This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

“Beti Bachao, Beti Padhao” is the mantra with which Prime Minister Narendra Modi launched Sukanya Samriddhi Yojana on January 22nd this year. Later on, the government issued a notification to allow 80C exemption equal to the amount invested in the scheme up to Rs. 1,50,000, which is also the maximum amount one can invest in this scheme in a financial year.

Now, the Finance Minister in his budget speech has proposed to make the interest component as well as the maturity proceeds as tax-free. I think this proposal has made this scheme to be the best small savings scheme available to the Indian investors. Yes, even better than our golden scheme of Public Provident Fund (PPF). So, what is this scheme all about? Let’s check.

Sukanya Samriddhi Yojana is a small savings scheme which can be opened by the parents or a legal guardian of a girl child in any post office or authorised branches of some of the commercial banks. The girl child is called the “Account Holder” and the guardian is called the “Depositor” in this scheme.

Before I compare this scheme with PPF, let us first check the important features of this scheme.

Salient Features of Sukanya Samriddhi Yojana

Who can open this account? – Parents or a legal guardian of a girl child who is 10 years of age or younger than that, can open this account in the name of the child. For initial operations of the scheme, one year grace period has been provided to make it 11 years of age. With this one year grace period in age, which is valid up to December 1, 2015, you can get this account opened for a girl child who is born between December 2, 2003 and December 1, 2004.

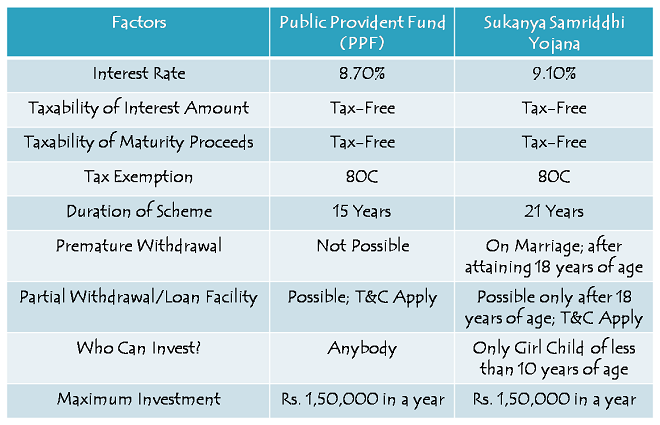

9.1% Tax-Free Rate of Interest – This scheme has been flagged off with a 9.1% rate of interest, higher than that of PPF which stands at 8.7%. But, this rate is not fixed at 9.1% for the whole tenure and is subject to a revision every financial year like all other small savings schemes, including PPF.

Prior to the budget announcement, 9.1% annual return seemed unattractive, but not anymore, as it has been made tax exempt now. Interest amount gets added to your balance amount in the account and compounded either monthly or annually, as per your choice. Monthly interest compounding will be done only on your balance amount on completed thousands.

Duration of the Scheme – The scheme will mature on completion of 21 years from the date of opening of the account. If the account is not closed on maturity after 21 years, the balance amount will continue to earn interest as specified for the scheme every year. In case the marriage of your daughter takes place before the maturity date i.e. completion of 21 years, the operation of this account will not be permitted beyond the date of her marriage and no interest will be payable beyond the date of marriage.

Deposit for 14 years only – Though the scheme has a duration of 21 years, you are required to make contributions only for the first 14 years, after which you need not deposit any further amount and your account will keep earning the interest rate applicable for the remaining 7 years.

Premature Closure – The account can also be closed prematurely as your daughter completes 18 years of age provided she gets married before the withdrawal. As the maximum permissible age of the girl child is set as 10 years, the scheme effectively carries a minimum duration of 8 years i.e. 18 years of exit age – 10 years of entry age.

Partial Withdrawal – It is also allowed to withdraw 50% of the balance standing at the end of the preceding financial year, but only after your daughter attains the age of 18 years. So, effectively it has a complete lock-in period of at least 8 years, before which you cannot take out any money for any purposes.

Minimum/Maximum Investment – You need to deposit a minimum of Rs. 1,000 in a financial year to keep your account active. Failure to do so will make your account inactive and it could be revived only after paying a penalty of Rs. 50 along with the minimum amount required to be deposited for that year, which currently stands at Rs. 1,000.

Also, you can invest a maximum of up to Rs. 1,50,000 in a financial year. You can make your contribution to this account in as many number of times as you like.

How many accounts can be opened? – You can open only one account in the name of one girl child and a maximum of two accounts in the name of two different children. However, you can open three accounts if you are blessed with twin girls on the second occasion or if the first birth itself results into three girl children.

Nomination Facility – Nomination facility is not available in this scheme. In an unfortunate event of the death of the girl child, the account will be closed immediately and the balance will be paid to the guardian of the account holder.

Documents Required – Birth Certificate of the girl child, along with the identity proof and residence proof of the guardian, are the mandatory documents required to open an account under this scheme. You can approach any post office or authorised branches of some of the commercial banks to get this account opened.

Sukanya Samriddhi Yojana vs. Public Provident Fund (PPF)

Budget 2015 has made this scheme quite attractive for the investors. If you’ve already exhausted your PPF deposit limit, want to save for your girl child’s marriage or higher education and have spare money to invest in this scheme, then this scheme provides you one more excellent avenue of safe investment with high returns. You can wait for the next financial year’s rate of interest to get announced anytime this month, if it remains higher than PPF, just go for it.

Application Form to open a Sukanya Samriddhi Account

List of authorised commercial banks where you can get this account opened

Sir to aap hi batao ki kitne saal tak pesa bhare or uske baad band kar de,or saal ka kitna pesa bhare ki 14saal,ya 21 Saal baad 6 lak mile

14 saal tak har saal Rs. 1,000 deposit karne pe aapko 21 saal baad approx. Rs. 52,605 milenge. Rs. 6 lakh ke liye aapko har saal Rs. 12,000 deposit karne padenge. Ye post check keejiye – http://www.onemint.com/2015/03/09/sukanya-samriddhi-yojana-calculating-maturity-value-after-21-years/

6000Lak nahi sir 6lak

Sir

Mene suna hai ki sukanya sammradhi yojana me post ofice me 1000 Rs 1saal ka14 saal tak bharne ke baad. 21Saal ke baad 6000lak milega

Jagdishji, ye information bilkul galat hai, aise logon pe bharosa mat keejiye.

Sir is yojana me kitne saal k liye kitne rupye JMA karwane par kitne rupye milenge plz reply sir

Maturity value ke liye please ye post check keejiye – http://www.onemint.com/2015/03/09/sukanya-samriddhi-yojana-calculating-maturity-value-after-21-years/

Can I open a SSY a/ c for my PIO card holder daughter

It is still not clear whether PIO card holders will be eligible for this scheme or not. Most likely they will not be eligible for this scheme, but you’ll have to wait some more time for further clarity.

Can V open a SSY account in the name of my daughter who is a PIO card holder. I am a Indian National

Sir,

I have 2 daughters and both are below 10 years old. i want to invest in ssa(sukanya yozona) in post office but some confusion arises, please .can you give me the following questions–

1. My Aadhar card address is in Bihar but i am living with family in orissa(by work), If i open a ssa in orissa post office then in future , can i transfer this account to my native place(bihar)???

2. can i invest 1.5 lakh each of my 2 daughters ssa a/c?total= 3 lakh??

4.In the ssa post office form- what should i write in 1st depositor column — my name or daughter name??

1. Yes, you can transfer it to your native place in future.

2. There is no clarity in this matter. I am assuming it is Rs. 3 lakh (Rs. 1.5 lakh for each girl child).

3. “Your daughter’s name” followed by “under guardian” “your name”.

what is sukanya samruddi yajana how much pay inmonthly

Please check the post above.

Hello sir my daughter born on 17 july 2005 and 20 july 2006 are they eligible for sukanya smridi scheeme

Yes, both are eligible for this account.

Hello Mr Shiv.. is residencial proof from form is compulsory for government employees.they traveled one place by other places yearly or few years once.

Hi,

Yes, address proof is required for opening this account. You cannot open an account without providing it.

Sir,

Mera beti ka DOB 17.08.14 kya me ye kar sakta hu?post office me or bank me bi khata khulbana parega?purana bank me account hai to chalega?

Please reply sir

Tanmoyji, aap ye account khulwa sakte hain, aapki beti eligible hai. Post office or bank branch mein khata khul jaayega. Puraane bank mein khata khulega ya nahin, ye bank batayega.

Hi Sir,

You have mentioned that in case of daughter gets married before completion of 21 years of opening the account, operation of this account will not be permitted beyond the date of her marriage and no interest will be payable beyond the date of marriage.

Suppose my daughter age is 9 years now and i am opening the account, and she gets married at the age of 25, will the account be closed after 16 years? and how will they know when my daughter gets married? Do we need to submit marriage certificate?

Yes, the account will have to be closed as your daughter gets married after 16 years.Also, I am not sure what you would be required to produce as marriage proof, but I think a declaration from the girl child or the marriage certificate or wedding invitation card would work as a proof.

Hi,

my daughters birth date is 1jan.2008 can we apply for this scheme.

Yes, you can open the account.

Hello sir,

my daughters birth date is 1jan.2008 can we apply for this scheme.

Yes, you can do that.

Hi Shiv,

Thanks for your efforts on this forum. Today’s TOI edition carried an article on the SSY scheme where they say, the maximum cap is 1.5L per financial year per family of 2 children. I believe this is not correct because it would then render the cap of 2 accounts for 2 children meaningless. Please clarify if it is 1.5L per account upto a max of 2 accounts which means one could deposit upto 3L though the 80c limit would still be only 1.5L.

Further, have any banks started opening accounts as on date. Any info on this?

Thanks for your kind words!

What has been mentioned in the post above is based on the wordings of the Circular – “the total money deposited in an account on a single occasion or on multiple occasions shall not exceed one lakh fifty thousand rupees in a financial year”.

Source: http://www.indiapost.gov.in/dop/Pdf%5CCirculars%5Csukanya_samriddhi_SB_Order_2.pdf

So, I think what I have mentioned holds correct. As you rightly mentioned, Rs. 1.5 lakh split between two daughters will leave the maturity value significantly insufficient for meeting their future education & marriage expenses.

There are viral shares on social media claiming the maturiy amount of Rs. 6,00,000/- for Sukanya Suraksha scheme after 14 years. Does this have validity? I have calculated with Rs.1000/- principal every year with 9.1% p.a. interest compounded yearly for 14 years, followed by compound intererst for the next 7 years. This gives me maturiy amount of Rs. 52,602/-. Am I missing something?

By the way, thanks for educating the people!

sreekar

No, you are not missing anything & your calculation is correct. People are getting misguided with Rs. 6 lakh figure.

Moreover, thanks for your kind words!

Can you please explain how the interest is calculated for every year. For Example if im depositing 12000 per year, then if we calculate the interest for 12000 x 9.1%, it comes to 1092. Can you please explain me why im going wrong in this ?

Mr. Dinesh, your calculation is correct. Rs. 1,092 should be the first year’s interest if you deposit Rs. 12,000 in the beginning of the year and rate of interest is 9.10%. So, why are you asking that where are you getting wrong? You are nowhere wrong.

Please check this post for maturity value tables – http://www.onemint.com/2015/03/09/sukanya-samriddhi-yojana-calculating-maturity-value-after-21-years/

First year for interest calculation ( 6.5 months deposits ) has been taken, the balance will be taken (5.5 months deposits) where added at 15th year, while the exact is matching with the chart given

Hi sir,

Pls tell me, 1000 pay every month.ya every year

Minimum Rs. 1,000 once every year is required and not every month.

can we increase the monthly installment later if we started by 1000 each month

Yes, you can do so. Also, it is not mandatory to make monthly contributions, one contribution in a year is good enough.

Hi Shiv,

Thanks for such good information and the way you are helping..

Just small question :

ONLINE : Can we transfer amount online or each time we have to go in post office and need to do payment of same.

Thanks in advance.

Thanks Rohan,

In a fews days time, commercial banks including SBI, ICICI, Axis etc. will start opening these accounts and with them you will definitely have online transfer facility.

Dear Shiv sir,

Thanks for the information (SSY)

You are welcome!