

After investing in your above given suggestions (HDFC Tax Saver, Franklin India Taxshield and Reliance Tax Saver),should i further diversify in Axis Long term fund ?

I plan to invest upto 5 lacs each year divided among 5 different family members. (The remaining amount of upto Rs50k per file per year, I plan to invest in PPF to avail full benefit under 80c)

Hi Krunal,

Axis Long Term Equity Fund is a good fund and has outperformed all the three funds I have mentioned during last 5 years or so. So, now it is up to you which all funds you want to invest into.

Dear Shiv,

Thanks for the post. Can you add the expense ratios for each of the schemes and update the tables. Its quintessential to know expense ratios while comparing mutual fund schemes.

Cheers,

Sam

Hi Sam,

There is no space left for adding one more column to the table above. Moreover, most of these companies have expense ratio between 2.25% to 2.90%. So, I think there is not much value addition it will have even if it is mentioned here.

Thanx a lot Shivji. I would be grateful if you could suggest another 2 or 3 fund houses based on your experience.

Thanx again.

Hi Mr. Hariharan,

Personally I like HDFC Tax Saver, Franklin India Taxshield and Reliance Tax Saver, but for the last couple of years, HDFC Tax Saver is performing very poorly.

Hi Shiv, could you please suggeat some good equity schemes

Hi Mukesh,

I’ll try to cover it in a separate post.

Good jone Shiv

Thanks Anubhav!

Hi Shivji

I’m a regular reader of your blogs and find them immensely informative and educative. I also appreciate your prompt response to the queries of your readers.

I had retired from service and plan to invest in various schemes of HDFC MF and Franklin Templeton MF with whom I already have accounts and investments. My plan is to invest around Rs.3.80 lakhs per year (incl my wife’s who is in service) through SIP mode on various schemes; mainly equity-based of these two fund houses.

My query is whether I should restrict myself to continue to invest in these two Fund houses only or to invest in well-performing schemes of other Fund houses limited to the above ceiling. I feel the second option could involve KYC and monitoring issues.

Please advise.

Hi Mr. Hariharan,

I think it is better to diversify your investment among at least 3-5 funds. KYC is just a one time process for all the fund houses, after which you need not undergo such process. I think monitoring up to 5 funds is ok, there is no point over-diversifying your portfolio.

dear Mr shiv ,

birla tax relief 96 fund – generated regular return over 20 years. real show for money compounding ! Readers .. Enjoy this opportunity.

Yes, that’s right! Equity mutual funds generate good returns over a period of time. Timing of your investment is very crucial for above normal returns though.