This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

General Insurance Corporation of India (GIC Re) IPO Details

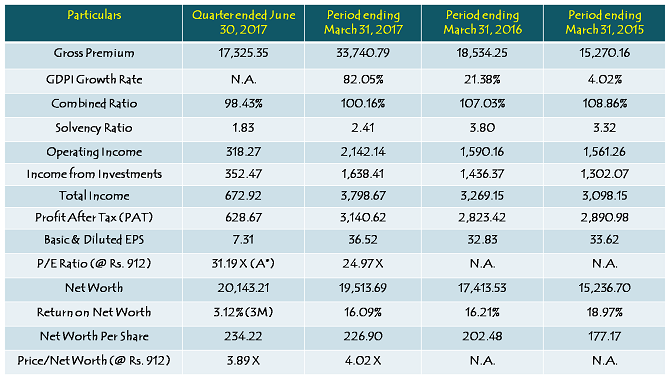

Financials of GIC Re

(Note: Figures are in Rs. Crore, except per share data & percentage figures)

Combined Ratio – This is the measure of profitability which is used to indicate how well underwriting operations are performing. The combined ratio is calculated by taking a percentage of claims incurred (net) divided by premiums earned (net) plus percentage of expenses of management and net commission and then dividing the quotient by net premium. A ratio below 100% indicates that the company is making underwriting income/profits, while a ratio above 100% means that the company is paying out more money than it is receiving from premiums.

Solvency Ratio – This is a regulatory measure of capital adequacy, calculated by dividing available solvency margin by required solvency margin, each as calculated in accordance with the guidelines of the IRDAI on a standalone restated basis. The IRDAI has set a minimum solvency ratio of 1.50.

Should You Invest or Not in GIC IPO?

During financial year 2016-17, GIC reported an operating income of Rs. 2,142 crore, investment income of Rs. 1,638 crore and profit after tax (PAT) of Rs. 3,141 crore, as against Rs. 1,590 crore, Rs. 1,436 crore and 2,823 crore respectively in the previous financial year, registering a growth of 34.72%, 14.07% and 11.26% respectively. The company could manage to deliver such a big jump of 34.72% in its operating income last year, all thanks to an unusually high jump in its gross premium last year, which in turn was the result of the launch of Pradhan Mantri Crop Insurance Scheme.

Is such a high growth sustainable? It doesn’t seem so, as the company has reported a muted set of numbers in the first quarter of the current financial year and the recent slowdown in the Indian economy would make it even tougher for the company to avoid a degrowth in its operating revenues and profitability in the current financial year.

The company reported an EPS of Rs. 36.52 a share as on March 31, 2017 and a net worth of Rs. 234.22 a share as on June 30, 2017, which gives it a multiple of 24.97 times its EPS and 3.89 times its book value. These multiples seem reasonably fair to me as per the current market sentiment. Moreover, recently listed insurance companies, SBI Life, ICICI Lombard and ICICI Prudential, all are trading at multiples higher than that of GIC, but then they are growing at a faster pace as compared to GIC and their growth is relatively consistent as well. So, the premium with which other listed insurance companies are trading relative to GIC seem justified to me.

There are other financials parameters also, which again make it difficult to take a final call to invest in it or not. The company has shown a consistent improvement in its combined ratio, from 108.86% in FY 2014-15 to 98.43% in Q1 of FY 2017-18. However, Solvency Ratio and Return on Net Worth (RoNW) have been on a declining trend during this period, from a high of 3.32 times to 1.83 times as far as Solvency Ratio is concerned, and from 18.97% during FY 2014-15 to 16.09% in FY 2016-17 and 3.12% in Q1 of FY 2017-18.

Finally, investing in this IPO depends on two things – one, what kind of investor you are and two, what is your investment objective with this IPO. I mean if you usually invest in IPOs for making quick listing gains and exit out immediately post listing, then I think this IPO is not for you. I think even in a buoyant market sentiment as it is there in the markets these days, I don’t think GIC should have listing gains of more than 8-10% in this IPO. I think GIC is fairly valued in this price band of Rs. 855-912 and it should consolidate here in the price range of Rs. 800-1000 in the short-term, and should break out of this range only when the company shows some real improvement in its core operating income and profitability.

I think Rs. 45 a share discount is key here and provides a much required margin of safety for the retail investors. Probably in its absence, I would have definitely avoided this IPO. But, its presence has put me in two minds. Still I would skip this IPO and wait for better opportunities to invest in GIC post listing, or pick better companies relatively.

Being a large issue, it’s under subscribed, but I treat it as advantage in comparison to highly sought after IPOs , where even if one is lucky to get allotment, it’s only 1 lot (approx. 15K).

In GIC full allotment as per application is assured, if applied at cut-off.

So even a small gain while listing + retail discountwill offer profit.

There is also a possibility that issue will be revised (less than higher bracket price) before listing and that can increase the profit.

If due to some adverse market condition on listing day, the listing happens at lower price than the purchase, one should hold for some period and price should recover.

Mutual funds are stashed with influx of retail money and they are deploying all that money into newly BB listed quality companies as existing stocks have become expensive.

(Ref to Mutual Fund data , most newly listed good companies are bought by MFs after listing).

Hence there will always be takers for GIC.

Being a large issue, it’s under subscribed, but I treat it as advantage in comparison to highly sought after IPOs , where even if one is lucky to get allotment, it’s only 1 lot (approx. 15K).

In GIC full allotment as per application is assured, if applied at cut-off.

So even a small gain while listing + retail discountwill offer profit.

There is also a possibility that issue will be revised (less than higher bracket price) before listing and that can increase the profit.

If due to some adverse market condition on listing day, the listing happens at lower price than the purchase, one should hold for some period and price should recover.

Mutual funds are stashed with influx of retail money and they are deploying all that money into newly BB listed quality companies as existing stocks have become expensive.

Hence there will always be takers for GIC.

Hi Vasu,

I wish it turns out to be a good IPO for its investors.

Dear Shiv,

Now that the subscription figures are available, what are the chances of listing above Rs. 867 ?

Thanks

Hi TCB,

I think there is a high probability that it would list below Rs. 900, it should not list above that.

Thank you! Both for your analysis and your courage to take a call publicly!

Thanks Hitesh! 🙂

What does Solvency Ratio mean? Thanks

Solvency Ratio – This is a regulatory measure of capital adequacy, calculated by dividing available solvency margin by required solvency margin, each as calculated in accordance with the guidelines of the IRDAI on a standalone restated basis. The IRDAI has set a minimum solvency ratio of 1.50.

Dear Shiv Ji,

Thanks for your timely advise.

I am considering full application as full allotment looks a possibility.

Even if there is a 2-3% gain at listing or in near term the returns will be good considering retail discount.

If not , I will treat it as a long term investment.

So far this year all quality, well known companies did well in IPO Market irrespective of their valuations.

Hopefully this issue should also fetch, with full application amount.

Thanks again for your advice anyway.

Thanks Vasu,

Yes, full allotment is a possibility in this IPO.