This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Gold finance company, Manappuram Finance Limited (MFL), has decided to launch one more issue of its non-convertible debentures (NCDs) from tomorrow i.e. September 15th. The company plans to raise Rs. 300 crore in this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 150 crore. The issue is scheduled to get closed on October 8, 2014.

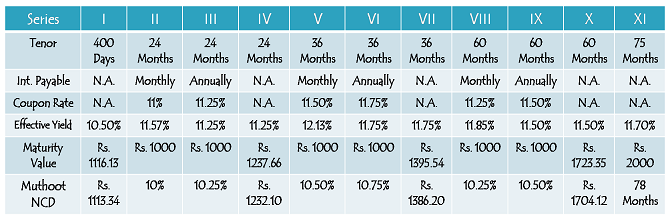

The company is offering XI different options of interest payments with investment periods ranging from 400 days to 75 months and coupon rates falling between 10.50% p.a. to 11.75% p.a. Due to the compounding effect, these coupon rates will result in an effective yield of 10.50% p.a. to 12.13% p.a.

Interest rates offered by Manappuram Finance are 0.75% higher than the rates offered by Muthoot Finance in its NCD issue which is getting closed on September 18. Though both these issues are ‘Secured’ in nature, with this 0.75%, the company is trying to compensate the investors for the extra risk they will have to bear with its NCDs.

Additional 0.25% to Existing Shareholders/Bondholders – The company has decided to reward its existing shareholders and bond investors by offering an additional 0.25% p.a. in respect of Series VI or Series VII bonds. To be eligible for this additional 0.25%, the investors should hold their investments on the record date of interest payment.

“Double Your Money” Option – Like its previous offerings and also with the Muthoot issue, Manappuram is offering to double your investment amount in 75 months. Muthoot is doing it in 78 months and the last time Manappuram came out with its NCDs in December 2013, this duration was 70 months.

Coupon Rates for Non-Retail Investors – Like the last time, Manappuram has kept its interest rate as the same for all categories of investors, retail as well as non-retail investors.

Categories of Investors & Allocation Ratio – The investors would be classified in the following four categories and each category will have the following percentage fixed during the allotment:

Category I – Institutional Investors – 10% of the issue size is reserved

Category II – Non-Institutional Investors including corporates – 20% of the issue size is reserved

Category III – High Networth Individuals including HUFs – 20% of the issue size is reserved

Category IV – Retail Individual Investors including HUFs – 50% of the issue size is reserved

Note: Investors investing Rs. 5 lakh or less will be considered as the retail investors.

NRI Investment – Unlike its previous issue, non-resident Indians (NRIs) are not eligible to invest in this issue.

Ratings & Nature of NCDs – CRISIL has assigned “A+/Stable” rating to this issue which is a notch lower than ‘AA-/Stable’ rating ICRA has assigned to the Muthoot issue and reflects its stable outlook for the issue. However, as mentioned above also, these NCDs are ‘Secured’ in nature and the claims of its investors will be superior to the claims of any unsecured creditors of the company.

Listing, Demat & TDS – Investors have the option to apply these NCDs in physical form as well as demat form and post allotment, these NCDs will get listed on the Bombay Stock Exchange (BSE).

Taken in the physical form, the interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. However, NCDs taken in the demat form will not attract any TDS.

Minimum Investment – The investors will have to put in at least Rs. 10,000 in this issue i.e. at least 10 bonds of face value Rs. 1,000 each.

Should you invest in these NCDs?

Interest rates have already started their move to the southward direction as there is enough liquidity in the system. Banks and deposit-taking NBFCs have also reduced interest rates on their deposits and some of their loans.

With markets going up steadily, the government is trying hard to bridge its fiscal deficit target by selling its stake in some of the bigger PSUs like SAIL, ONGC, Coal India, NHPC etc. Successful stake sale in these companies will help the government control its market borrowings, which in turn will put some more pressure on the interest rates to go down.

Though the market sentiment towards the gold financing business as well as the financial standing of the company has improved slightly as compared to the last time it came out with its NCDs issue, I am not very comfortable making such an investment or advising my clients to invest their money with Manappuram. However, investors with a high risk appetite and in the lower tax brackets may consider investing in this issue as an alternate to company deposits or bank FDs.

Application Form of Manappuram NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in Manappuram NCDs, you can contact me at +919811797407

I AM HOLDING 70 DEBENTURES ISSUED IN SEPTEMBER 2014.TILL DATE I HAVE NOT RECEIVED YEARLY INTEREST WHICH HAS BECOME DUE.