This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

India Infrastructure Finance Company Limited (IIFCL) is back again to offer its tax-free bonds and as expected this time, it is carrying higher rate of interest for all the maturity periods. The issue is getting opened for subscription from Monday, 9th of December and is scheduled to get closed along with the HUDCO 9.01% issue on January 10th, 2014, which is a Friday.

Size of the Issue – IIFCL raised Rs. 1,213.01 crore from its Tranche I issue in October and plans to mop up another Rs. 3,000 crore from this issue, including the green shoe option of Rs. 2,000 crore.

If the company is able to successfully raise its target amount of Rs. 3,000 crore from this issue, then it plans to launch its Tranche III issue sometime in January again.

Categories of Investors & Allocation Ratio – Investors have been categorised in the four usual categories and the percentage allocation has been the same as it was in IIFCL’s first issue:

Category I – Qualified Institutional Bidders (QIBs) – 15% of the issue is reserved i.e. Rs. 450 crore

Category II – Non-Institutional Investors – 20% of the issue is reserved i.e. Rs. 600 crore

Category III – High Net Worth Individuals including HUFs – 25% of the issue is reserved i.e. Rs. 750 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 1,200 crore

NRIs Ineligible to Invest – Once again, IIFCL has not allowed Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) to participate in this issue.

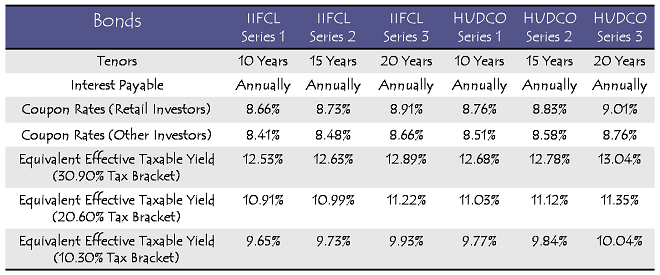

Coupon Rates on Offer – Coupon rates in this issue are absolutely same as those got offered in the NTPC issue – 8.91% per annum for the 20 year option, 8.73% per annum for the 15 year option and 8.66% per annum for the 10 year option.

These rates are applicable for the retail investors investing Rs. 10 lakh or below. All other investors will see a cut of 25 basis points or 0.25% per annum for the respective maturity periods.

Rating of the Issue – Like its previous issue, IIFCL Tranche II issue is also ‘AAA’ rated. CARE, ICRA, Brickwork Ratings and India Ratings, all these four rating agencies have assigned their highest credit rating to this issue.

These bonds are again ‘Secured’ in nature as certain receivables of the company will be charged equivalent to the outstanding amount of the bonds.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchange.

Listing – IIFCL will get these bonds listed only on the Bombay Stock Exchange (BSE). As required by the listing rules of the SEBI, the company has committed to get the bonds allotted and listed within 12 working days from the closing date of the issue.

No Lock-In Period – As these bonds are freely tradable, an investor may sell them on the BSE whenever he/she wants after these bonds get listed on the exchange. That is how these bonds do not carry any lock-in period.

Demat/Physical Option – Though these bonds are tradable if taken in the demat form, investors have the choice to subscribe for these bonds in physical form as well, if they don’t have a demat account or they don’t want to take these bonds in the demat form.

Interest on Application Money & Refund – IIFCL will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum Investment – Investors are required to invest a minimum of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each.

Interest Payment Date – IIFCL has not fixed the date of interest payment for this issue as yet. It has decided to pay its first due interest exactly one year after the deemed date of allotment.

NTPC issue, which got closed on Thursday, received an overwhelming response from all the categories of investors. As IIFCL is offering coupon rates absolutely same as those offered by NTPC, it is very much clear that these tax-free interest rates are very attractive.

Though I don’t expect this issue to get subscribed as fast as the NTPC issue, the investors, who missed out on the NTPC issue and/or want to invest only in ‘AAA’ rated securities, I think this issue offers a very good opportunity.

Also, a number of macro economic data is expected to get released sometime next week here, such as trade deficit for the month of November, IIP growth figures, CPI inflation, WPI inflation etc. This data will be very crucial for the RBI Governor Dr. Raghuram Rajan to take his final decision for the RBI’s monetary policy of December 18th.

One more rate hike would once again ruin the mood of the market participants in the bond markets and result in a jump in the G-Sec yields. Investors should keep a close eye on all these events also.

Application Form of IIFCL Tax Free Bonds

IIFCL Tax-Free Bonds – Bidding Centres

IIFCL Tax-Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IIFCL tax-free bonds, you can contact me at +919811797407

Day 13 (December 26) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 592.80 crore as against Rs. 600 crore reserved

Category III – Rs. 619.86 crore as against Rs. 750 crore reserved

Category IV – Rs. 970.30 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,618.14 crore as against total issue size of Rs. 3,000 crore

IRFC has also announced it now. Their IPO opens from jan 6. I hope the interest rate will be as good as NHB or better

As Shiv has already posted , IRFC coupon Rates are 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. No 20 year option

Day 12 (December 24) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 580.66 crore as against Rs. 600 crore reserved

Category III – Rs. 617.80 crore as against Rs. 750 crore reserved

Category IV – Rs. 950.56 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,584.21 crore as against total issue size of Rs. 3,000 crore

Here are the links to the NHB Prospectus and the application forms:

http://www.nhb.org.in/Whats_new/NHB-Prospectus-Tranche-I.pdf

http://www.akstockmart.com/akintra/BA/DNLDFORM.aspx?refno=dU6gu20m1nc=

Hi Shiv,

I’m also surprised at rate of 9.01% for AAA rated bond. I will def go for this issue because future rates might not be as good as this.

That’s Great !!

National Housing Bank (NHB) Tax-Free Bonds issue opens on December 30th. Coupon Rates – 8.51% for 10 years, 8.88% for 15 years and 9.01% for 20 years. It is a ‘AAA’ rated issue and closes on January 31, 2014. I am pleasantly surprised with the coupon rates.

can u provide the link to this? Is this news confirmed?

Here are the links to the NHB Prospectus and the application forms Sam:

http://www.nhb.org.in/Whats_new/NHB-Prospectus-Tranche-I.pdf

http://www.akstockmart.com/akintra/BA/DNLDFORM.aspx?refno=dU6gu20m1nc=

What is the issue size? How much is reserved for category 4?

The issue size is Rs. 2,100 crore and 40% of the issue is reserved for Category IV i.e. Rs. 840 crore for the retail investors investing Rs. 10 lakh or less.

I will stick with IIFCL as 20 years is a long time. If it was IRFC at 9.01% p.a. I would have jumped to apply.

Did not get the full meaning of your comment .. can you please elaborate

Do you mean to say that NHB is less acceptable than IIFCL or IRFC? Considering that it is a bank owned by RBI, there is good control by RBI and the fundamentals are also good. IIFCL and IRFC are also having the same level or more risk compared to NHB. For example IIFCL pumps huge funds in few projects and risk is high and return is low. NHB funding goes to many banks and housing projects and the NPA need not go that high. IRFC finances projects of Indian Railways. The bond is issued by IRFC and not Indian railways. If you think it is better to put money for 10 years, I will go with you considering that IIFCL is giving 8.66%. But I fail to understand why you feel it is better to invest for 20 years in IRFC.

I agree with George here also.

Even I did not get it. NHB is a wholly-owned subsidiary of the RBI and I trust RBI more than any other regulator or any other company, even more than the government.

This is really Good news. Some how the news has not reached news papers. NHB uploaded the prospectus in their website. I am sure NHB TF will have more takers for 15years bond compare to other issues. There is a 37 BP difference from 10 years to 15 years and just 13 BP from 15 to 20 years. I felt the 10 years bond should have been 8.66%. But since the pricing is related to Govt Securities, I am sure they could not fix anything above 8.51 considering that the 10 years security was trading between 8.7 to 9% recently. My gut feeling is that this bond also will get subscribed in 1-2 days time considering the size , coupon rate and strength of NHB.

I agree with you George, this issue should get subscribed quite soon, but not as soon as 1-2 days. Let’s see.

Day 11 (December 23) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 573.56 crore as against Rs. 600 crore reserved

Category III – Rs. 613.94 crore as against Rs. 750 crore reserved

Category IV – Rs. 921.46 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,544.14 crore as against total issue size of Rs. 3,000 crore

Today’s subscription numbers please 🙂

Hi Shiv

To-days position in category II – as on Dec. 20 – Rs. 562.05 crores against Rs. 600 crore reserved.

What you think if I apply for Rs. 10 Lac to-morrow , suppose the subscription is oversubscribe in categoey II on Monday then i will get the partial allotment and if not fully subscribe up to Rs. 600 crore then i will get the full allotment.

Hi Shiv,

Does the investment in this bond come under Section 80CCF or Section 80C for tax implications ?

Thanks,

Adak

Hi Adak,

No, investment in these bonds is not eligible for 80CCF or 80C deduction. Deduction u/s. 80CCF is history now. Only the interest income is tax-free with these bonds.

IRFC issue to get launched on January 6th. Coupon Rates are 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. 20 years option not available. The issue closes on January 20th.

Hi Shiv

Thanks for the information. It is very disappointing that IRFC is not giving a 20 year option and interest rates are much lower. I feel they missed the bus to come up with the issue at the right time.

I hope NHB which opens on Dec-30 will be able to come up with better coupon rate

Regards

Ramadas

Yes, it is very disappointing Ramadas! Also, as IRFC’s coupon rates are out now, I think NHB’s coupon rates would be even lower than that of IRFC and that would be more disappointing. Both companies have missed the bus.

Any reason why NHB coupon rates would be lower than that of IRFC? And does that mean that now IIFCL will close very fast?

Since inflation is widely expected to tick lower in January, NHAI issue seems already doomed to fail.

I think NHB has filed its draft prospectus quite late and since then the G-Sec yields have been moving lower only. That is the reason I think its rates would be lower than IRFC. I think IIFCL issue should get closed in the next 5-8 days time.

You are spot on. The GSec is are trading with lower yield following RBI and Fed decisions.

Many of the investors were waiting for higher interest bonds and with the announcement of IRFC that expectation is taken care. Monday IIFCL and HUDCO will have more takers and the bonds will close in a day or 2. We can expect lower coupon rates for NHB, NHAI bonds. Considering that banks also started reducing the lending rates for housing loans the chances of bond coupon rates going up is limited.

Hi Shiv

Looking at the draft prospectus of NHB , they have a 20 year option unlike IRFC. Assuming same interest rates as IRFC , may be 20 year option of NHB will be priced at 8.71%. Hope it doesnt go below that

Regards

Ramadas

Hi Ramadas,

Yes, there exists this possibility, but then it would be lower than 8.91% which ‘AAA’ rated IIFCL is currently offering and 9.01% which ‘AA+’ rated HUDCO is offering. Why not go for IIFCL or HUDCO then, if you haven’t already ??

Hi Shiv

I have applied to both IIFCL and HUDCO in earlier issues and current issue.

I was looking for IRFC and NHB to diversify my TFB holdings. I am a bit concerned in concentration risk in a particular sector in infrastructure whether it is power or housing. IRFC caters to railways which is different infrastructure sector compared to rest of sectors which IIFCL lends to. NHB being a bank itself offers another diversification oppurtunity. In fact , the subscription levels of NHPC and NTPC shows this diversification interest.

20 year bonds is a long time frame and you never know what will happen to current AAA companies in that time frame. ITI , HM , HMT are all classic examples. Thought of not putting all eggs in one basket.

Regards

Ramadas

Hi Ramadas,

Your thoughts are noble and correct also.

Day 10 (December 20) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 562.05 crore as against Rs. 600 crore reserved

Category III – Rs. 598.72 crore as against Rs. 750 crore reserved

Category IV – Rs. 878.30 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,474.25 crore as against total issue size of Rs. 3,000 crore

Thanks Shiv

You are welcome Aditya!

Also, I got your mail in the afternoon today, but could not respond to it. I’ll do that soon.

Ok no problem Shiv

Could you please reply to my mail Shiv ? depending on that i will have to plot the next strategy

It just skipped my mind today Aditya. I’ll do that sometime tomorrow for sure.

Thanks for the replying to my mail Shiv

You are welcome Aditya!

Hi Shiv

NHB TFB opening on Dec-30 as per latest report from businessline.

http://www.thehindubusinessline.com/industry-and-economy/banking/nhb-taxfree-bonds-issue-to-open-on-dec-30/article5482796.ece

What is your guess on interest rate? Will it be higher or lower than IIFCL?

Regards

Ramadas

Hi Ramadas,

It is very difficult to guess NHB’s coupon rates as the G-Sec yields have been quite volatile for the past 4-5 days. I would like not to do that this time.

Can you tell if this would be AAA or AA or less? How were past tfb issued by NHB rated?

NHB is a reserve bank of India subsidiary and a regulator for housing finance companies. Nothing less than AAA for NHB for sure

Regards

Ramadas

Yes, that’s absolutely correct! I would have replied in a similar manner. NHB issue is ‘AAA’ rated by CRISIL, CARE and ICRA. Thanks Ramadas!

NHB will give an opportunity to diversify the portfolio considering that it is a housing finance bank controlled and owned by RBI. Checking on the fundamentals of NHB, I found that they are having negligible NPA.

Some info which gives a birds eye view of their strength is give below which I have managed by Goggling. Over all my impression is that NHB will get fast subscribed like NHPC and NTPC considering that the fundamentals are better. While Shiv is making detailed analysis , I hope this will help some of you.

“On an overall basis, NHB’s Gross NPA% increased from 0.01% as on June 30, 2012 to 0.53% as June 30, 2013 on account of one large project exposure slipping into NPA category. NHB’s gearing has increased over last two years as balance sheet growth (24% in 2012-13 and 22% in 2011-12) was far in excess of internal capital generation (around 12% over last two years). NHB’s capitalisation (CRAR of 16.59% as on June-2013) is adequate in relation to risk profile of its portfolio. Further, its ability to get capital, in case of need, is relatively high in light of its strategic importance to the Government of India (GoI).”

I found that they also have a good Asset base when considering there exposure. NHB reported a net profit of Rs. 450 crore over an asset base of Rs. 38,721 crore for the year 2012-13*,as compared with a net profit of Rs. 387 crore over an asset base of Rs. 31,332 crore for the year 2011-12. NHB reported gross NPA% of 0.53% and net NPA% of 0.45% as on June 30, 2013. NHB’s capital adequacy was 16.59% as on June 30, 2013.

Thanks George for this detailed analysis !!

Inflation bonds have opened. can you provide details ?

Hi Pradeep,

I’ve started writing about it. I’ll post it either today or tomorrow.

great sir. Good work 🙂

Has IRFC filed its prospectus? How much time does a company get to open the issue after filing the prospectus?

Hi Simple,

IRFC filed its draft shelf prospectus a couple of days before NTPC did it. While NTPC issue got opened, got subscribed, got allotted and got listed also, IRFC is yet to file their final prospectus.

I’ve observed that normally it takes 15-25 days for a company to launch its issue after filing its draft shelf prospectus.

Ok Shiv. Thank You!

You are welcome!

NHAI to launch its tax-free bonds issue sometime around mid-January.

http://www.thehindubusinessline.com/markets/nhais-taxfree-bond-issue-to-hit-market-in-midjan/article5478623.ece

Day 9 (December 19) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 537.01 crore as against Rs. 600 crore reserved

Category III – Rs. 590.43 crore as against Rs. 750 crore reserved

Category IV – Rs. 849.11 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,411.73 crore as against total issue size of Rs. 3,000 crore

Hi Shiv,

One question – I have already invested 5 lacs in Cat 4 in IIFCL Bonds. Can I invest 5 lacs more since the Cat 4 is still not oversubscribed ? Will my application get rejected for multiple applications even though the total is not more than 10 lacs ?

Thanks,

Gaurav

Hi Gaurav,

No, your application(s) won’t get rejected. You can submit multiple applications up to any investment amount you want. To get higher rate of interest applicable only to the retail investors, the investment amount should not be more than Rs. 10 lakh.

So, if I invest 5 lacs more then I will still get the higher interest rate. right ?

Yes, that’s right.

ok, one more question. Do you think RBI decision to not increase key rates yesterday will decrease the coupon rates for IRFC and other TFBs coming in the future ?

It depends on the timing of these issues. If IRFC files its final prospectus quickly, then I think the rates would be similar or probably higher than the current issue of IIFCL. But, if they delay it further and by that time G-Sec yields fall further from here, then you’ll get lower coupon rates in the upcoming issues.

Hi Shiv

If I apply to day Rs 10 Lac in category I I. , I think I will get the full allotment because as on December 18 category II – Rs. 530.83 crore as against Rs. 600 crore reserved

Yes, that’s right Paresh!

Day 8 (December 18) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 530.53 crore as against Rs. 600 crore reserved

Category III – Rs. 578.51 crore as against Rs. 750 crore reserved

Category IV – Rs. 815.78 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,359.99 crore as against total issue size of Rs. 3,000 crore

It is getting boring 🙂 🙂 This issue is crawling now

🙂 You want it to be like the NTPC issue or NHPC issue ??

Its delaying my allotment and since i am a first time TFB investor, i am sort of getting impatient 🙂

oh ok… I see. Then you have all the rights to be impatient !! I must say you would be very excited on the date of its listing.

Hi Shiv,

I have invested the refund amount from NTPC in the IIFCL bonds, hope that I’ll get the full allotment?

thanks,

Hemant

Yes Hemant, you’ll get the full allotment.

thanks Shiv.

You are welcome!