This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Stock markets are going up and as always people are getting excited, disappointed, confused or hyper. Excited, as they are seeing this kind of jump after a very long time and short-term investors have made some real quick money. Disappointed are those who just could not participate and missed this rally. Confused, as they don’t know whether it is the right time to buy stocks or sell their current holdings. Then, there are those who are getting hyper in search of potential multibaggers.

In search of multibaggers and with some quick profits made in the recent issues like Just Dial, Engineers India, Power Grid Corporation, Goldman Sachs CPSE ETF etc., the investors are showing interest in fresh public issues as well. Such an issue has hit the primary markets with Wonderla Holidays Limited, which is one of the largest operators of amusement parks in India.

What is an Amusement park?

Amusement park is the generic term for a collection of rides and other entertainment attractions, assembled for the purpose of entertaining a large group of people, including kids, teenagers and adults. For people like me, who have never visited an amusement park, I would like to name some amusement parks so that we get somewhat familiar with Wonderla’s business model.

Apart from Wonderla Kochi & Wonderla Bangalore, Essel World in Mumbai, Adventure Island (Rohini) & Appu Ghar, both in Delhi, Nicco Park in Kolkata, Ramoji Film City in Hyderabad, Kishkinta in Chennai, Entertainment City in Noida etc. are some of India’s famous amusement parks. Disneyland is the global leader in this business and has presence in many countries, including the United States, Hong Kong, France, Australia etc. Singapore’s Universal Studios is also one of the popular amusement parks.

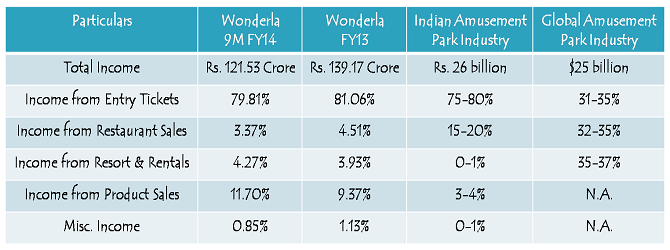

Amusement park industry today is worth about $25 billion globally and continues to stay dominated by the US, contributing almost half of the pie. India has around 150 amusement parks and the industry here is estimated to be worth Rs. 26 billion.

There are three major heads of revenues for amusement parks – (i) Entry Fees, (ii) Foods, Beverages & Merchandising, and (iii) Resort & other rentals. In India, entry ticket sales contribute to a major chunk of the total revenues of amusement parks. Wonderla generated 81.06% and 79.81% of its total income through such entry fees in FY 2013 and the nine month period ending December 31, 2013, respectively.

About Wonderla Holidays Limited

Wonderla Holidays is a company promoted by Kochouseph Chittilappilly and his elder son, Arun Kochouseph Chittilappilly. Kochouseph Chittilappilly is also the promoter of V-Guard Industries Limited, which is a listed company on the BSE and NSE and has given some good returns to its investors since it got listed in 2008.

Wonderla was founded in 2002 and is one of the largest amusement park operators in India. It currently operates two amusement parks, one in Kochi (Kerala) and the other in Bangalore (Karnataka), and the company is in the process of setting up its third amusement park ‘Wonderla Hyderabad’ in Ranga Reddy District of Andhra Pradesh. It also owns and operates a resort in Bangalore, Wonderla Resort, which contributes about 4% in Wonderla’s overall revenues.

Though I have never been to any of Wonderla’s amusement parks, Ketki has visited it in Bangalore and she liked it quite a lot. This is what she has to say about it.

ketki April 17, 2014 at 3:15 pm [edit]

Any views on the upcoming “WONDERLA HOLIDAYS LTD : WONHOL” ipo? opening 21st April…worth a buy ? I personally have visited their park in bangalore and was quite impressed with cleanliness and quality of the park/rides…

Also, I personally found their website to be quite unappealing.

Initial Public Offer (IPO) Details

Initial public offer of Wonderla opened yesterday and is scheduled to close tomorrow i.e. April 23. Wonderla has fixed the price band at Rs. 115-125 per share and is offering 1.45 crore shares during this period. At Rs. 125 per share, the company plans to raise Rs. 181.25 crore in the IPO. As always, 35% of the issue size is reserved for the retail individual investors.

Objective of the Issue – Out of Rs. 181.25 crore, Wonderla plans to use approximately Rs. 173.31 crore to finance the balance of its estimated cost for setting up Wonderla Hyderabad.

IPO Grading – The issue has been graded by CRISIL as 4 out of 5, indicating that the issue is fundamentally above average relative to other listed equity securities.

Risks

* Wonderla has acquired 49.57 acres of land to set up Wonderla Hyderabad, out of which 14.70 acres of land is subject to two litigations. Adverse court ruling will impact proposed development, which may affect operations and financial performance of Wonderla.

* Due to the bifurcation of Andhra Pradesh into two separate states, Wonderla Hyderabad may finally be situated within Telangana. Due to various political as well as socio-economic changes, the company might face certain new restrictions in relation to approvals already obtained.

* Amusement parks are extremely land intensive as large parks require some 40-50 acres of land. Some of the proposed amusement park projects have suffered due to uncertainty in the land acquisition process. With the recently passed bill, land acquisition has become extremely expensive as well as difficult.

* Amusement parks are capital intensive also, as they require huge investments in land, equipments etc. Regularly adding rides to keep visitors’ interest and replacement of existing equipments also require huge funding.

Financials of the Company

(Figures are in Rs. Crore, except per share data & percentage figures)

As on December 31, 2013, the net worth of the company was 152.44 crore as against Rs. 121.45 crore as on March 31, 2013. The net asset value per share as at March 31, 2013 and as at December 31, 2013, stood at Rs. 28.92 and Rs. 36.29 respectively.

As of December 31, 2013, Wonderla’s outstanding indebtedness stands at Rs. 21.02 crore and its debt-to-equity ratio works out to be 0.1 times.

Valuation

Considering annualised profit after tax of Rs. 41.32 crore and post-issue outstanding shares of 5.65 crore, its FY 2014 EPS would stand at Rs. 7.31. At the upper end of its price band i.e. Rs. 125, the offer discounts Wonderla’s annualised FY 2014 earnings by 17.10 times. CARE Research expects revenue of the amusement parks to grow by 15-18% on account of rising footfalls and increased spending on other items like food and beverages, spas etc.

For a growing company, the valuation seems reasonably attractive, but it would take at least 3-4 years for the company to fully utilise the IPO proceeds and generate meaningful returns for its shareholders. So, I think it is an attractive offer for the long-term investors, but short to medium term investors should not expect superfast returns from this IPO.

Hi when will it get listed??

Wonderla Holidays IPO shares to get listed for trading on the exchanges from tomorrow i.e. Friday, May 9th.

Issue reported to be subscribed 38 time, a huge success and likely to yield good listing gain

But due to the huge oversubscription the absolute gains will be very minimal which is what’s typical of all good IPOs.

Day 2 (April 22) subscription figures:

Category I – 35 lakh shares as against 50.75 lakh shares reserved – 0.69 times subscribed

Category II – 11.54 lakh shares as against 21.75 lakh shares reserved – 0.53 times subscribed

Category III – 73.70 lakh shares as against 50.75 lakh shares reserved – 1.45 times subscribed

Total Subscription – 1.20 crore shares as against 1.23 crore shares on offer – 0.98 times subscribed

Day 1 (April 21) subscription figures:

Category I – Qualified Institutional Buyers (QIBs) – 0.64 times

Category II – Non Institutional Investors (NIIs) – 0.21 times

Category III – Retail Individual Investors (RIIs) – 0.28 times

Total Subscription – 0.42 times