This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

2016 so far has turned out to be a nightmare for the equity investors. Portfolios have undergone a massive value erosion and sentiment has turned extremely negative. Financial advisors, who were recommending a higher allocation to equity so far, have also become cautious to advise higher equity investments. Some analysts have started calling it a bearish phase and not just a deep correction in a bullish phase.

However, it is not just the equity portfolios which are bleeding. Debt portion of portfolios are also facing the music. Past few months have seen the 10-year G-Sec yield rising to 7.95% from a range of 7.60-7.65% in September last year. Due to a scary fall in international crude prices and commodity prices like steel, aluminium etc., many companies are facing it difficult to service their debt. Credit rating agencies have also started downgrading these companies resulting in a fall in the NAVs of debt mutual funds which have lent huge money to such companies.

In such a difficult environment, investors want to opt for safer investment options and it seems that tax-free bonds are among the best options available. NHAI is launching one such issue from 24th February i.e. Wednesday and the issue is scheduled to get closed on the first of March. NHAI will raise Rs. 3,300 crore from this issue.

Here you have the salient features of this issue:

Size of the Issue – Though base size of this issue is Rs. 500 crore, NHAI will retain an additional Rs. 2,800 crore in case of oversubscription, thus making it a Rs. 3,300 crore issue. NHAI has already raised approximately Rs. 15,700 crore by issuing tax-free bonds through its public issue in December and a couple of private placements in September 2015 and February 2016.

With this Rs. 3,300 crore issue, NHAI will exhaust its full quota of Rs. 19,000 crore for the current financial year.

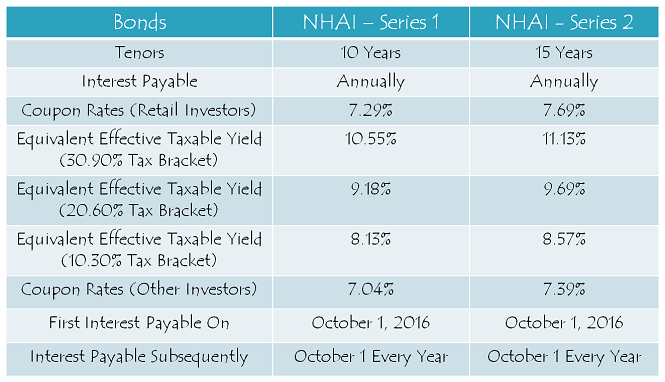

Coupon Rates on Offer – With a widening gap between the 10-year G-Sec yield and 15-year G-Sec yield, NHAI issue will carry 7.69% coupon rate for 15 years and 7.29% for 10 years. As with its first issue, 20-year investment option will not be there this time as well.

For the non-retail investors, coupon rate will be lower by 25 basis points (or 0.25%) for the 10-year option and 30 basis points (or 0.30%) for the 15-year option.

Rating of the Issue – CRISIL, ICRA, CARE and India Ratings have once again assigned ‘AAA’ rating to this issue. Also, these bonds are ‘Secured’ in nature i.e. in case of any default, the bondholders would carry a right to make claim on certain assets of the company.

NRI/QFI Investment Not Allowed – Like its previous issue, Non-Resident Indians (NRIs) won’t be able to make investment in this issue as well. Qualified Foreign Investors (QFIs) are also not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 20% of the issue is reserved i.e. Rs. 660 crore

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved i.e. Rs. 660 crore

Category III – High Net Worth Individuals including HUFs – 20% of the issue is reserved i.e. Rs. 660 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 1,320 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing & Allotment – NHAI has again decided to get these bonds listed on both the stock exchanges i.e. National Stock Exchange (NSE) as well as Bombay Stock Exchange (BSE). Bonds will be allotted and get listed on the exchanges within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – Again, it is not mandatory to have a demat account to apply for these bonds. Investors have the option to subscribe to these bonds in physical form also. Also, even if you get these bonds allotted in your demat account, you have the option to rematerialize your holding in physical/certificate form if you decide to close your demat account in future.

However, whether you apply for these bonds in demat form or physical form, the interest payment will still get credited to your bank account through ECS.

No Lock-In Period – These tax-free bonds do not carry any lock-in period and you can buy/sell them on the stock exchanges at the market price whenever you want.

Interest on Application Money & Refund – Successful allottees will earn interest at the applicable coupon rates i.e. 7.29% p.a. for 10 years and 7.69% p.a. for 15 years, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of face value Rs. 1,000 each. There is no upper limit for the investors to invest in this issue. However, an investor investing more than Rs. 10 lakhs will be categorized as a high networth individual (HNI) and will get a lower rate of interest as applicable.

Interest Payment Date – NHAI will make its first interest payment on October 1 this year and subsequent interest payments will also be made on October 1 every year, except the last interest payment, which will be made to the bondholders along with the redemption amount on the maturity date.

Record Date – For the payment of interest or the maturity amount, record date will be fixed 15 days prior to the date on which such amount is due to be payable.

Should you invest in this issue?

I think tax-free bonds are one of the best fixed income options available for the retail investors. There is no fixed income option which carries so many distinct advantages which these bonds have, like tax-free interest, easy liquidity, favourable tax liability if sold after holding for more than one year, scope of capital appreciation, annual interest payments etc. Risk-averse investors with a long term view should definitely invest in these bonds.

Also, there is no certainty that these bonds will be allowed to be issued next year as well. For that, we’ll have to wait for the Budget speech on February 29. In case the Finance Minister decides not to allow these bonds for the next year, it will result in a sharp increase in their demand. Also, as there is a difference of 0.40% between the interest rates of 10-year bonds and 15-year bonds, I think it makes more sense to subscribe to the 15-year option.

Application Form for NHAI Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHAI tax-free bonds, you can contact me at +919811797407

Day 3 (February 26) subscription figures:

Category I – Rs. 1,895 crore as against Rs. 660 crore reserved – 2.87 times

Category II – Rs. 4,359.36 crore as against Rs. 660 crore reserved – 6.60 times

Category III – Rs. 1,385.94 crore as against Rs. 660 crore reserved – 2.10 times

Category IV – Rs. 1,567.81 crore as against Rs. 1,320 crore reserved – 1.19 times

Total Subscription – Rs. 9,208.11 crore as against total issue size of Rs. 3,300 crore – 2.79 times

Dear Shiv,

Will refund from Hudco tax free bond Tranch II issue come in time for upcoming IRFC or NABARD issue.

As HUDCO issue is smaller, may not get full allotment for 1st day subscribers. So how to go about investing in TFB’s . Wait for the bigger issue ??

Iam puzzled.

Hi Pankaj,

As the launch dates of IRFC and NABARD issues are yet to get announced, it is not possible for me to answer your query with certainty. But, I think if you need to invest in only one issue, then you should wait for the bigger issues of IRFC or NABARD.

Shiv,

Can you please confirm what other TFBs are due to come out this fiscal year ?

If possible please let me know their approximate sizes as well…

Thanks a lot !!

Hi Gaurav,

IRFC and NABARD issues are expected to get launched in the 2nd week of March. Expected issue sizes are Rs. 2,450 crore and Rs. 3,500 crore respectively.

HUDCO Tranche II update:

Issue opens – 2nd March, 2016, Issue closes – 10th March, 2016

Interest Rates for Retail Individual Investors investing upto Rs. 10 lacs:

10 years – 7.29% p.a.

15 years – 7.69% p.a.

Total Issue Size – Rs. 1,788.50 crore, including Green-Shoe Option to retain Rs. 1,288.50 crore

What does “Green-Shoe” option mean? Also why do they call it “coupon rate”? Is it different from “interest rate” that is there for Bank fixed deposits?

Sorry for the naïve questions.

Green-Shoe option is the option to retain oversubscription in case the issue gets oversubscribed over and above the base issue size. ‘Coupon’ term originated as historically coupons were affixed to bond certificates and the investors were supposed to detach and surrender the coupons to get their due interest payments periodically. Interest rate and coupon rate are used interchangeably.

Thank you Sir. Really learning a lot from your site. Don’t know if there is any other site where people clarify these kind of doubts. Much appreciated 🙂

Dear Shiv,

I know it’s too late for retail investors now to buy this 2nd tranche, but how do you go about buying this TFB? Can it be bought online without doing any paperwork? I’m having ICICI direct trading account, but don’t see it listed. Can I buy it directly from NHAI?

Want to be better prepared for next time 🙂

Thanks,

Melwyn

Hi Melwyn,

You can buy in secondary market from ICICI direct. Buy the earlier issues listed.Go to Equity, NCD List. You will find some list of TFBs. Click on view more. All the TFB with YTM will appear. Buy which ever is good for you. You need not boy NHAI only, there are whole lot of companies like NTPC, IRFC etc. Based on YTM, you can choose. ICICI Direct charges anothe 1.1 % towards brokerage etc. take that also into account.

Thanks George for your inputs!

Thanks George. For the upcoming TFB where do I find it? For eg HUDCO tranche 2 is coming on 2nd March, but I’m not able to find it on icici direct. Will it show up only on 2nd March? and if so, will it be listed in the same place you mentioned (under “Equity”, “NCD List”)?

Thanks for your response.

These are normally available under IPO. I do not recollect seeing this in the app, but have invested in the past using icicidirect.com. Had also received a mail from icicidirect regarding the ipo a couple of days ago.

If you buy in secondary, additional brokerage charges may be incurred so may make sense to wait for the ipo of the other issuers.

Thanks nn. Yes, I managed to find it today in the IPO section.

UPDATE

HUDCO is launching on 02/03 at the same rates.. 7.29/7.69 for retail. Total size 1788 crs (500 + 1288 oversubscription). Retail quota is 715 crs.

ICICI Direct would support it.

Thanks nn for the quick update!

Day 2 (February 25) subscription figures:

Category I – Rs. 1,895 crore as against Rs. 660 crore reserved – 2.87 times

Category II – Rs. 4,358.86 crore as against Rs. 660 crore reserved – 6.60 times

Category III – Rs. 1,384.94 crore as against Rs. 660 crore reserved – 2.10 times

Category IV – Rs. 1,560 crore as against Rs. 1,320 crore reserved – 1.18 times

Total Subscription – Rs. 9,198.80 crore as against total issue size of Rs. 3,300 crore – 2.79 times

Hi Shiv,

are these bonds are tradeable in stock exchange as well

regards

Pawan Aggarwal

Hi Pawan,

Yes, these bonds are tradable on the stock exchanges – https://www1.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

Any guess for allotment basis for retain investors, based on oversubscription in NHAI Tranche II Tax free bonds?

Hi Shirish,

Approximately 87-88% allotment will be made.

Hi Shiv

I applied for these bonds in retail category today ( Feb 25). Given that they were oversubscribed yesterday, what is the approximate allocation that I can expect?

Thanks

I do not think people who applied today will get any allotment. All of the amount will get refunded.

Hi Jyoti,

You should not expect any allotment against your application.

Is there a point in applying under retail if the NHAI issue is already oversubscribed for this category ?

No.

Yes. Only if you want 5% interest on money.

Hi KKJ,

If not applied on the first day, no allotment will be made against your application.

Manshu/Shiv

Nothing on upcoming budget? Never thought I would say this but this govt is scaring us more than the previous one. At least you knew what to expect then in budgets.

Hi Harinee,

It is the human nature to get unduly scared and excited. Markets are falling due to the sins Congress did in the past and are doing in the present. The present government is trying to correct those anomalies and I think the course correction is taking its own sweet time. Global economic conditions are also working as headwinds and our wounds are getting more painful.

Shiv

Any idea why the subscription is so low.I really expected it to see only 47% like last time but seems quite a high number will get this time.

Is it because of HUDCO,IRFC,NABARD following or people investing in equity direct as many shares are at a bargain?

Thanks

Hi Harinee,

As I have mentioned above, I think it is primarily because NHAI issue has come at a very short notice. Also, investors probably do not want to invest more in NHAI as they had already invested good amount in December and got full allotment.

I fully agree with Vin and others.

Shiv, all your postings and replies on TFB are very useful to us. I really appreciate your dedication on this forum. Looking forward for upcoming TFB issues and your posts. Once again, thanks a million, from bottom of my heart.

Thanks Mr. Singh! It is your love and affection which keeps me motivated, dedicated and patient! Thanks once again! 🙂

Dear Mr. Shiv Kukreja,

Kindly let me know the charges by law, that generally DEMAT Service Providers can charge customers for ‘off market’ DEMAT transfers of TFB’s/Equity between 2 family Accounts of same DEMAT service provider.

Thank you.

Hi S.K.,

Please check the tariff structure of CDSL, including the Off-Market transactions – https://www.cdslindia.com/dp/dpfees.html

Dear Mr. Shiv,

Was unable to appreciate the link sent. Please elaborate in your words directly. Will be grateful fir your help.

Shiv, Have to admire your super patience and kindness in replying to so many repeat and mundane questions … by many ‘novice’ people who are anxious to do the right thing with their savings. Good to know you do this service with no upfront charge. The many sincere thanks you receive are payment enough, I guess. Great work!

Thanks a lot Mr. Srinivasan for your kind and encouraging words! 🙂

HUDCO issue is expected to get launched next on 2nd or 3rd of March.

Hi Shiv,

Thanks for the wonderful infomation you are providing.

Can you please clarify on selling these bonds in stock exchanges where these bonds get traded. Below are my questions.

1. The bonds are purchased at 1000/- each. Is there an chance of bond value getting increased in stock market?

2. If the above is true can the bond value also get decreased resulting in Losses? If that is the case (gain/loss) how come these can be called fixed income investments?

3. If I sell the bond(s) in stock market, what will happen to the interest on the bond? Interest hence forth would not be paid to me but would be paid to whomsoever bought the bond?

4. Once the bond value increases/decreases, how come its value remain same during maturity.

Sorry for the multiple questions but I’m confused with these.

Many Thanks,

Venu

Thanks Venu,

1. Yes, if the bond yields (YTM) go down, then the market value of these bonds would go up. Tax-Free Bonds issued two years ago are all trading at a 20-25% premium.

2. Yes, the market value of these bonds can also go down, if the bond yields go up. They are called fixed income investments as these bonds carry coupon rate of 7.69% per annum which remains fixed throughout its tenure of 15 years, irrespective of its market price going up or down.

3. Yes, full year’s interest will be paid to the bondholder whose name is there in the records of the company on the record date.

4. Its value will be equal to its face value on maturity as nobody will pay you any premium for the bonds which will cease to exist on maturity.

Thank you very much Shiv for patiently answering my questions. I’ve come to this site by chance but now I’m an regular follower.

Glad to know that, thanks Venu!

As you mentioned that TFBs issued 2 years ago are trading at 20 – 25% premium currently, so will their market value come down toward their face value as their maturity date comes close? As you mentioned in another comment, as the maturity date comes near no one will pay more than the face value as that is what they will get for the bond on the maturity date. Just wanted to clarify my understanding. Thanks.

Hi Melwyn,

Yes, the market value of these bonds will merge with the face value on the maturity date.

As per notification on 18th Feb, Nabard is allowed to raise 5000 Crore Tax Free bonds. Again we can expect an issue of 3500 Crore for Public from NABARD. We can expect coupon rate of 7.65% 7.8% considering the current trend of GILT.

https://www.taxmann.com/topstories/104010000000047645/nabard-allowed-to-issue-rs-5000-crore-tax-free-bonds.aspx

Thanks George for sharing this info!

I read somewhere that Nabard is not planning public issue of tax free bonds. They are going for private placement only

Hi Ramadas,

It is an incorrect information you have read. NABARD has been authorised to raise Rs. 5,000 crore by issuing tax-free bonds this financial year. It will raise Rs. 1,500 through private placement, after which it will have to mandatorily raise Rs. 3,500 crore through a public issue. It cannot raise more than 30% of the allocated amount through private placement.

You are right Shiv. I just reread in Financial express that they are raising 1500 crore through private placement of TFB. Nothing was mentioned on public issue and I was under the impression that it is only private placement. Thanks for clarifying.

Thanks Ramadas!

Shiv – retail category oversubscribed by 6.63 times, so I think successful applicants should get (1320/200)/6.63 = 99.55 % allocation. Please confirm.

Hi Vineet,

You are checking the BSE subscription numbers only. There are NSE subscription numbers also to be added.

Thank you very much, Shiv. Let me once again reiterate- you have provided an invaluable platform for retail investors like us!

Thanks a lot Vin for your kind and motivating words! 🙂