This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

India Infrastructure Finance Company Limited (IIFCL) is back again to offer its tax-free bonds and as expected this time, it is carrying higher rate of interest for all the maturity periods. The issue is getting opened for subscription from Monday, 9th of December and is scheduled to get closed along with the HUDCO 9.01% issue on January 10th, 2014, which is a Friday.

Size of the Issue – IIFCL raised Rs. 1,213.01 crore from its Tranche I issue in October and plans to mop up another Rs. 3,000 crore from this issue, including the green shoe option of Rs. 2,000 crore.

If the company is able to successfully raise its target amount of Rs. 3,000 crore from this issue, then it plans to launch its Tranche III issue sometime in January again.

Categories of Investors & Allocation Ratio – Investors have been categorised in the four usual categories and the percentage allocation has been the same as it was in IIFCL’s first issue:

Category I – Qualified Institutional Bidders (QIBs) – 15% of the issue is reserved i.e. Rs. 450 crore

Category II – Non-Institutional Investors – 20% of the issue is reserved i.e. Rs. 600 crore

Category III – High Net Worth Individuals including HUFs – 25% of the issue is reserved i.e. Rs. 750 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 1,200 crore

NRIs Ineligible to Invest – Once again, IIFCL has not allowed Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) to participate in this issue.

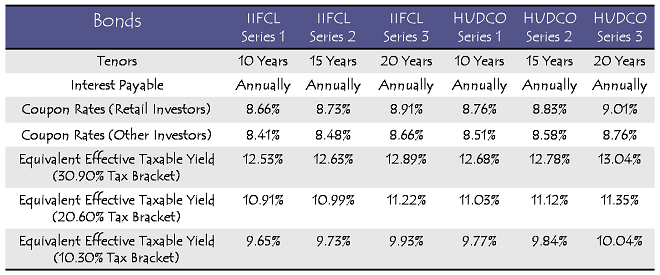

Coupon Rates on Offer – Coupon rates in this issue are absolutely same as those got offered in the NTPC issue – 8.91% per annum for the 20 year option, 8.73% per annum for the 15 year option and 8.66% per annum for the 10 year option.

These rates are applicable for the retail investors investing Rs. 10 lakh or below. All other investors will see a cut of 25 basis points or 0.25% per annum for the respective maturity periods.

Rating of the Issue – Like its previous issue, IIFCL Tranche II issue is also ‘AAA’ rated. CARE, ICRA, Brickwork Ratings and India Ratings, all these four rating agencies have assigned their highest credit rating to this issue.

These bonds are again ‘Secured’ in nature as certain receivables of the company will be charged equivalent to the outstanding amount of the bonds.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchange.

Listing – IIFCL will get these bonds listed only on the Bombay Stock Exchange (BSE). As required by the listing rules of the SEBI, the company has committed to get the bonds allotted and listed within 12 working days from the closing date of the issue.

No Lock-In Period – As these bonds are freely tradable, an investor may sell them on the BSE whenever he/she wants after these bonds get listed on the exchange. That is how these bonds do not carry any lock-in period.

Demat/Physical Option – Though these bonds are tradable if taken in the demat form, investors have the choice to subscribe for these bonds in physical form as well, if they don’t have a demat account or they don’t want to take these bonds in the demat form.

Interest on Application Money & Refund – IIFCL will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum Investment – Investors are required to invest a minimum of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each.

Interest Payment Date – IIFCL has not fixed the date of interest payment for this issue as yet. It has decided to pay its first due interest exactly one year after the deemed date of allotment.

NTPC issue, which got closed on Thursday, received an overwhelming response from all the categories of investors. As IIFCL is offering coupon rates absolutely same as those offered by NTPC, it is very much clear that these tax-free interest rates are very attractive.

Though I don’t expect this issue to get subscribed as fast as the NTPC issue, the investors, who missed out on the NTPC issue and/or want to invest only in ‘AAA’ rated securities, I think this issue offers a very good opportunity.

Also, a number of macro economic data is expected to get released sometime next week here, such as trade deficit for the month of November, IIP growth figures, CPI inflation, WPI inflation etc. This data will be very crucial for the RBI Governor Dr. Raghuram Rajan to take his final decision for the RBI’s monetary policy of December 18th.

One more rate hike would once again ruin the mood of the market participants in the bond markets and result in a jump in the G-Sec yields. Investors should keep a close eye on all these events also.

Application Form of IIFCL Tax Free Bonds

IIFCL Tax-Free Bonds – Bidding Centres

IIFCL Tax-Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IIFCL tax-free bonds, you can contact me at +919811797407

Day 7 (December 17) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 523 crore as against Rs. 600 crore reserved

Category III – Rs. 565.01 crore as against Rs. 750 crore reserved

Category IV – Rs. 775.36 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,298.55 crore as against total issue size of Rs. 3,000 crore

Do you feel that maybe a possibility of a higher coupon in forthcoming issues is slowing down the current HUDCO and IIFCL issues ?

Some retail/HNI investors are still investing, whereas some smarter retail/HNI investors, who expect higher rates in the upcoming issues, have opted not to put money in these two issues. They are waiting for the IRFC and NHB issues to make their investments.

sir, i saw the news that RBI has not hiked rates. will IRFC come with higher coupon rate or not ?

That is what only time will tell Pradeep, but the unchanged stance of the RBI w.r.t. the policy rates is a very welcome move. People, who were waiting for the higher rate issues to invest in these tax free bonds, should now deploy at least some portion of their investment in the current issue of IIFCL tax-free bonds.

Day 6 (December 16) subscription figures:

Category I – Rs. 435.18 crore as against Rs. 450 crore reserved

Category II – Rs. 521.74 crore as against Rs. 600 crore reserved

Category III – Rs. 553.15 crore as against Rs. 750 crore reserved

Category IV – Rs. 728.23 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,238.30 crore as against total issue size of Rs. 3,000 crore

I had applied for the NTPC bonds on the first date of issue and I have also got full allotment as assured by you.

That’s Great !! 🙂

Hi,

All those who applied for NTPC TF Bonds. The allotment of bonds happened today.

Thanks George for the info !! You’ve got the bonds credited to your account or you’ve some other source of info?

Yes that’s right. 100% allotment.

That’s Great!

Thanks Shiv anyways 🙂

You are welcome Anil!

Hi Shiv,

I had a question regarding long term savings. I was wondering if I should invest in long term debt funds or should I invest in these bonds?

Instead of paying for an LIC policy, I could invest every year in a bond/debt mutual fund.

For example, I want money by 1st Jan 2030, then I would start investing every year from now. If there are no bonds available, I could buy in secondary market.

My question is:

Would I be better off investing in long term debt funds or bonds?

Hi Anil,

It is like a personal query, which I won’t like to respond to here on this forum. I’ll try to do a post on the same though.

For the benefit of illiterate 🙂 investors like me , you might also want to include FDs in that comparison if you do a post.

For the benefit of illiterate investors 🙂 like me , you might want to add FDs also in that comparison

I think FDs don’t stand anywhere near these tax-free bonds, except only a couple of benefits – 1. your investment is insured up to Rs. 1 lakh and 2. the interest gets compounded quarterly.

But, still I’ll try to keep FDs in the comparison table.

Day 5 (December 13) subscription figures:

Category I – Rs. 435.08 crore as against Rs. 450 crore reserved

Category II – Rs. 505.97 crore as against Rs. 600 crore reserved

Category III – Rs. 540.71 crore as against Rs. 750 crore reserved

Category IV – Rs. 660.83 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 2,142.59 crore as against total issue size of Rs. 3,000 crore

Looks like new issue like IRFC will be open after this IIFCL closes 🙁

Ya, no issues lined up in the next 10 days at least, except IRFC.

sir,

when is IRFC opening ? i wnat to withdraw from iifcl and opt for irfc as interest rates are expected to be higher 😉

IRFC issue is expected to get launched anytime on or after December 23rd.

Hi Shiv

I am going to submit my application for 1000 Bonds for IIFCL Bonds / 20 Years /. Coupon rate 8.66 %. In category. II ( as my status is A. O. P. )

As on Day 4 / December 12 in category. II. – Rs. 479.94. Crore as against. Rs. 600 crore reserved

So as per my thinking I will get the full allotment if Rs. 600 crore is not filled to-day

Hi Paresh,

It is obvious that you’ll get full allotment if Category II does not get fully subscribed by 5 p.m. today.

Day 4 (December 12) subscription figures:

Category I – Rs. 365 crore as against Rs. 450 crore reserved

Category II – Rs. 479.94 crore as against Rs. 600 crore reserved

Category III – Rs. 530.08 crore as against Rs. 750 crore reserved

Category IV – Rs. 602.45 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 1,977.47 crore as against total issue size of Rs. 3,000 crore

Hi Shiv,

I can’t find out the reason behind delay of IRFC tax free bonds issue. This was suppose to come before NTPC.

Same here Ikjot. Somebody should call IRFC management and ask them.

i read in businessline website, the issue will be in dec-jan.

Day 3 (December 11) subscription figures:

Category I – Rs. 355 crore as against Rs. 450 crore reserved

Category II – Rs. 440.52 crore as against Rs. 600 crore reserved

Category III – Rs. 492.46 crore as against Rs. 750 crore reserved

Category IV – Rs. 525.89 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 1,813.88 crore as against total issue size of Rs. 3,000 crore

Less of a retail interest and more in other categories here , exactly opposite of HUDCO 🙂

When, according to you Shiv, will this get closed ?

I am a first time TFB investor and would be happy only when i see the bonds in my demat account 🙂

It should take at least 5-7 working days for it to get closed.

My broker left out 1 small thing in the form – he did not tick the category (point no 2). According to him, it should not cause any problem as the category can be determined from the PAN number. All other details, including the Series in which the bonds are applied is correct.

Will my application still fail ?

I don’t know but I don’t think it should. I don’t find any reason for it to fail.

Please send me if any comments on this bond

Day 2 (December 10) subscription figures:

Category I – Rs. 355 crore as against Rs. 450 crore reserved

Category II – Rs. 404.64 crore as against Rs. 600 crore reserved

Category III – Rs. 446.25 crore as against Rs. 750 crore reserved

Category IV – Rs. 431.29 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 1,637.19 crore as against total issue size of Rs. 3,000 crore

This issue is getting a better response as compared to the HUDCO issue.

Hi Shiv

Do you know what is causing delay in IRFC TFB Issue? IRFC had filed prospectus with SEBI a week before NTPC and there is no sign of IRFC bonds yet. Also , do you know if NHAI will raise money at all through tax free bonds this year?

Regards

Ramadas

Hi Ramadas,

It is almost certain that NHAI will issue tax-free bonds this financial year. It has already appointed Book Running Lead Managers (BRLMs) for the issue.

But, I am not sure why IRFC is delaying it. It should have launched its issue by now.

Day 1 (December 9) subscription figures:

Category I – Rs. 55.40 crore as against Rs. 450 crore reserved

Category II – Rs. 306.17 crore as against Rs. 600 crore reserved

Category III – Rs. 380.03 crore as against Rs. 750 crore reserved

Category IV – Rs. 292.64 crore as against Rs. 1,200 crore reserved

Total Subscription – Rs. 1,034.24 crore as against total issue size of Rs. 3,000 crore

Not as great as the NTPC issue, but this issue has got reasonably subscribed on the first day.

Hi Shiv,

Again a silly and an apparent question, but just want to double check. I would be applying tomorrow so i assume I would get full allotment right ?

Yes Aditya, you’ll get full allotment.

Hi Shiv,

One query – IIFCL and HUDCO will pay the interest at coupon rates for successful allotments for the application->allotment period. Normally when would this interest get credited in our bank accounts ?

Hi Aditya,

Interest on application money is paid as the bonds get allotted, around that time itself.

Thanks for the info Shiv

You are welcome Aditya!

Hi

Why would a rate hike impact existing bonds? Wont yield increase for already listed ones. Please clarify.

Thanks

Hi Harineem,

As the interest rates go up, the yield as well as the price of already listed bonds go down, as the investors expect higher coupon rates from the forthcoming bonds.

I thought yield goes up because price goes down as you are getting interest at bonds less than par value. Makes a bit of sense what you are saying because if the same amount can be lent only at a higher rate from banks then the bond subscriber should also expect a higher rate of return.

Any link which can help in understanding this more.

Thanks a lot for answering all my basic queries with such patience every time.

You are welcome Harineem !!

Though there are many such links which can help you understand these relationships, here is one such link:

http://moneyover55.about.com/od/howtoinvest/qt/bondpricesrisinginterestrates.htm

I am planning to invest in this issue but going to get funds on 10th so I hope it’s not fully subscribed in 2 days like NTPC.

Hi Ikjot,

IIFCL issue will not get oversubscribed in 2 days.

That’s good, thanks Shiv for the reply.

You are welcome!

Is it possible to rank all the AAA PSUs issuing TF Bonds. And separately Same also for all AA PSUs?

It is not impossible to rank these issues based on the fundamentals of all their issuers, but it is not easy either. Some of these companies are listed on the stock exchanges, so disclosures are high. But, some are unlisted, so it is difficult to analyse those companies properly. If I get some time in the next couple of weeks, I’ll try to do that.

Hi Shiv,

“One more rate hike would once again ruin the mood of the market participants in the bond markets and result in a jump in the G-Sec yields” – Therefore should we wait a little longer and take a chance for getting higher coupon rates for IRFC, NHAI etc.

Good writeup and guidance as usual. Excellence of details is maintained in each of your articles. I am really grateful that i came across this site !!

Thanks a lot Aditya for your kind words !!

Nobody knows what Dr. Rajan is going to do on 18th December. It is totally up to you whether you want to wait for RBI’s monetary policy decision or you want to go ahead with these bonds. NTPC opportunity is behind us now.

RBI’s decision will hinge on inflation numbers next week. I have high hopes that the RBI is not going to hike the Repo Rate this time around and if it goes that ways, then you’ll see lower coupon rates with the forthcoming issues.

just came across this news a few days ago – http://www.google.com/url?sa=t&rct=j&q=&esrc=s&frm=1&source=newssearch&cd=2&cad=rja&ved=0CCwQqQIoADAB&url=http%3A%2F%2Fwww.thehindubusinessline.com%2Fcompanies%2Fiifcl-net-dives-59-in-first-half%2Farticle5383850.ece&ei=9ymkUqSKO8SxrAeJvoDwBA&usg=AFQjCNHjC4ghsFHsXzLWfJpnEgPOaesZXg

I am looking to invest in IIFCL bonds so how much of a factor should this be in deciding to invest in this issue ?

Hi Aditya,

It definitely matters, but then it is happening with every other public sector financier here in India. Personally, I’ll not give much importance to it in the short-term.

the ‘risk’ of interest rate hike has been so long(for debt investor ), but I believe 9%(approx) of rate is quite high in itself.

But a rate hike is surely in order, as real estate guys must face a crash, it is amazing they holding such prices even at these rates, can anyone enlighten what has been highest bond rates in recent past? 10% or more?

Tax-Free Bond coupon rates have never gone above these levels. 9.01% for a ‘AA+’ rated issue and 8.92% for a ‘AAA’ rated issue have been the highest rates so far.