This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

New India Assurance IPO Details

Should you invest in New India Assurance IPO or not @ Rs. 770-800?

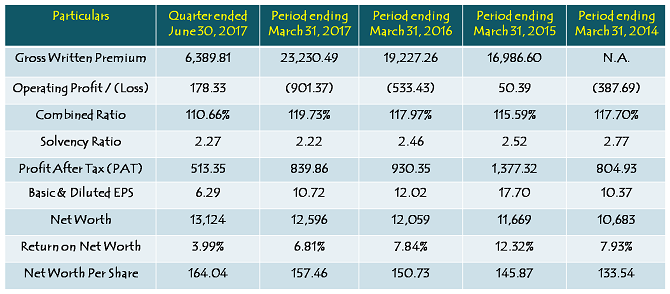

During the financial year 2016-17, New India Assurance reported Gross Written Premium of Rs. 23,230 crore, up 20.82% against previous year’s Rs. 19,227 crore. However, Gross Written Premium is the only area in which the company registered some kind of growth, as the company failed to perform on all other parameters. The company reported an operating loss of Rs. 901.37 crore as against Rs. 533.43 crore loss it had in FY 2015-16. Its profit after tax (PAT) was also down 9.72% at Rs. 839.86 crore as against Rs. 930.35 crore in 2015-16.

Combined Ratio stood at 119.73% (vs. 117.97% in FY 2015-16) and Solvency Ratio was at 2.22 times (vs. 2.46 times in FY 2015-16). Combined Ratio of 100 or above indicates that the company is incurring losses in its core insurance business. As far as Return on Net Worth (RoNW) is concerned, it has fallen from a high of 12.32% in FY 2014-15 to almost half at 6.81%.

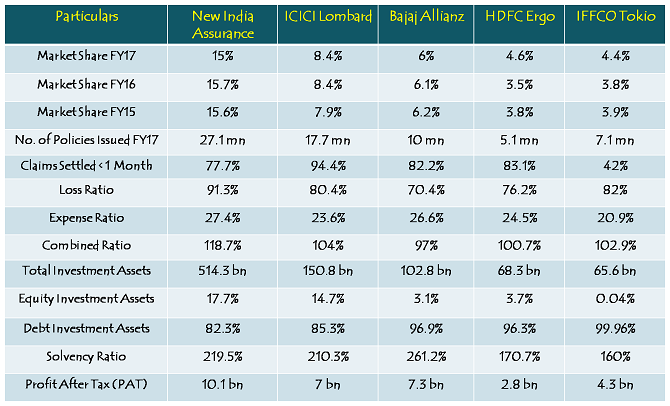

Recently listed ICICI Lombard is the only listed company with which we can compare NIA’s pricing and valuations, and NIA lags ICICI Lombard in almost all the parameters except Solvency Ratio. Firstly, NIA’s market share has declined from 15.6% in FY 2014-15 to 15% in FY 2016-17, whereas ICICI Lombard has been able to increase its pie from 7.9% in FY 2014-15 to 8.4% in FY 2016-17. HDFC Ergo and IFFCO Tokio too have gained on their respective market shares. Moreover, ICICI Lombard reported far better Combined Ratio (104%), Loss Ratio (80.4%) and Expense Ratio (23.6%) as compared to NIA for which these ratios stood at 118.7%, 91.3% and 27.4% respectively during the same period.

Peer Comparison

As far as its pricing is concerned, NIA is seeking a valuation of 74.63 times its trailing EPS of Rs. 10.72 and 4.88 times its book value of Rs. 164.04 as on June 30, 2017. The company showed a surprisingly remarkable turnaround in the first quarter of the current financial year and reported an EPS of Rs. 6.29 a share, based on which the PE ratio it is seeking has fallen to 31.8 times its annualised EPS of Rs. 25.16. However, looking at its declining or inconsistent performance in the past, I have a serious doubt over sustainability of this turnaround and that is why I don’t think the company deserves such high valuations. At these high valuations, I would personally avoid this IPO and invest my money with better managements and bankable businesses.

Nice Artice. It’s very informative. Thank You. 🙂

Thanks Ankit!

Mr. Kukreja, at current market prices after IPO listing, which of the INSURANCE companies would you advise a buy? Kindly specially advise regarding ICICI-PRU LIFE?

Hi S.K.,

I think I would go with SBI Life, but only at lower price points.

Great analysis as always Mr. Shiv.

Thanks Nitin! 🙂

Sir, what is your opinion on HDFC Life IPO & on KHADIM IPO please? Your inputs would be greatly appreciated.

me too waiting for u reply on HDFC Life IPO & on KHADIM IPO

Hi,

We are not covering Khadim IPO, but we’ll review HDFC Life IPO soon.

Thank you sir for your Analysis and recommendation

Thanks Venkat!

Your posts are indeed short and to the point. Its a pleasure reading.

Thanks!

Thank you Mr. Shiv for your valuable time and advise.

Thanks Vasu!