This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

A couple of days back, I got an investor query on my email id asking me whether she should go for NCDs issue of India Infoline Finance Limited (IIFL) or not and can we expect any tax-free bonds issue to offer monthly interest option. She also told me that she falls in the 30% tax bracket and her mother, for whom also she wants to invest, falls in the 20% tax bracket.

So, if you have been reading my posts regularly, you must be knowing my thoughts about it by now. I told her that I think it is better to invest in HUDCO tax-free bonds as compared to IIFL NCDs as she and her mother both fall in the higher tax brackets and also it is always better to go with debt securities of the government-owned public sector companies vis-a-vis private sector issuers.

But, her reason for considering IIFL NCDs was different and genuine also. She wanted to have a regular monthly income for her mother and she was not able to take a decision between Post Office Monthly Income Scheme (POMIS), which is fetching 8.40% annually to its investors for FY 2013-14, and IIFL NCDs, which are going to give approximately 43% higher interest @ 12% per annum.

Though she knew that POMIS deposit is government backed and old age people should not take high risks with their principal investments by depositing their hard-earned lifetime savings with private companies, she wanted to earn higher rate of interest, interest rate which is able to earn them somewhat higher than the spiralling inflation.

I told her that the government has not allowed any of the companies to issue tax-free bonds with monthly interest payment option. The maximum these companies can offer is to make the interest payments twice in a year, on a semi-annual basis. But, no company till date has issued bonds with a semi-annual interest payment.

So, what is the deal? How can you generate regular monthly inflows from your tax-free bonds, which are designed to pay it only once every year, and pay tax only to the minimum extent possible?

By now, we all know the taxability rules of the bonds/NCDs listed on the stock exchanges. What did you say? You do not know the tax provisions as yet? Shame on me if you do not know the taxation rules even now, I have been writing these posts since ages now.

🙂 Just trying to make you people feel a little light and prepared for reading a long post!

As per the language of HUDCO tax-free bonds prospectus – “As per third proviso to Section 48 of Income tax act, 1961, benefits of indexation of cost of acquisition under second proviso of Section 48 of Income tax Act, 1961 is not available in case of bonds and debenture, except capital indexed bonds. Thus, long term capital gain tax can be considered at a rate of 10% on listed bonds without indexation”.

I hope at least now the taxation rules are clear! No ?? Still Not ?? What did you say ?? The language does not tell you the rules for the short term capital gain tax. Oh yes, I am sorry !! You are right, my mistake !!

So, here you have the taxation provisions with respect to the short-term capital gains – “Short-term capital gains on the transfer of listed bonds, where bonds are held for a period of not more than 12 months would be taxed at the normal rates of tax in accordance with and subject to the provision of the I.T. Act.

A 2% education cess and 1% secondary and higher education cess on the total income tax (including surcharge for corporate only) is payable by all categories of taxpayers”.

I hope now it is done and nobody will forget these rules now onwards!

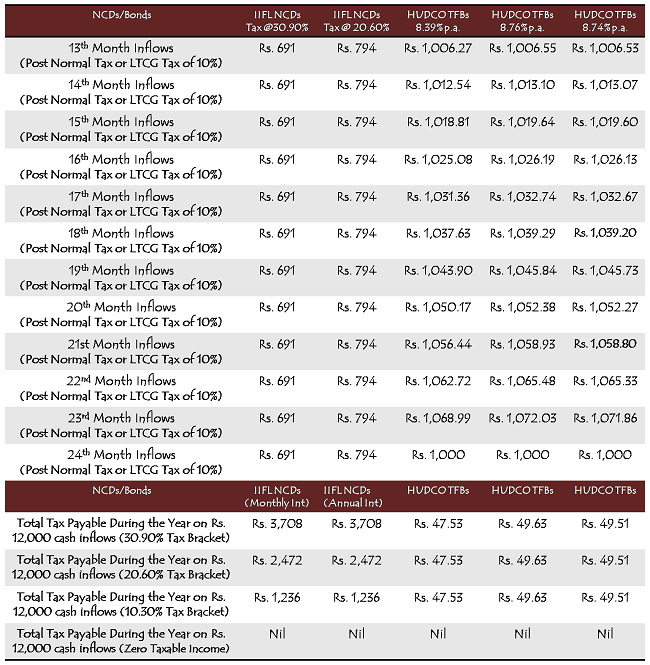

So, you must be asking, am I suggesting you to start selling these bonds every month from the end of the first month itself from the date of their allotment ?? You are partially right. Yes, I am suggesting you to sell 1% of your investment in these bonds every month to get a sort of monthly income, but not from the end of the first month itself, but starting from the 13th month of your investment from tax planning point of view.

How it works?

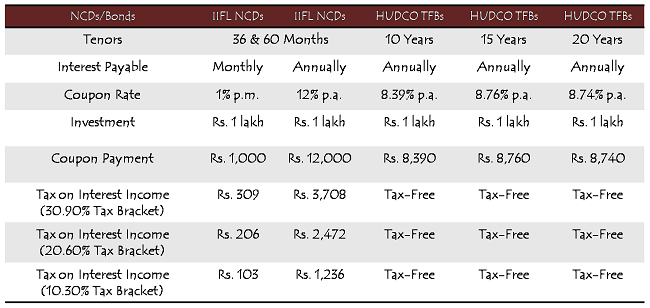

Suppose, you fall in the higher tax bracket of 30% or 20% and invest Rs. 1 lakh in any of the tax-free bond issues, HUDCO, IIFCL, PFC, IRFC, NHB or any other company. Stay invested with these bonds for at least one complete year and from the thirteenth month onwards, you can start selling 1% of your investment every month. If you do that every month, you are going to get 1% of your investment i.e. approximately Rs. 1,000, for 100 months or 8 years & 4 months. This way it is going to last till 9 years and 4 months from the date of your investment and that is how it would be helpful if your investment is for 10 years.

Assumptions

* The investor takes tax-free bonds in a demat account, in order to sell them on a monthly basis or periodicity of his/her choice. It is very difficult to find a buyer for the physical bonds.

* After each annual interest payment, tax-free bonds are assumed to appreciate in value exactly equal to the monthly value of their annual interest. So, if the annual interest is 8.76%, then the market price of the bond is assumed to appreciate by 0.73% every month i.e. 8.76% / 12 months.

* Tax is paid as & when each monthly cash inflow is received.

* Brokerage charges on sale of the bonds have been ignored as they vary across different broking houses and across different investors. Investors should consider them before taking a final decision.

Let me try to explain you the monthly cash inflow table. Interest earned on IIFL NCDs is taxable as per the tax slab of the investor, so it has been termed as the “Normal Tax”, whereas long term capital gain tax on listed tax-free bonds is 10.30%.

IIFL NCDs post-tax monthly inflow = Interest Rs. 1,000 – Tax Rs. 309 @ 30.90% = Rs. 691.

IIFL NCDs post-tax monthly inflow = Interest Rs. 1,000 – Tax Rs. 206 @ 20.60% = Rs. 794

IIFL NCDs post-tax monthly inflow = Interest Rs. 1,000 – Tax Rs. 103 @ 10.30% = Rs. 897

HUDCO TFBs post-tax monthly inflow (Rs. 1,006.55 – for understanding purposes)

Sale Price of 1 Bond (13th month) = Rs. 1,000 * (1 + 8.76%/12) = Rs. 1,007.30

Long Term Capital Gain (LTCG) = Rs. 1,007.30 – Rs. 1,000 = Rs. 7.30

Long Term Capital Gain Tax = 10.30% of Rs. 7.30 = Rs. 0.7519

HUDCO TFBs post-tax monthly inflow = Rs. 1,007.30 – Rs. 0.7519 = Rs. 1,006.5481 (or Rs. 1,006.55)

If the investment is for 20 years or 15 years?

If your investment is for 20 years, you can either cut down your sale of these bonds by half or you can double your investment, in order to get the same monthly inflows for the next 16 years & 8 months, from next year onwards. You can do it with 15 years option also in a similar way. But, please mind it that to trade in these bonds, you are required to sell at least one bond. So, to have such monthly income for 15-20 years, you need to invest at least Rs. 1,50,000 to Rs. 2,00,000.

What about its annual interest?

I would call it a bonus. You can use it whichever way you want. You can reinvest it next year in any of the investment instruments you want. You can use it for meeting any of your other financial goals. You can go on a holiday with that money. You can use it along with your so called monthly income (sale of these bonds every month).

Basic idea behind it?

It is similar to a systematic withdrawal plan (SWP) of mutual funds. Though it must be clear to you by now, but I want to reiterate it here that the first basic idea behind this way out is to make tax-free bonds comparable to IIFL NCDs like instruments, which are giving 1% monthly interest to its investors throughout its holding period, but the interest is taxable as per the tax slabs of the investors.

The next basic purpose is to make your investment as tax efficient as it is possible. That is why I have suggested here to start selling these bonds from the next year onwards. You are required to pay only 10% tax on your long term capital gains you make by selling these bonds after one year.

If you really require regular inflows from the beginning itself, you can start selling these bonds from the beginning itself. The maximum you would be required to pay in tax in the first year would be exactly equal to the tax you are going to pay on the interest income earned from the IIFL NCDs.

Though I am still unaware of any major fallout of this technique of getting monthly inflows out of our tax-free bond investments, I am sure there must be some. I would like you people to do some brainstorming and find out at least one or two for me, so that we can try to work more on this idea and make it even better, if we can.

Exceptional Piece of Advice.

It is full of useful information. Where I am to look for purchasing tax free hudco bond?

Good solution for monthly payout option. The only think I see which is not considered here is the amount of principal at the end of the tenure.

In case of NCDs, at the end of NCD tenure, one will get the principal amount back. But in case of Tax Free Bonds where one goes for monthly payout (by selling one bond every month), the principal is reduced to “0 (zero)”. How do we factor this in our calculations?

Hi Shiv,

I have one query , would appreciate if you adress it.

I f a person is in 20% Tax Bracket (Annual income 9.95 Lac) and he invest 1 lac in Tax free bond and assume he receives 8000 interest.

Will that guy move to 30 % tax bracket? Will the Tax free interest received be clubbed to his income?

Hi Pramod,

Tax bracket gets ascertained based on your taxable income only. Exempt Incomes, like interest income of tax-free bonds, do not get added for determining your tax bracket. So, in this case, your taxable income will remain 9.95 lac only and Rs. 8,000 would come under exempt income.

Investing in these bonds across companies (leave aside 2 or 3 who have smaller issue size and do not provide appropriate level of liqidity) and holding investment till maturity can be a monthly source of income in itself. Invest 1lac each in 12 issues and you are assured of an approximate annuity of 8000/- per month over 15/20 years. That too tax free!! You will have additional benefit of moving out when the rates decrease and bond price increase (although i am not thinking of moving out at least in initial 10 years).

Over a period of 15/20 year (if one has patience) you will be presented at least with 3 to 4 opportunities where you shall be in a position to reap benefits of price increase.

As for safety of bonds – I think credit risk is close to zero (if not zero).

Hi Jitendra,

I agree to most of your points, except this one that investing in 12 issues will give you income on a monthly basis because not all the companies will pay you interest in different different months. Most of these issues will come in the next six months and most of them will have their interest payment dates during these months only. But, you have shared some good ideas. Thanks a lot for sharing them with us!

dear sir, nice advise for getting monthly cashflow but that’s onlt theory

have you ever tried SELLING on line this types of bonds liquidity is nearly zero in many cases and in at all liquid then one has to sell at a capital LOSS of bonds . is it it surprising piece of adv to be given to a senior citizen just to be more smart and earn some extra income but at cost of loss of peace of MIND. would you like to think it over what is ideal is not practical

Dear Dr. Shetti,

I hold NHAI N2 tax-free bonds in my personal investment holdings and it has been listed for more than one and a half years now. There is no liquidity crunch there, these bonds trade everyday on the stock exchanges and these bonds have never given me capital loss since their listing. I have served many of my clients selling these kind of bonds in the market and have been successful in 99% of those cases.

But, as the interest rates have gone up dramatically in the last 2-3 months, these bonds are on the verge of going into the red zone for the first time. But, that is something market driven. There is no guarantee that these bonds would never give capital losses.

This is just an idea to generate monthly cash inflows from your tax-free bond investments and I am not claiming it to be fool-proof. If it suits the investor, then only one should go for it.

Hi Shiv, thanks for your analysis. One question viz-a-viz Taxation rules:

Is interest earned by Debt Mutual Funds taxable in the hands of Mutual Fund? If not, then imagine al mutual fund that invests in high coupon Bonds and NCDs. Will it not be a vehicle for tax efficient monthly income?

Hi Aditya,

Interest income earned by the mutual funds from their investments in NCDs/Debentures is exempt under the provisions of Section 10(23D) of the I-T Act. Yes, there is an opportunity to use mutual funds as a vehicle to save on the taxes an individual pays on the interest income. I’ll try to work on this idea and lets see if I am able to come out with something useful.

This is a clever thought. I didn’t realize that redeeming IIFL bonds monthly would fetch more income tax. Selling from 13th month onwards is better. Thank you for good writing.

Thanks Himanshu for your motivating words!

Based on your calculation, monthly payment is either Rs 691 or Rs 794 for NCD from 13th month (depends on tax bracket). On the same token, montly payment will be Rs 730 ( Rs 8760/12) for 15 yeras tax free bond.

Instead of selling 1% on monthly basis, get the annual income once a year(after 1st year) and deposit that into a savings account , some savings account even pays 6/7% and withdraw Rs 730 on monthly basis. By this way, one will still have their intial invested money Rs 1 lakh in bond at the end of 15 yeras. Also, not sure how much commision one has to pay for selling 1% every month.

Hi Sundar,

Your points are absolutely valid, but my point is why to reinvest your annual interest in a savings account? It is going to earn you 4%, 6% or maximum 7%. Not all of the investors have their bank accounts in Yes Bank or Kotak Bank. It is better to reinvest your annual interest in tax-free bonds again next year or some other similar or better product(s). If you do that, your principal investment would again get topped up.

Yes, there are brokerage charges on the sale of these bonds, which is a genuine expense.

Still better options, now old bonds listed on exchange , majority has different interest date . Also some are available at good discounts. If tax is not issue then L& T holding is better option.

Thank you for this one.

You are most welcome Austere!

Hi Shiv,

As usual very good article and Nice info. Thanks for putting different prospective here.

My question is while calculation and everthing is OK, do you think it will really work in real senario i mean in terms of liquidity and selling bonds on monthly basis?

Also Senior folks who look for monthly income (say straight forward income without much hassle say post office scheme as you mentioned) does this will not be little tendious work?

regards,

–Kishor

Hi Kishor, thanks for your kind words!

Kishor, I have seen many senior people dabbling in stocks and doing many other things to earn small small returns. If they can stand in lines of post offices for an hour to get their monthly interest, I don’t think it is such a tedious job to sell these bonds on a monthly basis. Also, I don’t think liquidity would be a big problem in big issues like the HUDCO one, if it gets well subscribed.

thanks Shiv.

You are welcome Kishor!

I guess the HUDCO bonds are not listed on bourses so where do you sell those? Also the interest provisions state that the interest would become taxable on secondary ownership so who would want to buy it?

Hi Vikash,

Both your points are incorrect. Previous HUDCO bonds have been listed on the stock exchanges and the current bonds will also get listed on the BSE. Also, the interest payment will remain tax-free, irrespective of the first buyer or the subsequent buyer(s).

Shiva,

Thanks for the clarification. I somehow misread your earlier article comparing HUDCO bonds against IIFL’s about listing. Re-read it now and saw that HUDCO will be listed on BSE.

On the tax-ability of secondary owners – I think I got the wrong impression again – comes on skim-reading rather than reading all details…:)

Thanks again for posting back and clarifying and also for all the article.

Keep writing!

You are welcome Vikash!

is it guaranteed that market value of the bond will be always higher than the F.V irrespective of any economical condition. moreover these bonds are not highly liquidated ,thee will be a huge gap between sell price and buy price on the brouser and LTP may be misleading sometimes

Hi Santonu,

I have not considered any capital appreciation or depreciation while doing this comparison between the cash inflows of HUDCO tax free bonds & IIFL NCDs. I have just added the due interest on a monthly basis. So, yes I have not considered any such guarantee that the market value of these bonds will always be higher than the face value.

I think the higher the issue size is and the higher the rate of interest is, the more liquidity these bonds have. HUDCO issue size is Rs. 4809.20 crore, do you think that it is not possible for these bonds worth Rs. 1 crore to get traded on a daily basis ?? I think there is enough liquidity in the bond market to generate such monthly cash inflows.

thanks Sir

Thanks Santonu!

This is truly great advise, for anyone looking to generate a monthly inflow off your tax free bonds.

Thanks John!