This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

The Finance Ministry on March 31st announced the applicable interest rates for all the Post Office Small Savings Schemes, including PPF, Sukanya Samriddhi Yojana (SSY) and Senior Citizens Savings Scheme (SCSS). Except for SCSS and SSY, the government has kept all other interest rates unchanged, including 8.7% for its most popular scheme, PPF.

To encourage more and more people to get the Sukanya Samriddhi Account (SSA) opened, the Government has decided to ride against the tide and has increased its interest rate to 9.20% from 9.10% earlier, an increase of 0.10%.

As the interest rate on Sukanya Samriddhi Yojana is subject to a revision every financial year, this rate of 9.2% will remain applicable only for the current financial year, 2015-16 and will be further revised in March 2016 for the next financial year, 2016-17.

But, this move of keeping its interest rate higher makes me feel that the Modi Government will continue to keep its interest rate higher going forward as well. I think, like the current financial year, they will try to keep a differential of approximately 0.50% between PPF and Sukanya Samridhi Yojana.

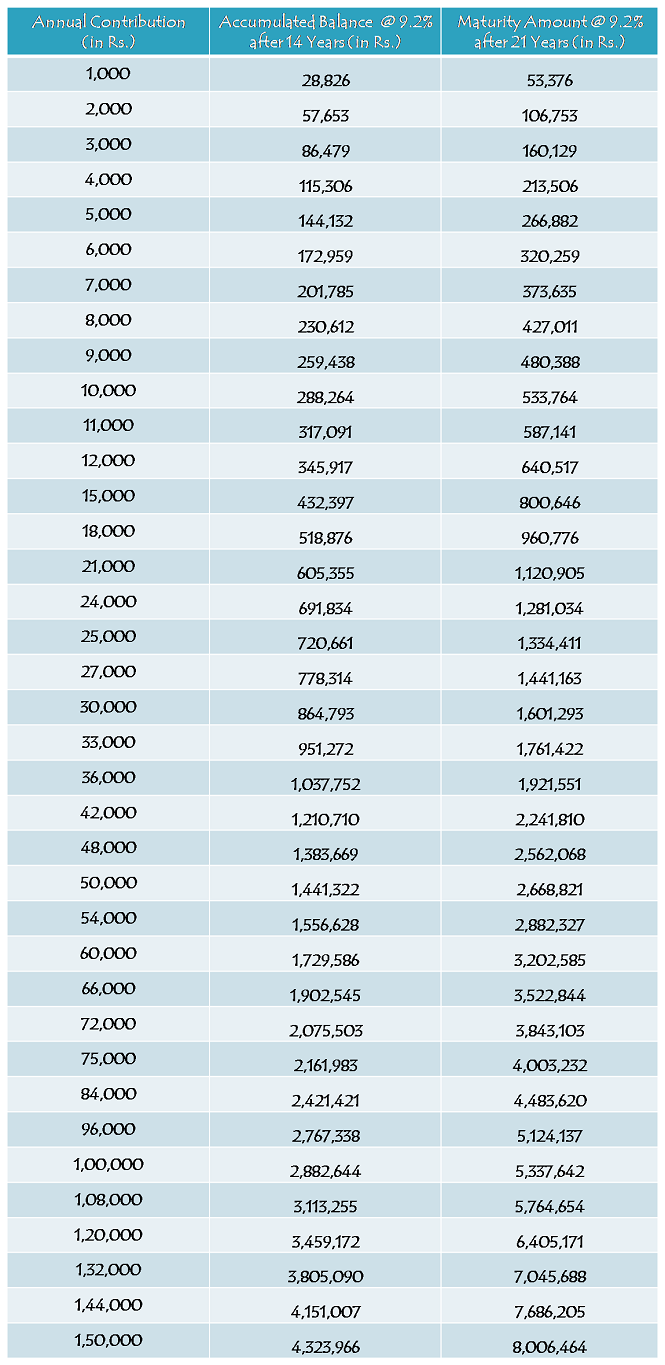

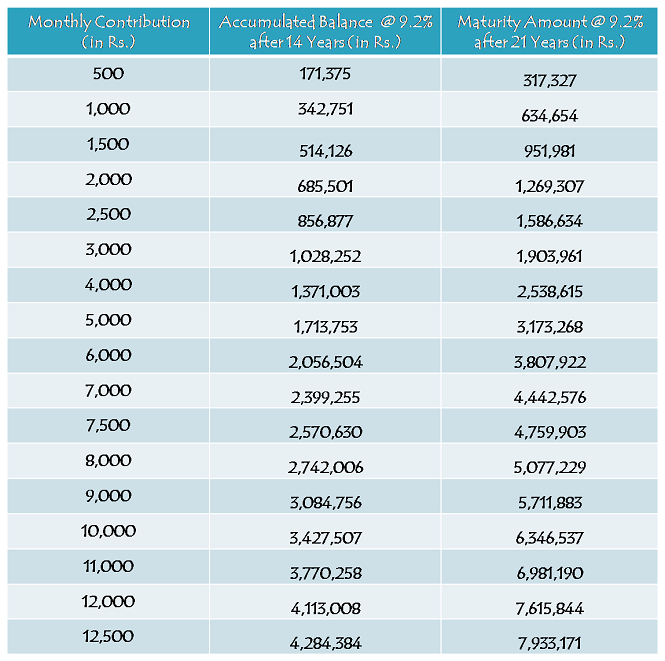

I had posted an article last month in which maturity values were calculated with 9.1% rate of interest throughout its tenure of 21 years. But, as the interest rate has been updated to 9.2% and as most of the investors are yet to open this account, I thought there is a need to have a new post having maturity values calculated as per the new rate of 9.2%.

So, here you have the tables in which maturity values are given as per your annual contributions as well as monthly contributions:

Yearly Contribution Table

Monthly Contribution Table

As different investors will have have different amounts and different timings of their deposits, it is natural that their maturity values will also be different. So, these maturity values are only indicative based on certain assumptions and here you have those assumptions:

* Rate of Interest has been assumed to remain 9.2% for all these 21 years.

* Yearly contributions have been assumed to be made on April 1 every year i.e. the beginning of the financial year.

* Monthly contributions have been assumed to be made on 1st day of every month.

* Although it is not mandatory, a fixed amount of yearly/monthly contribution has been assumed.

* It is also assumed that no withdrawal is made throughout these 21 years.

As people are looking for more and more information about this scheme, I would like to again highlight the main features of this scheme here:

Who can open this account? – Parents or a legal guardian of a girl child up to the age of 10 years, can open this account in the name of the girl child. So, if your daughter is born on or after December 2, 2003, you can get this account opened for her in a post office or an authorised bank branch.

Which documents are required to open this account? – You need birth certificate of the girl child, along with the identity proof, residence proof and two photographs of the parents/legal guardian, to open an account under this scheme. You can approach any post office or a branch of any of the authorised banks to get this account opened.

9.2% Tax-Free Rate of Interest for FY 2015-16 – As mentioned above, this scheme will carry 9.2% rate of interest for the current financial year and it was 9.1% for the previous financial year. Similarly, interest rate will be revised every year in March and will be applicable for the applicable financial year afterwards.

Scheme Matures in 21 years or on Girl’s Marriage, whichever is earlier – The scheme gets matured on completion of 21 years from the date of opening of the account or as the girl child gets married, whichever is earlier. Please note that the girl attaining the age of 21 years has no relevance to maturity period of this scheme.

Deposit for 14 years only – You need to deposit a minimum of Rs. 1,000 and a maximum of Rs. 1,50,000 only for the first 14 years, after which you are not required to deposit any amount. Your account will keep earning the applicable interest rate for the remaining 7 years or till it gets matured on your daughter’s marriage.

NRI/OCI Investment – It is still not clear whether Non-Resident Indians (NRIs) or Overseas Citizens of India (OCI) are allowed to open an account under this scheme or not. But, as it is not allowed with most of the post office small saving schemes, I think the government will not allow them to invest in this scheme either. I’ll update this post as soon as I get any information regarding the same.

Partial Withdrawal – It is allowed to withdraw 50% of the balance for higher education as the girl child attains the age of 18 years. Except for this period, it is not allowed to withdraw any amount during the whole tenure of this scheme.

Nomination Facility – Nomination facility is not there with this scheme. In an unfortunate event of the death of the girl child, the balance amount will be paid to the parents/ legal guardian of the girl child and the account will be closed immediately.

You can check all the features of this scheme from this post – Sukanya Samriddhi Yojana – Tax-Free Small Savings Scheme for a Girl Child

You can also check the updated list of banks and download the application form to open an account from this post – Sukanya Samriddhi Yojana – Updated list of Authorised Banks to Open an Account, Specimen Application Form & Passbook. If you have any query or something related to all these posts, please share it here.

Dear sir Mera acc jis date ko open hua or 1 sal bad same date ko agar kisi karn se jama karne me 1..2 din late ho jaye to or kisi or post office me b jama kar sakte h kya sir

Hi Ravi,

1. Aapko ek financial year mein sirf ek baar amount deposit karna hai, wo aap kabhi bhi kar sakte hain.

2. Aapko paise usi post office mein jama karwaane honge jisme aapka account khula hai.

Thanks for your expert advice.

I am few more queries:-

1. My wife got SSY account opened for my daughter and deposited 1000/ to account (my wife is parent\guardian in my daughter SSY account). Can my wife and myself both can deposit money in my daughters SSY account.

2. My wife is parent\guardian in my daughter SSY account. Can i add my name on my daughter SSY account in future (so that i can avail tax benefits under 80C)

meri bati 8year ki ha 1000 mantly bharana 18year ki hona par kitana milagy kitane year tak bharana padega

Hi Dhokalram,

18 saal ki hone pe balance amount ka 50% hi withdraw kar sakte hain.

hello sir.

meri beti abi 2 month ki hai agar me 10000 sal ka kawata hu to meje 21 sal bad kitna milega sia.

Hi Harjinder,

As per the table above, the maturity amount would be approximately Rs. 533,764 @ 9.2% per annum.

Is it mandatory to stop the investment after 14 years or shall we continue investment for 21 years. If yes then how would be the returns if the deposit is 5k per month.My daughter is 4 months old.

Hi Dinesh,

You cannot deposit money beyond 14 years.

How can we apply please send instructions

You need to visit an authorised bank branch or a post office, they will guide you the complete procedure.

Thanks for helping with your answers. My daughter is 8 years old. I have few questions on SSY on which i need your expert advice:-

a. We need to deposit contribution for period of 14 years i.e. till my daughter 22 years old. Is my understanding correct.

b. Till what date in month can I deposit contribution, so that I can earn interest for full month.

c. if my daughter gets married at age of 26 years, account is required to be closed. Can we use maturity proceeds for her marriage expenditures or we need to spend money from your savings.

Thanks

Thanks Saurabh,

a. That’s Right.

b. Till 5th of every month.

c. Your daughter can withdraw the balance amount before her marriage in order to meet her marriage expenses.

Dear sir,

I am working out of country not for permanent, but only for 5 to 6 yes,

Am I go for this scheme?

Thanks,

Hi Nirav,

Only Resident Indians are eligible for this scheme.

Maheshji, aapki beti ko 21 saal baad approximately Rs. 634,654 milenge @ 9.20% per annum.

meri beti 4 year ki 1000 month deposit karunga to 21 years ke baad kitne milenge

Sir meri beti ki age 04 sal h mai 14 sal tak 2000 month jama karte h. Jab meri beti ki age 21 sal ki hogi to hume kitne rupaye milege.

Shiv Prasadji, aapki beti ko uski age 21 saal hone pe nahin, uski marriage hone pe ya account khulne ke 21 saal baad balance amount milega.

Dear sir,meri beti 3.5 saal ki hai, main har mahine suknya samridhi yojna me 1500 rupey jama karunga, toh 21 saal k baad kitne rupey meri beti ko milenge, please reply

Pankajji,

Upar pasted table ke according aapki beti ko Rs. 951,981 milenge.

Thank you Shiv Kukreja ji

Sir isme jese 14 sal dene ke bad 50%paise wapis mil jate h agr wo le le to 21 sal bad kitne paise milege

Ye annual rate of interest pe depend karega.

Sir agr parents ki death ho jati h to paisa kb milega kisko milega or kitna milega

Parents ki death hone pe beti balance amount immediately nikaal sakti hai. Amount kitna hoga, ye time of withdrawl pe depend karega.

Sir meri ki dob 13/10/2011 h.mene is scheeme me uska khata kulwa dia h.sir mene shuru me 1000 rs jma krwae h .sir jese mene phle sal 1000 rs jma krwae h or me agle sal 2000 rs jma krwata hu to age b muje 2000 hi jma krwane h ya me km jydav krwa skta hu.

Hi Devi Dayal,

Aap kam ya zyaada paise jama karwa sakte hain.

Sir meri beti ki age 3 years h aur har mahine 2 thousand rs jama karta hu tuo kitne saal tak jama karni hoge aur kitna amount milage beti ko air sir kya net banking ke through account check kar sakta hu kya pls give ans

Hi Deepak,

Aapko 14 saal paisa deposit karna hoga, yaani 2029 tak. Maturity value ke liye upar pasted table check keejiye. Aapko apne bank se check karna hoga ki wo net banking facility provide kar rahe hain ya nahin.

Hi

Sir good morning

Nice sehecm ssy

sM samjhna cjahta hu meri beti ka age 08 year hai. agar suknya yojna 40000/- Per month paid krta hu to use sadi me time kitna pais milega.

sM samjhna cjahta hu second meri beti ka age 06 year hai. agar suknya yojna 40000/- Per month paid krta hu to use sadi me time kitna pais milega

Satendraji, is scheme mein Rs. 40,000 per month deposit nahin kar sakte.

sir if girl is expired in accident what is the scheme stage

I didn’t get your query.

sir agar account kulne kai baat mai kuch years baat rupay nahi bhar payi to mere deposite ke gaye rupay duub jayge please tall me

Aapke paise boobenge nahin, but account inactive ho jaayega.