This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

India Infoline Housing Finance Limited (IIHFL), which came out with its first public issue of secured non-convertible debentures (NCDs) in December, has decided to launch another such issue from tomorrow, 12th of March. The company offered 11.52% per annum as the interest rate to raise Rs. 500 crore in December and wants to raise another Rs. 200 crore from this issue with a higher rate of interest of 12% per annum.

The issue is scheduled to close on March 24, but going by the size of the issue, the response it got for its last issue and a fairly attractive interest rate of 12% p.a. payable monthly, I think it should get oversubscribed in a very short period of time, probably in a day or two. One thing which has left me disappointed is that these NCDs are unsecured in nature, whereas NCDs issued last time were secured.

Before we check how the issue looks from an investment point of view, let’s take a look at some of its key features:

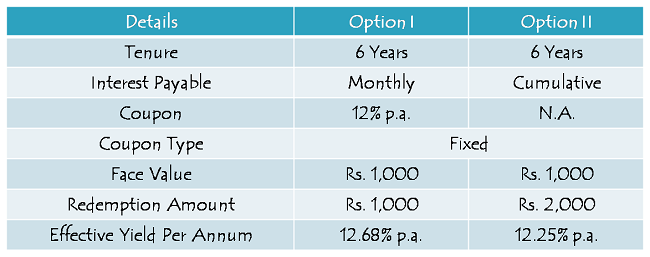

Interest Rate on Offer & Effective Yield – Like last time, the structure of this current issue is fairly simple. The company has decided to offer 12% p.a. payable monthly for a tenure of six years, as compared to 11.52% p.a. it offered last time for five years.

This issue also offers to double your investment amount in the same time period, if the investor decides to go for the cumulative option. With the cumulative option, the effective yield works out to be approximately 12.25% p.a., whereas the same stands at approximately 12.68% p.a. with the monthly interest option.

Credit Rating & Size of the Issue – CRISIL and ICRA have been appointed as the credit rating agencies for this issue and both have rated the issue as ‘AA-’ with a ‘Stable’ outlook. IIHFL wants to raise Rs. 200 crore from this issue, including the green shoe option of Rs. 100 crore.

Foreign Portfolio Investment – Non-Resident investors, including NRIs, QFIs and FIIs, are not eligible to invest in these NCDs.

Categories of Investors – The company has decided to categorise investors in the following three categories:

Category I – Qualified Institutional Bidders (QIBs) – 30% of the issue is reserved

Category II – Non-Retail Investors including HNIs, HUFs, Corporates etc. – 10% of the issue is reserved

Category III – Retail Investors, including HUFs, investing Rs. 10 lakh or below – 60% of the issue is reserved

Allotment on First Come First Serve Basis – Allotment will be made on a first come first served (FCFS) basis.

Minimum Investment – An investor needs to invest a minimum of Rs. 10,000 in this issue i.e. 10 NCDs worth Rs. 1,000 each.

Listing – The company has decided to list its NCDs on the National Stock Exchange (NSE) as well as on the Bombay Stock Exchange (BSE) and as always, the company will ensure that these NCDs get listed on the exchanges within 12 working days from the closing date of the issue.

Liquidity & Demat A/c. – As these NCDs will get listed on the stock exchanges, its investors will have the option to sell them whenever they want or have any urgent cash requirement. But, it is not mandatory to have a demat account to invest in this issue. You can subscribe for these NCDs in physical form as well, like you invest in bank/corporate fixed deposits (FDs) or post office schemes.

Interest Payment Date – IIHFL has decided to pay interest on the investors’ money on a monthly basis, but has not fixed the date of interest payment as yet. Interest payment will start from one month after the deemed date of allotment and will keep on getting paid on the same date every month.

Past Performance of India Infoline Housing Finance Limited (IIHFL) NCDs

I had reviewed IIHFL’s profile and financials when I covered its last issue in December. As the company has not updated its latest financial results in the prospectus filed for this issue, I have not been able to review its December quarter results. If you want to check its results up to September 2013, you can check the December post.

So, as there is nothing new on the financials front, let us focus on the performance of its NCDs issued last time around. Price of its already listed NCDs hit a 52-week high of Rs. 996.70 and a 52-week low of Rs. 899.90. It closed at Rs. 968.84 on the NSE today, which I would say is a steep discount to its face value of Rs. 1,000.

The company pays the due interest for its already listed NCDs on 27th of every month and the record date for the same falls due on 17th of that month, which means these NCDs go “ex-interest” two trading days prior to that. So, its current price of Rs. 968.84 already carries some portion of its current month’s interest also.

Though I think 12% annual rate of interest is fairly attractive, the nature of its current NCDs to be unsecured and the performance of its NCDs issued last time make me feel that it is better to avoid this issue at present and wait to buy these NCDs later from the stock exchanges when they get listed.

A long term investor, who is not liable to pay any taxes, wants regular income on a monthly basis and carries a little risk appetite, can subscribe to this issue as I think this issue looks relatively attractive to me as compared to its last issue.

Application Form of IIHFL NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IIHFL NCDs, you can contact me at +919811797407

I holding 1000 NCD , how can I cash my NCD ?

I want to take Home Loan. How can visit you.

M: 9555551234

2108, Sector-4A, Vasundhra, Ghaziabad

Sir,

If I want to transact on line(means redemption,purchase etc.)its it possible since I have not purchased through my demat. A/C.

thanks

v y k

I oftenly check the market value of INHFI ISIN No. INE477L07040 on BSE.IN but from the past few days there is no value qouted on the site. Also when the NCD will redeemed at its maturity, will it redeemed at face value Rs. 1000/- or at the prevaling market value at that time? Please clearify! Thanks.

please told me yearly value of the NCD BOND ,FOLIO NO.002936 for rs.25000/- & folio no.002937 for rs.25000/- for income tax purpose

Interest Rate on Offer let me know

Sir, I am holding NCDs of IIHFL @12% but the monthly interest amount differs every month even for the months having 31days viz.,March,May,July,August etc., and the co.is so neglegent though form 15g submitted well in time TDS isdeducted at source and not refunding even claiming immediately and inspite asking me to claim with IT Dept. shows its non accountability.Pl.suggest in the matter

Dear Mr. Shiv,

I WAS WAITING FOR NTPC TAX FREE BOND WHICH WAS TO BE LAUNCHED IN 2ND WEEK OF MARCH 2014. CAN YOU PLEASE INFORM WHEN IT IS GOING TO OPEN? IF ITS NOT SHOWING UP I PROPOSE TO INVEST IN IRFC OR REC WHICH ARE STILL OPEN. WHICH ONE IS BETTER AND ASSURES FIRM ALLOTMENT.

MANY THANKS FOR INFORMATION

BEST REGARDS

I’ve already responded to your query at some other post.

Mr Shiv ,

can you pl. compare between 11.52% Secured & 12% Unsecured. ??

i want to invest 5 lacs but looks like previous 11.52% @ 970 gives better return and carry Rs 10 interest so getting at huge 4 % discount ?

Dear Dr. Agarwal,

I think the 11.52% NCDs are fairly valued at around Rs. 960-970 as its current issue is offering 12% annual interest. With a difference of 0.48%, one year of maturity and secured-unsecured nature of NCDs, I think it is quite difficult to make a choice. Personally, I would go for the current issue NCDs once they get listed on the stock exchanges.