This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

As gold prices go up, more and more people start investing in gold in the hope of prices going up further. This has always been the case and seems this trend will continue in future as well. To cash it on this trend and cap purchase of physical gold, the government has launched its 5th tranche of Sovereign Gold Bonds (SGBs) from September 1, 2016. This will be the second such issue in the current financial year and fifth overall since it was first introduced in November 2015.

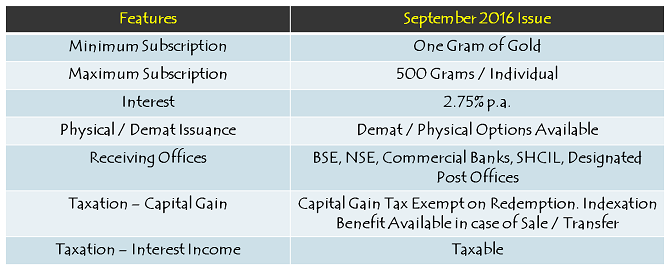

Notified as Series II of the current financial year, this issue is open till September 9th. Below are the salient features of this bond issue:

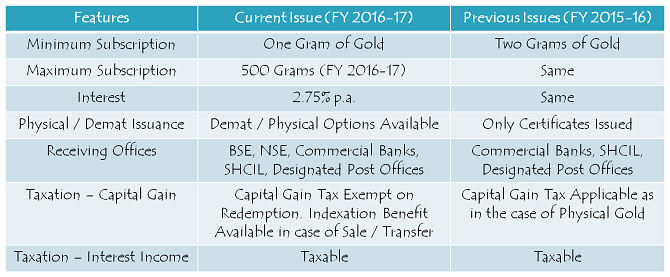

Salient Features of Sovereign Gold Bonds – Series I of FY 2016-17

Issue Price – As the price of gold in the international market has risen after Brexit, price for this tranche has been fixed at its highest level of Rs. 3,150 per gram of gold. Issue price for the first tranche was fixed at Rs. 2,684 per gram of gold, that of the second tranche was Rs. 2,600 per gram of gold, it was Rs. 2,916 per gram of gold in the third tranche and Rs. 3,116 per gram of gold in the fourth tranche.

The government could raise only Rs. 246 crore from its first issue in November issuing bonds with around 916 kg of gold, Rs. 798 crore from the second issue in January with around 3,071 kg gold, Rs. 329 crore from the third issue in March with around 1,128 kg gold and Rs. 919 crore from the fourth issue in July.

Issue Price Methodology – The issue price of Rs. 3,150 per gram of gold has been fixed on the basis of simple average of the closing prices of gold with 999 purity of the previous week (August 22, 2016 to August 26, 2016) published by the India Bullion and Jewellers Association Ltd. (IBJA).

Coupon Rate @ 2.75% p.a. – As always, interest rate has been fixed at 2.75% p.a. to be paid twice in a year. Apart from this fixed rate of 2.75%, there is a potential of capital appreciation with these bonds and also a risk of decline in gold prices. Fall in gold prices would result in a negative yield from capital gains point of view, but 2.75% p.a. interest would remain fixed throughout its tenor of 8 years.

Allotment Date & Tenor of Investment – As per the RBI, these bonds would get allotted on 23rd of September and carry a maturity period of 8 years from the allotment date. However, there is an option to surrender these bonds from the 5th year onwards. Option to redeem will be there in the 5th, 6th and 7th year of investment only on the interest payment dates.

Delay in Allotment & Listing – Investors should have low expectations from the RBI to get these gold bonds allotted in a timely manner on September 23rd. No issue in the past got allotted on time as promised. There is no grievance redressal mechanism in place to help you either. So, if you apply for these bonds now, you might again be required to have a lot of patience in getting them allotted and see their listing in a timely manner.

Demat Option Available – Like its fourth tranche, you have the option to get these bonds allotted in demat form as well. Introduction of demat facility should bring down the time taken to allot these bonds and get them listed on the stock exchanges for trading.

Tradability, ISIN & Exit Option Before 5 years – As mentioned above, these bonds are redeemable from the 5th year onwards. However, in order to provide liquidity to its investors before 5th year, the government and RBI have made provisions for these bonds to list on the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE). These exchanges have allotted ISIN as well to these bonds, which is IN0020160043. You can sell your gold bonds on these stock exchanges after they get allotted on or after September 23rd.

In order to carry out premature redemption after 5 years, investors would be required to approach the concerned intermediary 30 days before the coupon payment date. This request for premature redemption would only be entertained if the investor approaches the concerned intermediary at least one day before the coupon payment date. Redemption proceeds will be credited to the customer’s bank account.

Online Bidding Platforms Launched – During its last issue, RBI introduced online bidding platforms for these gold bonds with BSE and NSE. Applying for these bonds has become a lot easier now with these platforms in place. These platforms will remain open till 12 a.m. on September 9th. There is a cooling off period of 30 minutes from 5:30 p.m. to 6 p.m. everyday.

Taxation in case of Redemption/Sale – Sovereign gold bonds are subject to capital gains tax treatment from FY 2016-17 onwards and gains are tax exempt if these bonds are redeemed after 5 years. Moreover, if these bonds are sold on the stock exchanges after 3 years from the allotment date, indexation benefits can be availed to calculate your capital gain or loss.

As per the Budget speech “It is proposed to provide that redemption by an individual of Sovereign Gold Bond issued by Reserve Bank of India under Sovereign Gold Bond Scheme, 2015 shall not be charged to capital gains tax. It is also proposed to provide that long terms capital gains arising to any person on transfer of Sovereign Gold Bond shall be eligible for indexation benefits”.

So, as an individual, whenever you redeem these gold bonds after holding them for 5 years, you are not liable to pay any capital gains tax. Indexation benefit will also result in a substantial tax saving.

No TDS, Interest @ 2.75% is Taxable – Interest income earned every year @ 2.75% p.a. is taxable and it is the responsibility of the investors to show it as an income from other sources in their income tax returns (ITRs). No TDS (tax deducted at source) will be deducted by the RBI while making interest payments.

Minimum and Maximum Investment – Like its last issue, investors are required to buy a minimum of 1 unit of these bonds i.e. 1 gram of gold or a minimum investment of Rs. 3,150. However, you can buy a maximum of 500 units of these bonds or 500 grams of gold, which works out to be Rs. 15,75,000.

NRI/QFI Investment Not Allowed – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in these bonds. Only resident Indian entities, including individuals, trusts, universities and charitable institutions are eligible to invest in these bonds.

Transferability – These bonds can also be transferred by execution of an instrument of transfer, in accordance with the provisions of the Government Securities Act.

Collateral for Loans – If required, these bonds can be used as collateral for seeking loans from various lending institutions.

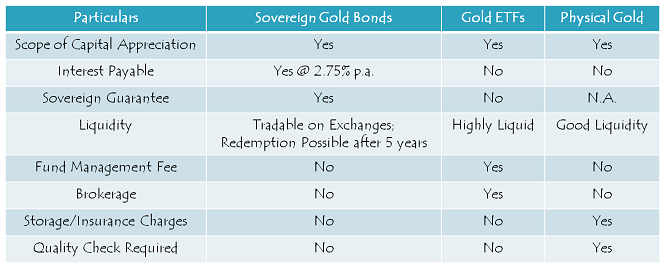

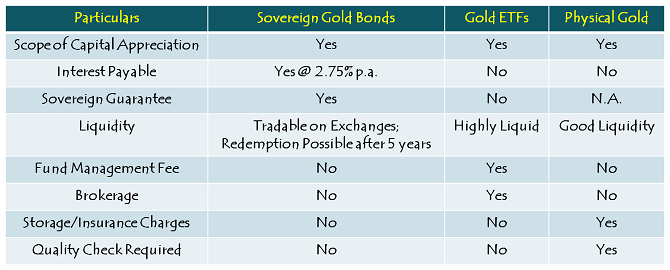

Sovereign Gold Bonds vs. Gold ETF vs. Physical Gold – A Comparative Chart

Should you invest in Sovereign Gold Bonds – Series I, FY 2016-17?

Gold is considered to be a hedge against inflation, recession and other times of uncertainties. It is also considered to be a safe haven for investors, that is why investors put more money in gold during volatile economic conditions. Moreover, when the global economies get stronger and the US dollar strengthens, investors move their investments away from gold.

As the US Federal Reserve is set to raise its policy rates sooner or later due to a stronger than expected jobs market, I think the gold prices should weaken going forward. However, investors with a bullish stance on gold prices and a medium to long-term investment horizon can consider investing in these bonds. As it is the cheapest, most tax efficient, risk-free way of investing in gold, I think this way of investing in gold is the best way. If your portfolio does not have gold as an investment, then you should definitely go for it, albeit in a staggered way.