This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

National Housing Bank (NHB), a wholly-owned subsidiary of the Reserve Bank of India (RBI) and the regulator of the housing finance companies (HFCs) in India, will be coming out with its issue of tax free bonds from the coming Monday, 30th of December.

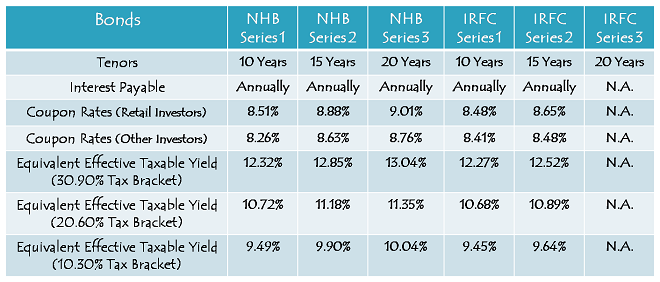

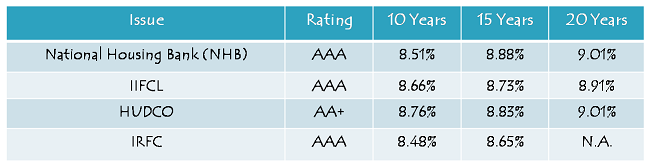

The good news is that the company is going to offer 9.01% per annum for the 20-year option and 8.88% per annum for the 15-year option, which is the highest rate of interest any ‘AAA’ rated issue has carried till date.

Though the issue is scheduled to remain open for the whole of next month to close on January 31st, 2014, the company reserves the right to close it earlier as well in case the issue gets oversubscribed anytime before the due date.

Size of the Issue – NHB is authorised to issue tax free bonds worth Rs. 3,000 crore this financial year, out of which it has already raised Rs. 900 crore through a private placement carried out on August 30th, 2013. NHB plans to raise the remaining Rs. 2,100 crore from this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.

Rating of the Issue – Being the regulator of the housing finance companies and a wholly-owned subsidiary of the RBI, this issue of NHB has been rated as ‘AAA’ by three credit rating agencies, CRISIL, CARE and ICRA, which is the highest rating by these rating agencies.

Interest Rates on Offer – The company has decided to offer 9.01% p.a. with the 20-year bonds, 8.88% p.a. with the 15-year bonds and 8.51% p.a. with the 10-year bonds. HUDCO is currently offering 9.01% p.a. for 20 years, 8.83% p.a. for 15 years and 8.76% p.a. for 10 years, but that is a ‘AA+’ rated issue. At 9.01% and 8.88%, NHB issue has become the best AAA rated issue for the 20-year and 15-year duration respectively.

If you want to have only AAA rated bonds in your portfolio and do not have more than 10 year investment horizon, then you can still subscribe to the IIFCL bonds which carry 8.66% p.a. interest rate for 10 years.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 210 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 525 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 525 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 840 crore is reserved

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Lock-in Period, Premature Redemption & Listing – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they have been listed for trading.

The company has decided to get these bonds listed only on the National Stock Exchange (NSE) and has got the necessary in-principle listing approval for the same on December 20, 2013. The company will get these bonds allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will still get credited to your respective bank accounts through ECS.

Interest on Application Money & Refund – NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – NHB is the first company this financial year to keep the face value of its bonds as Rs. 5,000 instead of Rs. 1,000. Considering its face value and minimum application size of one bond, an investor is required to invest at least Rs. 5,000 in this issue.

Interest Payment Date – NHB has not fixed its interest payment date as yet and the first due interest will be paid exactly one year after the deemed date of allotment. As the deemed date of allotment will be fixed once the issue gets closed and before the bonds get listed, I will update this post as and when it gets announced.

Should you invest in this issue?

I would say that one should definitely invest in this issue and I have many reasons to justify my view. Here are some of those reasons:

First, NHB issue is ‘AAA’ rated.

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Application Form of NHB Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

Hi Shiv,

I have applied for NHB Bonds on day 1 itself by way of three different physical applications (2L, 1L & 1L) in the same name at different times. The bidding and banking has been done on the first day itself for all three applications. However, I didn’t receive any allotment for both 1L applications. Do you know the possible reason for non allotment in last 2 applications? As far as I understand that anyone applying the bonds on 1st day will day will get the 75% allotment even if the person is applying multiple applications. Any help out here will be highly appreciated.

Thanks

Sanjay

I have made 2 applications and both online in the morning itself. Allocation happened for both the applications. So multiple applications can not be a reason and mostly to do with the uploading. If you submitted after 3 PM, sometime upload happens next day.

Hi Sanjay,

I think incorrect bidding or mismatch between bidding details and your application details should be the reason behind the rejection. You should check the exact reason either with your broker or the Registrar, Karvy Computershare.

As mentioned in Point 4 in the post above, CPI inflation in December 2013 has moderated to 9.87% on the expected lines, as against 11.24% for November 2013. Also, as the 10-year G-Sec yield has fallen to 8.71% today, I think both these are reasonably good news for the bond/debt markets.

Hi Ikjot, I used ICICI direct account and I didn’t get refund yet.

Same here still nothing. I believe will be there by tomorrow.

Hi all, I too used the icicidirect account for this transaction. I see both a demat entry (75% of applied for bonds have been allocated) and the refund of my money (along with interest) in my bank account as of 10:30 PM today.

Thanks for sharing this info Rama!

Got 74% demat allocation of applied bonds of NHB but still no refund from ICICI DIRECT.

Anyone who has account with ICICI DIRECT got his refund yet?

No. ICICI Direct is yet to give refund or demat credit. Generally bonds get credited by midnight and refund comes a day delayed compared to others. We should get refund tomorrow , hopefully

Regards

Ramadas

SBI Cap also, I got refund in one account at 5PM. Other one is still not happened. The Bonds credited message came in both the demat accounts. I also want to update that HUDCO allocation message also came which is 100%

Thanks Ramdas for your reply. Hope we get it in time to invest in NHAI.

I think the investors should check their bank accounts to get refund info, if they are not registered with their banks for SMS Alerts. There will be cases in which the investors might not have received the refund and the interest on their investment amount as yet.

I think the refund process should get completed by the end of the day today. Allotment process has also started and should get completed by the end of the day tomorrow.

Yes, I have an account with ICICI DIRECT. I have received the refund today morning. Looks like it is 25% refund + some interest.

That’s good to know. Thanks for reply Sailesh.

I also got my refund at 3 PM today. Allotment of 75%

Thanks for sharing this Mr. Vinod!

I got my refund too.. around 3 pm. 75% allotment. Hoping that the bonds get credited soon to the demat account. This will be the first TFB holding that i have ever had 🙂

I have just received my NHB refund, I too have got 75% allotment.

Here I wish a very Happy Lohri to all the readers of OneMint !!

Many thanks, Shiv, for the Lohri wishes. I would like to add my best wishes for a great Lohri/Sankranti to all readers as well.

Dear shiv.

when should be get recent HUDCO , IIFCL & NHB Allotment

& Approx Listing Dates of the above 3 issue…

Dear Rohit,

NHB and HUDCO are expected to get listed sometime this week itself, whereas IIFCL bonds should get listed sometime around January 24th-25th.

thank you Mr Shiv for the info .. and it should show in our DP a/c after how many days of listing ?

Bonds get credited to every investor’s demat account before they start trading on the exchange(s). So, NHB bonds should get credited into your demat account today or tomorrow and then only its trading will start.

Sorry, it was my calculation mistake. The alloment is 75% of applied bonds (not 67%). When are IIFCL Bonds expected?

IIFCL issue has closed on Friday only. It should get listed on or around January 24th.

Percentage of deduction of funds may not be used to arrive at percentage of allotment (which can be uniform). Eg at 74% allotment, A applied for 12 bonds can get 8 to 9 bonds which would require 66% to 75% deduction of funds.

Yes, that’s right.

I’ve applied for 150 bonds so based on this Will I get near about 100-110 bonds?

Yes, around 110 bonds.

Thanks for the reply.

You are welcome!

Today (11-1-2014) allocation money has been debited to my account. Money has been debited for roughly 67% of applied bonds. May be

percentage will vary from person to person depending on date & time

of application (my guess). Possibly will get bonds credited to my Demat

account on Monday/Tuesday.

‘Date’ & ‘Time’ of the applications will not be relevant at all. Only those investors who applied for it on the first day itself will get the allotment. Time of the applications is also not relevant as it will be done on a pro-rata basis. Its just that the investors who have applied for only 1 bond, 2 bonds or 3 bonds should get full allotment. It will get clear only once the Basis of Allotment gets announced.

Received the debit email (ASBA so funds have now been debited) from my bank today. 75% Allotment. Allotment email not received though (that is stating bonds have been credited into account).

Oh that’s great, thanks for sharing this info !! So, I hope the allotment process should get completed by Monday-Tuesday and the bonds to get listed by Wednesday.

I just checked the Bank Account… I am getting 70% allotment.

Thanks Amlan for sharing this info! So, it looks like that it is varying from investment amount to investment amount, falling between 70% to 100% allotment.

Shiv – could you please clarify on “varying from investment amount to investment amount” ? i was under the impression that everyone gets the allotment in the same ratio

I think the investors who have applied for only 1 bond, 2 bonds or 3 bonds should get full allotment. Also, as different investors are sharing different number of bonds allotted to them, I think it will not be 70% allotment to all.

NHAI Tax-Free Bonds issue opens January 15th. Coupon Rates – 8.52% for 10 years and 8.75% for 15 years. 20-year option is not there. It is rated ‘AAA’ and closes on February 5, 2014.

Thanks for this news Shiv. What is the issue size ?

It is Rs. 3,698.40 crore issue.

So approximately 1400 crores for retails right ?

Rs. 1479.36 crore for the retail investors to be precise.

So do you think it is going to be fully subscribed on Day 1 in the retail category ? I am waiting for NHB refunds and hope it comes before 15th Jan.

I doubt it will get oversubscribed on the first day itself in the retail category. NHB refunds should start pouring in from Monday or Tuesday I think.

Shiv – Will we also get the interest on the alloted and refunded amount along with the refund money ?

Yes, we’ll get interest on both the amounts.

Anyone got the allotment\refund for the NHB issue ?

I have not till yet.

Hi Shiv,

I have been reading your blog since inception and love the analysis you and Manshu bring to the table. Keep up the good work and ignore people like Sam.

Do keep us posted with the date of listing.

Sure AB, I’ll do that, thanks for your kind words !!

Dear Shiv,

Is there any way to cross-check whether the broker with whom I have submitted my application has done bidding on NSE/BSE platform or not ?

On the exchanges, is it possible for retail investor to buy bonds issued to non-retail category and still get higher coupan applicable to retail category for a particular tenure ? e.g. for NHPC and NTPC there are total of six series (N1 to N3 for non-retail and N4 to N6 for retail). Can a retail investor buy bonds from series N1 to N3 based on the tenure he wants and still get higher coupan payable to retail ?

If the answer to above question is “yes”, why is there separate series for retail and non-retail, as both can buy bonds from either series and get coupans applicable to their category ?

Thanks

Dear TCB,

As your broker bids for your application, an exchange Bid ID gets generated which is known to the broker. It is not possible to successfully submit the application in a designated bank branch without BSE/NSE Bid ID. I am not sure whether there is any mechanism to check it online on the exchange’s website, but you can ask your broker the Bid ID of your application. I usually convey the Bid IDs to my clients when I do bidding of their application forms.

Though I am not 100% sure, but I think it is possible for the retail investor to buy bonds issued to the non-retail investors and still get higher coupon applicable to the retail category. Coupon rate applicable to a retail investor would depend on the number of bonds held by the investor on the record date. If a retail investor subscribes to these bonds for Rs. 10 lakhs and buys some additional bonds from the market, then he/she would be categorized as a non-retail investor.

I think separate categories are there as every listed security needs to carry a different ISIN number and different exchange code.

Hi TCB / Shiv,

The rule is like this.

1. These (retail / others) are separate series.

2. Anyone buying into the retail series will get higher coupon rate if the “face value” of their holding at the time of interest payment is below Rs 10 lakh. If the value is above Rs 10 lakh, they will only get lower coupon rates.

3. The “other series” will remain as it is – ie you will get only lower rate even if your holding is only Rs 1 lakh.

Regards,

Thanks a lot Raju for sharing this info !! Is this info there in the Prospectus? If yes, can you please share the extract?

The given below link give details about it:

http://www.nhb.org.in/Whats_new/NHB-Prospectus-Tranche-I.pdf

The issue closed on Jan 1. Any news about its allotment?

No info as yet on NHB allotment. I think it is too early to expect NHB’s allotment as it has been only 5 working days since the issue got closed. I am expecting the refund/allotment to happen either on Friday or Monday.

What is minimum no. of bonds that will be alloted ? is it 5 ?

As the face value of each bond is Rs. 5,000, I think at least one bond should get allotted.

Thanks for the quick reply. I was planning to recycle the refund money to IIFCL bonds before it gets closed on Jan 10. That is why I asked.

I hope you get your refund back on time and are able to channelize it into IIFCL bonds issue.

Hi shiv,

If we get bonds in physical form, then the annual payout arrives in a form of check by post and manually to be deposited into our bank?

Or it is still automatically credited in our bank account annually ?

Just trying to compare whether It is worth to have a demat account and pay maintenance fees,just for holding tax free bonds , which I don’t plan to sell , but just get the interest payout annually without much hassle

Hi Prash,

In case you take these bonds in physical form also, interest will get credited directly to your bank account.

Thanks Shiv. One more question, how can I apply for physical form, can you guide me for the process and steps needed ?. Couldn’t find much valuable info doing random google search on same.

Hi Prash,

We, at Ojas Capital as a brokerage firm, help investors do it on a PAN India level. Here is the procedure to apply it in the physical form:

* Download the application form and duly fill it.

* Mail us the scanned copy of your duly filled form and we’ll do the bidding on the stock exchange, which is mandatory before banking the application form.

* We’ll let you know the BSE/NSE Bid ID, which you’ll be required to mention in front of the application form numbers.

* After that you can either courier the form to us, along with your self-attested copies of PAN card, address proof and a cancelled cheque, or directly submit the form/docs at the designated bank branch nearest to your place. We’ll let you know the address of the designated bank branch nearest to your place. If required by you & possible for us, we’ll get the form, docs picked from your place.

I hope it helps! For any clarification or further info, you can contact me at +91-9811797407 or mail me at skukreja@investitude.co.in

You can get in touch with any of your local brokers also for the same.

What are the expected allocation dates for HUDCO and NHB TFBs which

closed recently?

I think NHB bonds should get listed by January 14-15 and HUDCO bonds should list by January 16-17.

Dear Shiv,

Long-time reader/first time commenter. I would like to wish you and your near and dear ones a happy and joyous new year ahead.

Please keep up the good work!

Anirban

Thanks a lot Anirban for your wishes !! You too have a wonderful 2014 ahead !! 🙂