This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

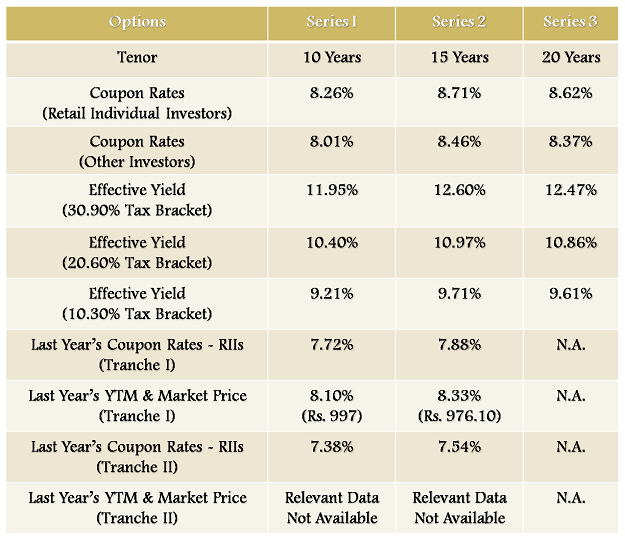

Rural Electrification Corporation (REC) will be launching the first public issue of tax-free bonds for the current financial year from 30th of this month. The company is offering quite attractive interest rates to the retail individual investors with 8.26% for 10 years, 8.71% for 15 years and 8.62% for 20 years. These rates are higher by approximately 0.70% to 1.50% as compared to the rates offered last year.

REC plans to raise Rs. 3,500 crore from this issue, including the green-shoe option of Rs. 2,500 crore. Though the official closing date of the issue is September 23rd, I think the issue should get closed before that due to oversubscription.

The government has allowed REC to issue Rs. 5,000 crore worth of tax-free bonds this financial year and the CBDT notification has mandated a minimum of 70% of this amount to be raised from public issues. As the issue size is Rs. 3,500 crore, if it gets fully subscribed this time itself, I think REC would raise rest of the money through private placements only and it will become the last issue of REC this financial year.

NRIs, QFIs & “Retail Individual Investor” – Non-Resident Indians (NRIs) on repatriable as well as non repatriable basis and Qualified Foreign Investors (QFIs) are also eligible to invest in this issue. The scope of a retail individual investor, investing upto and including Rs. 10 lakhs, has got broadened with the introduction of NRIs and QFIs (as individuals). It includes Hindu Undivided Families (HUFs) also through the Karta.

So, the investors have been classified into the following four categories:-

I – Qualified Institutional Bidders (QIBs) – 20% of the issue reserved

II – Non-Institutional Investors (NIIs) – 20% of the issue reserved

III – High Net Worth Individuals including HUFs, NRIs & QFIs – 20% of the issue reserved

IV – Retail Individual Investors including HUFs, NRIs & QFIs – 40% of the issue reserved

Interest Payment Date & Record Date – As this question gets asked by many of the investors throughout the year, it is better to mention it here itself as the date is known in advance this time. Interest will be paid on December 1st every year and the record date will be 15 days prior to that.

No Cumulative Option – There is no option of taking cumulative interest at the time of maturity with these bonds. Interest will be paid annually.

Safety, Ratings & Nature of Bonds – Being a ‘Navratna’ PSU, REC offers a high degree of safety as far as your investment is concerned and that gets reflected in the ratings assigned to this issue. The issue has been rated ‘AAA’ by four rating agencies, CRISIL, CARE, India Ratings and ICRA. It is the highest rating given by each of these companies. Also, these bonds are secured in nature against certain assets of the company.

Listing – REC bonds will get listed on the Bombay Stock Exchange (BSE) within 12 working days from the closing date of the issue. Investors have the option to apply these bonds as per their choice, either in physical form or in demat form.

TDS & Minimum Investment – As these are tax-free bonds, there is no question of TDS getting deducted, whether you take them in physical form or demat form. Minimum investment required is Rs. 5,000 only i.e. 5 bonds of Rs. 1,000 face value each.

Interest on Application Money & Refund – REC will pay interest to the successful allottees at the applicable coupon rate and at 5% per annum to the unsuccessful allottees.

Tax Treatment on Sale – Listed bonds held for more than 12 months qualify as long term capital assets and if sold thereafter, would attract a flat 10% capital gain tax, without indexation benefit. However, if the bonds are sold prior to holding them for more than 12 months, then short-term capital gain tax would be applicable, as per the tax slab of the investor.

Key Attractions of these Bonds: There were many issues with the tax-free bonds issued last year. There was a huge difference between the interest rate paid to the retail investors and the interest rate paid to other investors. Also, the subsequent buyer from the secondary markets was to get a lower rate of interest. Moreover, the cut from the G-Sec rate was also set on a higher side.

I think most of those issues have got rectified this year. Here are some of the key attractions of these bonds this year:

High Interest Rates – Due to the falling rupee and the unsuccessful measures taken by the Government and the RBI to control it from further fall, the yields of the benchmark government securities (G-Secs), against which the coupon rates of these tax-free bonds get fixed, have risen sharply in the last 45 days or so. 10-year benchmark yield touched a high of 9.47% before falling sharply to 8.25%. Thanks to this jump, the company has been able to offer such attractive coupon rates, especially for the 15 years period.

A word of caution. 10-year benchmark yield has again jumped back to close at 8.78% on August 27th. If the economic fundamentals of the country continue to deteriorate at the same speed as they have been doing, the yields could keep moving higher and the rupee could keep falling further against the dollar. But, I still hope India would come out of the current crisis soon and as the macroeconomic things get stabilised, these rates would look highly attractive again.

High Interest Rates, even if bought from the Secondary Markets – As per the CBDT notification – “The higher rate of interest, applicable to RIIs, shall not be available in case the bonds are transferred by RIIs to non retail investors”. So, the interest rates earned by the retail individual investors this year would remain higher even if they buy these bonds from the secondary markets subsequent to the offer period.

Your eligibility for a higher rate will depend on the number of bonds held in your name on the record date and the same will get tracked by your PAN number. Your holding should not be more than 1000 bonds per issue on the record date to get higher rate of interest.

Till last year, only the first allottees were eligible for a higher rate of interest and the subsequent buyers from the secondary markets were supposed to get a lower rate of interest. This factor will encourage the retail investors to participate in the secondary markets and thereby result in higher liquidity.

Low Differential – The differential between the rates offered to the retail individual investors and the other categories of investors has been cut down to 25 basis points (or 0.25%) only, as compared to last year’s 50 basis points (or 0.50%). This is the best step that has been taken this year. This factor would attract higher participation from the other categories of investors, both during the initial offer period as well as in the secondary markets.

I honestly think that these tax-free interest rates are very attractive. If I compare these rates with the interest rates on bank fixed deposits, the rates look quite similar, but with huge difference of tax applicability. I seriously hope India’s macroeconomic picture should start looking better in the days to come, only then we will be able to enjoy these high rates, otherwise inflation would again eat up all fruits of our hard work.

Link to Download the Application Forms of REC Tax-Free Bonds

If you need any further info or you want to invest in these bonds in Delhi/NCR, you can contact me at +919811797407

Day 3 subscription update:

Category I – Rs. 230.37 crore as against Rs. 700 crore reserved

Category II – Rs. 709.14 crore as against Rs. 700 crore reserved

Category III – Rs. 709.71 crore as against Rs. 700 crore reserved

Category IV – Rs. 1004.91 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2654.12 crore as against total issue size of Rs. 3500 crore

PFC is going for a private placement of its tax-free bonds on Friday. Rates are 8.11% for 10 years, 8.48% for 15 years and 8.44% for 20 years, which means PFC’s rates for its public issue would be 8.36% for 10 years, 8.73% for 15 years and 8.69% for 20 years.

Source: http://in.reuters.com/article/2013/09/03/pfc-bonds-idINL4N0GZ1GD20130903

What does private placement mean ? Why do they for private placement also ? Basically what is the diff between them ?

Thanks Shiv !

Private placements are done privately between the issuer and certain investors. They are not open to public at large. The issuers are not required to file prospectus and there are lesser other formalities and hence private placements are cheaper mode of raising money.

As per the news article, it seems that the PFC issue will be limited to provate placement (“The issue is open only to sovereign wealth funds and pension and gratuity fund investors, as per the document.”).

Does it mean that it will not come out with public issue? The rates for public issue mentioned by you for PFC are not mentioned in article, neither the article talk anything about public issue.

Can you please throw some more light?

Hi cvshah77… PFC has been given permission to issue Rs. 5,000 crore worth of tax-free bonds and out of that, at least Rs. 3,500 crore will be through public issues. PFC has opted to go with private placements first and that is PFC’s discretion. PFC will definitely come with its public issue. The rates mentioned above would be applicable for public issues only.

HUDCO has filed its Draft Shelf Prospectus for FY 2013-14 on August 29th, so the issue will most likely hit the markets in the next 15-20 days.

HUDCO is AA rated company. can we expect interest rate to be 9 %p.a ?

thanks

HUDCO issue is rated ‘AA+’ as per its draft shelf prospectus. Though it is quite optimistic to expect interest rate to cross 9% mark and the probability is very low, but still it can happen.

Dear sir,

Thanks for provinding useful info.

when is the next tax free bond issue coming.

Pradeep

Hi Pradeep… HUDCO, PFC and IIFCL are expected to hit the markets soon, in the next 10-20 days I think.

Why there is lack of interest by Category 1 investors (QIB)?

Hi Harshul… I think QIBs are foreseeing higher rate of interest in the issues to come and rightly so going by the yield movements.

It appears to be over subscribed already as of today.

Retail upto 10 lakhs investment limit is at 2.14 times.

No point in applying niw, if not done already. Isn’t it ?

Category No.of Bonds/NCDs offered/ reserved No. of Bonds/NCDs odered for No. of times subscribed

1 category1 2000000 2303200 1.15

2 category2 2000000 6846455 3.42

3 category3 2000000 6472106 3.24

4 category4 4000000 8564213 2.14

Total 10000000 24185974 2.42

Hi Vej,

The data above is showing oversubscription only against the base issue size of Rs. 1000 crore and not overall issue size. Total issue size is Rs. 3,500 crore and it got subscribed to the tune of Rs. 2654.12 crore till today evening. If you are a retail investor, you’ll still get full allotment as the reserved amount for the retail investors is Rs. 1400 crore.

Day 2 subscription figures:

Category I – Rs. 230.32 crore as against Rs. 700 crore reserved

Category II – Rs. 684.65 crore as against Rs. 700 crore reserved

Category III – Rs. 647.21 crore as against Rs. 700 crore reserved

Category IV – Rs. 856.42 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2418.60 crore as against Rs. 3500 crore reserved

Apart from the minimum lock-in of 10 years, these bonds make an attractive investment option. How easy is it to trade on these bonds?? Do they have an active secondary market? Can these bonds be pledged and a loan taken against them, if required?

Hi Annapurna,

I would not call it a lock-in period of 10 years, rather it is the minimum tenor of these bonds. Also, there is good enough liquidity in the secondary market for these bonds from an investors point of view. These bonds get traded on a daily basis in the secondary markets.

Yes, these bonds can also be pledged and a loan can be taken against them.

Dear Sir, Thanks for the wonderful detailed information about the tax free bonds…

Please advise me shall i sell REC Tax Free Bonds purchased last year in Dec’2012 as they carry only 7.38 % interest & should enter into the current REC bonds for 20 years at 8.62 % …?

( Even if the sell price for the same is a below par around 950 ….)

Hi Aryan… I think it is too late to do that now. The yields have already jumped higher and the prices have gone below their face value. Now, you should compare their YTMs with the coupon rates of current year’s bonds and then take a decision accordingly.

Hi Shiv,

REC tax free bonds offered this time contain the step down clause?

Hi Ashish… Step-Down feature has been removed from this year’s tax-free bonds. Category IV investors, with their bond holdings at 1000 bonds or less on the record date, will get higher rate of interest. Category I, II & III investors will get a lower rate of interest.

Thank you for detailed info on REC isue. As seen the issue is due to close on 23 Sept. Is there any chance of getting it closed earlier. Could you please let me know what is the status of retail subscription?

Thanks and Regards

Hi Anand,

Here are the subscription figures of Day 1:

Category I – Rs. 205.30 crore as against Rs. 700 crore reserved

Category II – Rs. 573.22 crore as against Rs. 700 crore reserved

Category III – Rs. 559.01 crore as against Rs. 700 crore reserved

Category IV – Rs. 487.52 crore as against Rs. 1400 crore reserved

Going by the response, the issue should get closed well before September 23rd.

Hi Vignesh,

Neither REC nor anybody else would give you a higher value for your bonds at the end of 15 years or at the time of maturity. You’ll get your principal investment back at that time.

Good article.

Question regarding this.

a) In case, the investor invest in these bonds (not for the full term) and need to trade it later (on BSE) for liquidity, is there a guarantee that there will be buyers for this on exchange, and if yes, will these always trade above the face value (given the market conditions, since I these are bonds I presume they will be?) – for capital protection.

b) Will the interest rate of these vary over the years as G-Sec int. rates vary?

Thanks Raghavendra!

a) Given the size of the issue and looking at the subscription figures, most likely there will be enough liquidity for the investors to cash out their investments. There is no guarantee that these bonds will always trade above their face value. Capital Protection does not mean that these bonds cannot go below their face value. But, as these are ‘AAA’ rated bonds, their is enough confidence that the company would pay back its interest and principal on time.

b) Interest rates will remain fixed throughout its tenure and will be paid on December 1st. YTM and market prices of these bonds will vary as per the market conditions.

Hi Sundar

Int remains constant throughout the tenure.

Coupon rate will be given always. But there will be change in capital invested that we need to declare as capital gain while cashing out.

And shiv one more query :

How much capital appreciation one could expect in this;at the end of 15 yrs ?

Pls shiv correct me if am wrong

After reading the last comment, I have another question. Where can I see the current value of 2012 REC bonds or any other bonds from the pervious years. Also, can you let me know how much interest one can get from these bonds?

For example, one has invested in a bond for Rs10 lakhs with the interest rate of 8%. If the bond price goes below Rs10/unit and assume the total value of investment is say Rs 9 lakhs in next year. What is the interest amount that one will get, Rs80,000 or Rs 72000? Does one get Rs80k every year irrespective of the bond price or will it change based on current value of the bond? Can you let me know? Thanks,

Sundar.

Hi Sundararajan… Vignesh is right in stating that the interest amount will remain constant at Rs. 80,000 every year and it has nothing to do with the market price of these bonds. Even your principal investment value will remain constant at Rs. 10 lakhs at the time of maturity, if you hold these bonds for their full term. Whatever movement happens in the market price of these bonds will happen only in between the date of listing and the date of maturity.

Here is the link to check the bonds/NCDs of previous years which are listed on the NSE:

http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

Shiv = Quite likely, the market price of bonds issued in 2011-12 and more so for those issued in 2012-13 will fall sharply. Are you tracking their market rate. Any comments

Hi… Yes, the prices have already fallen quite sharply, in fact, by approximately 6-10% in the last 1-2 months itself. NHAI N2 bonds, which were trading at around Rs. 1160 a month back, are now trading at around Rs. 1079. Bonds issued last year are all trading at below the face value of Rs. 1000 and the approximate yield range has jumped to 8.30-8.50%.

Thank you for the detailed answer and explanation. That will really help.

Sundar.

You are welcome!

I have a question. Under HNI section of the instructions, it is mentioned like this

The following Investors applying for an amount aggregating to above `10 lakhs across all

Series of Bonds in this Tranche – I Issue:

What does this exactly mean?

My question is, how HNI is determined? I understand that one can invest upto Rs 10 lakhs and that falls under retail category. But if one person invests in more than one tax free bonds (from different companies) each Rs10 lakhs and still considered as retail investor? Or total of all tax free bonds should be Rs 10 lakhs to be considered as retail investor? Since PAN number is given when one apply for these bonds.

BTW, is this limit per year? Can you let me know?

Also, I read online about IIFCL tax free bonds 2013 (to be open in Aug 2013), but couldn’t find more information like when it will open, interest rates etc? Do you have information about that? Please let me know. Thanks,

BTW, your website gives lots of good information with no strings attached so far. Thank you for doing this.

Thanks Sundararajan for your kind words !!

Investors investing Rs. 10 lakhs per issue per company would be classified as Retail Investors. They can invest Rs. 10 lakhs in every issue of REC (and/or any other company) and still enjoy higher rate of interest. So, if REC & IIFCL come out with their 2 issues each this financial year, a retail investor can invest Rs. 10 lakhs * 2 * 2 = 40 lakhs.

As per my information, IIFCL would be launching its tax free bonds issue in September. Interest rates are linked to G-Sec yields, so will be announced by the company at some later date only.

Hi Shiv, Thanks for the post. We know that there are many other companies too lined up this year which might come up with the issue. Do you think to wait for the rest of them or put all eggs into this one ? Please provide your thoughts.

Hi Karthik, I think it is always wise to diversify your portfolio, even if the returns are very attractive. As the coupon rates of these tax-free bonds are linked to the reference G-Sec rates, most of the companies which will issue these bonds even in September or October, the coupon rates would be similar i.e. plus/minus 0.25%. The chances of a sharp downturn in rates look very remote at present.

REC’s 15-year option looks attractive to me, dont know if others too will be able to offer similar rate. I hope they should be.

Hi Shiv,

How can a person buy bonds from retail market? Do the equity brokers allow that? I am not able to see them on my trading platform?

Paul.

Hi Paul… yes, these bonds get listed on the stock exchanges and equity brokers do facilitate trading in these bonds. I am not sure why you are not able to find them on your trading platform. Which platform you use?

Plz check this link, it has trading info of bonds listed on the NSE: http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

I was looking at the Series EQ. Saw the bonds now! Thank you for your help.

Thats great, thanks!