IRFC Tax-Free Bonds Issue Details

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Indian Railway Finance Corporation Limited (IRFC) will be the next company to launch its tax-free bonds this financial year from January 21st. The company plans to raise Rs. 1,000 crores from this issue with an option to retain oversubscription up to Rs. 8,886.40 crores.

This will be the second such issue by IRFC as the company issued tax-free bonds last year also. The issue will close on January 29th, coincidently on the same day on which the RBI is scheduled to announce its monetary policy.

Investors who want to invest in these tax-free bonds for their higher effective yields, I think this is the last such opportunity this financial year. I am saying this because IRFC was among those few companies which filed their final prospectus in December when the yield on the 10-year government securities was higher at around 8.15-8.20%. It has fallen by 35-40 basis points (or 0.35-0.40%) since then.

As the interest rates offered by these companies are linked to the benchmark government securities, the upcoming tax-free bond issues are going to offer lower rate of interest and hence, will be very unattractive.

As most of these tax-free bonds are quite similar in their regular features, here are some of the unique features of this issue:

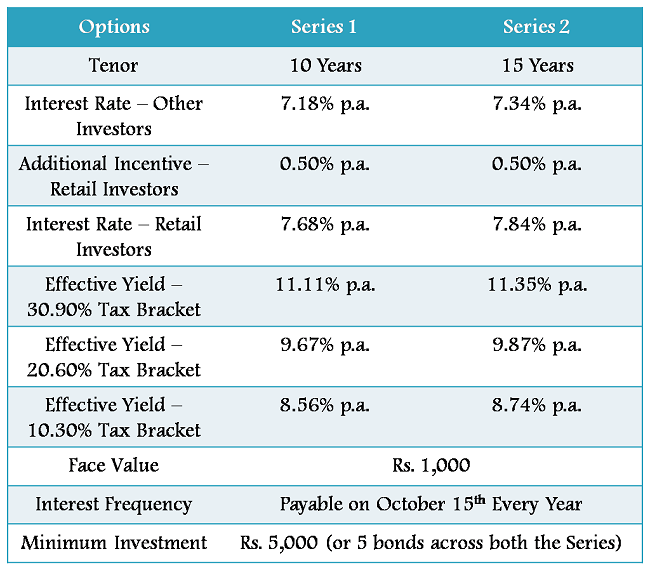

Interest Rate

IRFC is offering 7.84% per annum for its 15-year option and 7.68% per annum for the 10-year option to the retail investors investing up to Rs. 10 lakhs. Again, the additional incentive of 0.50% will be payable to the original allottees only who invest in these bonds during this offer period. In case these bonds are sold or transferred by the original allottees, except in case of transfer of bonds to legal heir in the event of death of the original allottee, the coupon rates will be revised downwards to the base coupon rates.

As with all of these issues, the interest rate for the other categories of investors, like QIBs, corporates and HNIs, will be 0.50% lower than the above rates offered to the retail investors. For 15 years, it will be 7.34% per annum and for 10 years, it will be 7.18% per annum.

NRI Investment: Like HUDCO tax-free bonds, NRIs can also invest in this issue, but only non-US based NRIs. They can apply for these bonds both on repatriation basis as well as non-repatriation basis. Eligible NRIs can use their NRE/NRO/FCNR/NRNR/NRSR account to invest in this issue but will be required to get a bank certificate made to confirm that the money has been used out of an NRE/NRO/FCNR/NRNR/NRSR account. If the NRI is a Person of Indian Origin (PIO), then it is mandatory to attach the copy of the PIO card.

Other Terms of the Issue

The issue is secured in nature and has been rated ‘AAA’ by CRISIL, ICRA and CARE. The bonds will get listed within 12 working days post closure of the issue on both the national exchanges, National Stock Exchange (NSE) and Bombay Stock Exchange (BSE).

Like its first issue last year, IRFC has fixed October 15th as the interest payment date for this issue as well. The investors have the option to apply for these bonds either in the demat form or physical form and thus, demat account is not mandatory to apply for these bonds.

40% of the issue is reserved for the retail investors, another 20% of the issue is reserved for the high net worth individuals (HNIs) i.e. for the individual investors investing above Rs. 10 lakhs. 20% of the issue is reserved for the institutional investors and the remaining 20% is for the corporate investors.

The minimum amount of application is Rs 5,000 with face value of Rs 1,000 per bond. The allotment will be made on first-come-first-serve basis.

About IRFC

Indian Railway Finance Corporation Limited (IRFC) is a wholly-owned public sector undertaking (PSU) and works as a financial arm of Indian Railways. It is also registered with the RBI as Infrastructure Finance Company-NBFC (IFC-NBFC). IRFC has strong asset quality zero gross and net non-performing assets (NPAs) as on March 31, 2012.

The proceeds raised from the issue will be utilised by the company towards financing the acquisition of rolling stock that will be leased to the Ministry of Railways and for funding other projects approved by the Ministry of Railways.

As mentioned above, interest rates have fallen by around 0.35-0.40% in the last few days and going by this trend, the upcoming issues of tax-free bonds will offer lower rate of interest. As much anticipated, if the RBI decides to cut interest rate this time on January 29th, the bond yields should fall more from these levels.

So, it is highly recommended now for the investors in the higher tax brackets to use this opportunity to invest their money either in the ongoing HUDCO tax-free bonds which offer the highest interest rates or in this issue which is rated higher at ‘AAA’.

Shiv = Something interesting. The subscription to tax free bonds has lately picked up. HUDCO bonds are oversubscribed if not ‘?’ heavily ‘?’ subscribed. Non individual investors have shown interest in IRFC bonds on day one itself. Any analysis on possible reasons?

Hi Mr. Arun… I think the possible reasons are – 1) A very sharp & likely sustainable fall in the yields of G-Secs, this is the most important reason 2) It is almost certain that the forthcoming tax-free bond issues will offer lower rate of interest 3) IIFCL & IRFC have better fundamentals (both have zero NPAs) as compared to REC, PFC & HUDCO 4) NRIs are allowed to invest in these issues 5) Non-individual investors (or QIBs) are smarter investors and they prefer to have risk-free returns with enough margin of safety, which these tax-free bonds provide now.

Thanks Shiv for yr valuable comments/ inputs. With your kind permission, I would like to reword your inputs as below since this portal is as I understand primarily to advice the readers.

The readers are advised to read between the lines particularly his inputs on participation of NRIs and smart QIBs. In addition to yield/ returns, I consider liquidity to be a very important parameter especially when you are talking of investment for 10/ 15 and/ or 20 years. Investments are made because today you have more money than your needs. Such situation may not remain true all the times. It is not possible to forecast micro requirements and your income. Hence liquidity is very important. I believe liquidity will be better for bonds where there is interest by NRI/ QIBs. Individual investors may be reluctant to purchase the bonds offering 7.3% appx. The secondary market purchases are therefore likely to be mostly by NRIs/ QIBs.

Next, the REC/ PFCL bonds listed after their offer in Dec-2012 are quoting around their offer price because of the primary market opportunities offered by HUDCO/ IRFC and some other issues to follow. Once the primary market offerings stop and RBI agrees (?) for easing of interest rates the market price of all bonds will increase.

I also see value for bonds issued in Dec-2011/ Mar-2012 for certain type of investors. The investors may therefore weigh between secondary market purchases of old bonds vis-a-vis the fresh IPOs depending upon their investment attitudes and horizon.

Thanks for your inputs Mr. Arun!

What will be interesting to see is whether Govt goes forward with these tax free bonds in the forthcoming budget. I read few articles that IT people are unhappy seeing the huge loss of revenues and are asking Govt to stop this scheme. (But it could be a planted story to get people to rush in to buy these bonds). If these get discontinued then the listed price of the bonds are sure to move up.

Also many corporates cannot invest in anything less than AAA, so HUDCO was out of consideration for them.

Very difficult to say if the budget will provide for similar bonds in 2013-14. Though tax officials may be unhappy with loss of revenue, The Finance minister has many objectives to achieve. Money is needed for funding the PSUs projects. The problem is not loss of tax alone but also the distribution of bonds. The objective of large participation of retail through extra interest has remained unfilled. After tax saving bonds if tax free bonds also go, there would be some other scheme to attract capital.

The last date for subscription is extended till 8-Feb-2013

Either you save the tax and get the less return or pay the full tax and get more return. Ultimately the thing is same

Hi Abhishek… I dont think its the same thing. For an investor in the 30.9% tax bracket, the effective yield is 11.35% p.a. Please tell me which bank or ‘AAA’ rated instrument of a government company gives this kind of taxable return?

Got sms that IRFC bonds have been credited today. Thanks.

Thanks for sharing it Bhaskar.

please information irfc bond issue my email id