This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

National Housing Bank (NHB), a wholly-owned subsidiary of the Reserve Bank of India (RBI) and the regulator of the housing finance companies (HFCs) in India, will be coming out with its issue of tax free bonds from the coming Monday, 30th of December.

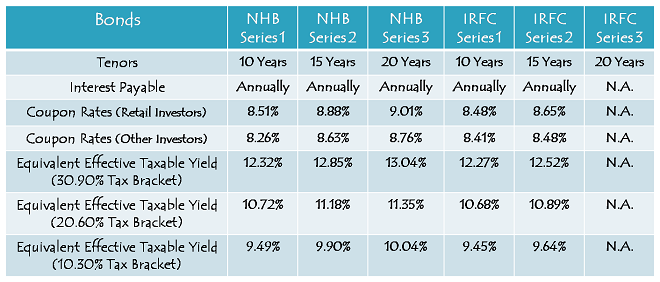

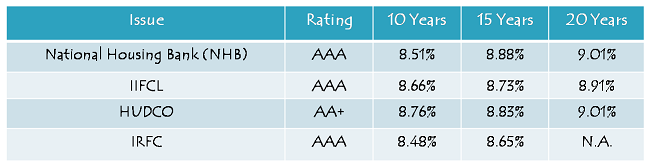

The good news is that the company is going to offer 9.01% per annum for the 20-year option and 8.88% per annum for the 15-year option, which is the highest rate of interest any ‘AAA’ rated issue has carried till date.

Though the issue is scheduled to remain open for the whole of next month to close on January 31st, 2014, the company reserves the right to close it earlier as well in case the issue gets oversubscribed anytime before the due date.

Size of the Issue – NHB is authorised to issue tax free bonds worth Rs. 3,000 crore this financial year, out of which it has already raised Rs. 900 crore through a private placement carried out on August 30th, 2013. NHB plans to raise the remaining Rs. 2,100 crore from this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.

Rating of the Issue – Being the regulator of the housing finance companies and a wholly-owned subsidiary of the RBI, this issue of NHB has been rated as ‘AAA’ by three credit rating agencies, CRISIL, CARE and ICRA, which is the highest rating by these rating agencies.

Interest Rates on Offer – The company has decided to offer 9.01% p.a. with the 20-year bonds, 8.88% p.a. with the 15-year bonds and 8.51% p.a. with the 10-year bonds. HUDCO is currently offering 9.01% p.a. for 20 years, 8.83% p.a. for 15 years and 8.76% p.a. for 10 years, but that is a ‘AA+’ rated issue. At 9.01% and 8.88%, NHB issue has become the best AAA rated issue for the 20-year and 15-year duration respectively.

If you want to have only AAA rated bonds in your portfolio and do not have more than 10 year investment horizon, then you can still subscribe to the IIFCL bonds which carry 8.66% p.a. interest rate for 10 years.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 210 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 525 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 525 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 840 crore is reserved

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Lock-in Period, Premature Redemption & Listing – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they have been listed for trading.

The company has decided to get these bonds listed only on the National Stock Exchange (NSE) and has got the necessary in-principle listing approval for the same on December 20, 2013. The company will get these bonds allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will still get credited to your respective bank accounts through ECS.

Interest on Application Money & Refund – NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – NHB is the first company this financial year to keep the face value of its bonds as Rs. 5,000 instead of Rs. 1,000. Considering its face value and minimum application size of one bond, an investor is required to invest at least Rs. 5,000 in this issue.

Interest Payment Date – NHB has not fixed its interest payment date as yet and the first due interest will be paid exactly one year after the deemed date of allotment. As the deemed date of allotment will be fixed once the issue gets closed and before the bonds get listed, I will update this post as and when it gets announced.

Should you invest in this issue?

I would say that one should definitely invest in this issue and I have many reasons to justify my view. Here are some of those reasons:

First, NHB issue is ‘AAA’ rated.

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Application Form of NHB Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

I haven’t received the physical certificate for NHB bonds yet. Only received the allotment letter. Anyone else still waiting for the certificate? I plan to convert it to demat form.

Thanks

NHB, NTPC, IIFCL seek govt nod for extra tax-free bonds, AAI unlikely to offer TFBs

http://freepressjournal.in/nhb-ntpc-iifcl-seek-govt-nod-for-extra-tax-free-bonds/

Thanks shiv you are very helpful. These bonds are trading at very high premium. I wanted to buy it from market but i didn’t know about such a high premium.

You are welcome Vikram!

Yes, these bonds carry good premium as demand for 9%+ tax-free interest bonds is quite high.

Hello shiv, Is this bonds are listed? If yes then please provide me details. Thanks a lot in advance.

Hi Vikram,

Yes, these bonds are listed. Here is the link to its details:

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NHBTF2014&series=N6

Dear Mr Shiv ,

Most of all the boarders would find very interesting topic for today market ..

can you help us all with this Topic ?

Which is best listed tax free bond?

you earlier posted on JULY 16, 2012…

Hi Rohit,

I think Manshu did a post on the same and it doesn’t make any sense to me to do a post on the same now. I think its too late to cover it as most of the issues are already over. I made a couple of comparisons – (i) between NHPC and PFC and (ii) between IRFC and NHAI, but at present only IRFC issue is open, so there is nothing to compare it with.

sorry Mr shiv , i was requesting about listed bonds (secondary market) as we dont have many options left in Primary market.

i urgently want to buy but dont know which to buy as some are

with 2-4 % premium on issue price. Need to know which can give best YTM at present market …thanks a ton .

This is the way I calculate the YTM of listed bonds, please let me know if I am right – as an illustration, let me cite the latest NHB 9.01% tax-free bonds (NHBTF2014 N6):

CMP: 5167

Interest for 15 days (Jan 13-28) embedded in the bond: 18.51

CMP net of embedded interest: 5148.49 (this is the actual amount we are going to pay for this bond)

Therefore, YTM: 450.5 (annual interest per bond)/ 5148.49 = 8.75%

However, I have not considered brokerage cost here. Brokerage will further reduce the yield.

This is not the way the yield gets calculated Santonu. Please check this link – http://www.onemint.com/2012/07/25/how-to-calculate-yield-to-maturity-of-a-bond-or-ncd/

Hi Rohit,

It is not easy to do such a comparison and conclude which one is the best among all the listed bonds. One which is trading at a higher yield today might become pricier after a month or so. Then it would not remain the best of all. Do your own research or consult a financial advisor to help you in buying some high yielding bonds.

Hi Shiv

NHBTF 2014. N 6 – retail Investor (category. I.) coupon rate. 9.01 %. and N. 3. – Category. II ( Trust ). Coupon rate. 8.76 %

If I purchase from open market ( NSE ). N 6 ( Retail category ) and this will go in to my Trust Demat a/c which fall in to category II , then what coupon rate I will get ? ( 9.01 %. OR. 8.76 % )

Hi Paresh,

You’ll get 8.76% p.a. interest.

IREDA has filed the Draft Shelf Prospectus with SEBI for its tax free bond issue on January 21st. The issue will be ‘AAA’ rated and NRIs are not eligible to invest in this as well.

Hello Shiv

Is it possible for NRIs to buy NHB bonds from Secondary market since they were not allowed to participate in IPO.

Thanx

Hi Rakesh,

Though I don’t think NRIs are allowed to buy NHB bonds from the secondary markets, but I am not 100% sure about it. You’ll have to check it with the company about it.

Hi Shiv,

I am a retail investor and am planning to buy NHB Tranche – I Series 3B (9.01%, 20 yrs) bonds in the secondary market. Am I eligible to get 9.01 % interest on these bonds or lesser, since I was not a direct allottee ?

A silly question, Also will the interest from these bonds continue to be tax free in my hands ?

Thanks in advance

LittleG

Hi LittleG,

If you buy tax-free bonds issued this financial year, including NHB bonds, you’ll be eligible for the same rate of interest as it is there for the first allottees. In this case, you’ll get 9.01% rate of interest. This rate of interest will be valid till your investment amount doesn’t cross Rs. 10 lakh mark. Also, it will remain tax-free for you as well.

hi shiv

exactly got 75 percent allocation. money refunded along with interest. but whether interest given for refund taxable ?

any other tax free bonds open as of now ?

Hi Vignesh,

Yes, the interest earned on the application money as well as on the refund money is taxable.

Also, two issues are open as of now, NHAI 8.75% (15Y) & 8.52% (10Y) and IRFC 8.65% (15Y) & 8.48% (10Y).

http://www.onemint.com/2014/01/12/nhai-tax-free-bonds-january-2014/

http://www.onemint.com/2013/12/28/irfc-tax-free-bonds-8-65-january-2014-issue/

http://www.onemint.com/2014/01/15/nhais-8-75-or-8-52-vs-irfcs-8-65-or-8-48-which-issue-is-better/

NHB bonds got listed today on the NSE. 9.01% 20-year bonds opened at Rs. 5,055.10, which was also the lowest price these bonds traded at, touched a high of Rs. 5,105 and finally closed at Rs. 5,100.88.

Total 1,33,444 bonds got traded on the stock exchange, worth Rs. 68.01 crore. People, who say there is a lack of liquidity with these bonds, should notice these volumes. These volumes are good enough to exit, partially liquidate or increase your investments.

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NHBTF2014&series=N6

Thanks for the link Jasbir!

Mr Shiv,

i have received in my DP but not received the refund amount

what should i do .. i want to buy 25 % from market even at higher rates..

what do you suggest sir.

Hi Rohit,

You should contact the Registrar, Karvy Computershare, for the refund amount.

thanks shiv for your suggestion.

Earlier you gave a useful Edeweiss url to check rates / compare various Bond price in market .. can you pl. paste that link as i lost it ..

Here you’ve the link:

https://www.edelweiss.in/debt/National-Housing-Bank/NHBTF2023-N1.html

NHB tax-free bonds to get listed on the NSE on January 16th i.e. Thursday.

Here are the NSE codes for the same:

8.51% 10-year bonds – NSE Code – N4

8.88% 15-year bonds – NSE Code – N5

9.01% 20-year bonds – NSE Code – N6

Deemed date of allotment has been fixed as January 13, 2014. Interest will be paid on January 13th every year.

NHB Bonds are listing tomorrow (16/01/2014) in the NSE.

http://www.nseindia.com/circulars/circular.htm

Thanks for sharing it first here Sanjay!

Think our investment in NHB tax free bonds has been near perfect.

WPI inflation in December 2013 has come down more sharply than expected to 6.16% against 7.52% in November 2013. Also, the 10-year G-Sec yield has fallen to 8.62% from 8.71% as of yesterday and from around 9% few weeks back.

This suggest that issues in near future may not be able to give high rate of interest and also listed bonds having high interest rate would have better valuation in the secondary market.

I fully agree with your views!

Anyone who used ICICI Direct got refund yet?

Got it about an hour back.

Got 75% allotment for NHB. Hudco bonds also got credited to dmat a/c today though the issue closed 2 days after NHB closing. Any idea when these two will get listed?

NHB bonds should get listed on Thursday and HUDCO bonds a day or two after that. No announcements yet by these companies though.

Got hudco 100% and nhb 70%. Thanks Shiv I wouldn’t even have known of these if I wasn’t following the blog. Any ideas on how to invest the interests. Thanks

You are most welcome Harinee! You should invest the interest income as per your asset allocation.

I received messages from HUDCO and IRFCL regarding debit of application

of money from my Savings Bank account. HUDCO bonds have been credited to my Demat account but not IRFCL. When can I expect these to be credited to my Demat account?

Hi Mr. Rakesh,

You can expect the bonds to get credited to your demat account at least 7-8 working days after the issue gets closed. IRFC issue is scheduled to get closed on January 20th, if not extended beyond this date.