This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

88% of India’s total labour force of 47.29 crore belongs to the unorganised sector, in which the workers do not have any formal provision of getting a regular pension payment on retirement. Moreover, due to increasing labour wages and better medical facilities, these people also face a risk of increasing longevity. So, this work force would require some kind of assured income guarantee to sustain itself in the coming years.

Launching Atal Pension Yojana (APY) from June 1, 2015

To encourage workers in the unorganised sector to voluntarily save for their retirement, the government of India will be launching a new scheme, called Atal Pension Yojana (APY), from 1st June, 2015. Finance Minister Arun Jaitley announced this scheme in his budget speech on February 28th.

This scheme will replace the UPA government’s Swavalamban Yojana – NPS Lite and will be administered by the Pension Fund Regulatory and Development Authority (PFRDA). The benefits of this scheme in terms of fixed pension will be guaranteed by the government and the government will also make contribution to these accounts on behalf of its subscribers.

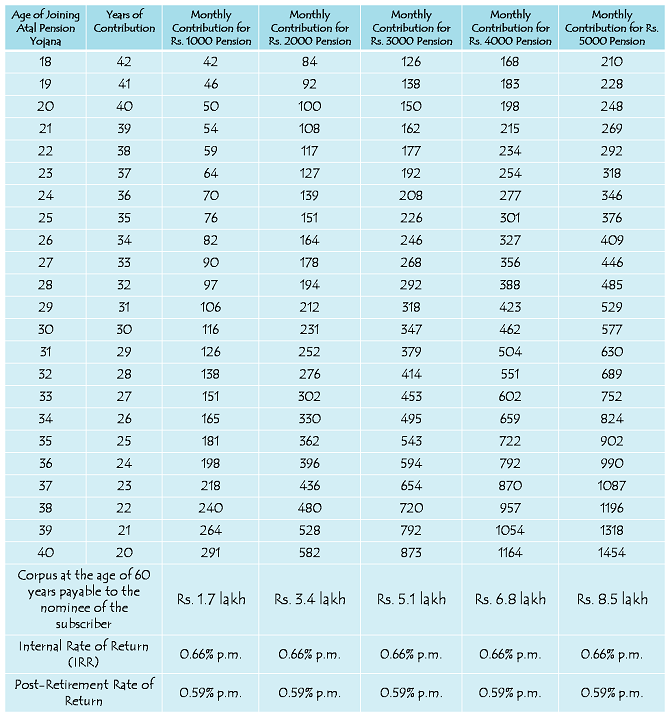

Under this scheme, a subscriber would receive a minimum fixed pension of Rs. 1,000 per month and in multiples of Rs. 1,000 per month thereafter, up to a maximum of Rs. 5,000 per month, depending on the subscriber’s contribution, which itself would vary on the age of joining this scheme.

The minimum age of joining this scheme is 18 years and maximum age is 40 years. Pension payment will start at the age of 60 years. Therefore, minimum period of contribution by the subscriber under APY would be 20 years or more.

The Central Government would also co-contribute 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower, to each eligible subscriber account, for a period of 5 years, i.e., from 2015-16 to 2019-20, who join the NPS before 31st December, 2015 and who are not income tax payers. The existing subscribers of Swavalamban Scheme would be automatically migrated to APY, unless they opt out.

Who is eligible for Atal Pension Yojana?

Any Citizen of India, aged between 18 years and 40 years, who has his/her savings bank account opened and also possesses a mobile number, would be eligible to subscribe to this scheme.

Government Funding – Indian Government would provide (i) fixed pension guarantee for the subscribers; (ii) would co-contribute 50% of the subscriber contribution or Rs. 1,000 per annum, whichever is lower, to eligible subscribers; and (iii) would also reimburse the promotional and development activities including incentive to the contribution collection agencies to encourage people to join the APY.

Who is eligible for Government Co-Contribution in Atal Pension Yojana?

Subscribers of this scheme, who are not covered under any other statutory social security scheme and are not income tax payers, would be eligible for the government’s co-contribution of up to Rs. 1,000 per annum.

Social Security Schemes which are not eligible for Government Co-Contribution

- Employees’ Provident Fund (EPF) & Miscellaneous Provision Act, 1952

- The Coal Mines Provident Fund and Miscellaneous Provision Act, 1948

- Assam Tea PlantationProvident Fund and Miscellaneous Provision, 1955

- Seamens’ Provident Fund Act, 1966

- Jammu Kashmir Employees’ Provident Fund & Miscellaneous Provision Act, 1961

- Any other statutory social security scheme

Minimum/Maximum Pension Payable – This scheme will pay a minimum pension of Rs. 1,000 per month and a maximum pension of Rs. 5,000 per month, depending on the subscriber’s own contribution per month.

Minimum/Maximum Period of Contribution – As the minimum age of joining APY is 18 years and maximum age is 40 years, minimum period of contribution by the subscriber under this scheme would be 20 years and maximum period of contribution would be 42 years.

Atal Pension Yojana – Contribution Period, Contribution Levels, Fixed Monthly Pension and Return of Corpus to the Nominees of Subscribers

Internal Rate of Return (IRR) – Thanks to the government funding of Rs. 1,000 per annum per subscriber account for 5 years, your account would generate an IRR of approximately 0.66% per month or 8% per annum. This pension amount per month is fixed and the government has made it clear that if the actual returns on the pension contributions are higher than the assumed returns, such excess return will be credited to the subscribers’ accounts, resulting in enhanced pension payment to the subscribers.

Minimum Contribution – A subscriber aged 18 years will have to contribute a minimum of Rs. 42 per month in order to get Rs. 1,000 pension per month starting 60 years of age. For a 40 years old subscriber, his/her minimum contribution would be Rs. 291 per month. The contribution levels would vary and would be low if subscriber joins early and increase if he joins late.

Maximum Contribution – A subscriber aged 40 years will have to contribute Rs. 1,454 per month in order to get Rs. 5,000 pension per month starting 60 years of age. For a 18 years old subscriber, his/her contribution for Rs. 5,000 monthly pension would be Rs. 210 per month.

Can I increase or decrease my monthly contribution for higher or lower pension amount?

The subscribers can opt to decrease or increase pension amount during the course of accumulation phase, as per the available monthly pension amounts. However, the switching option shall be provided only once in a year during the month of April.

What will happen if sufficient amount is not maintained in the savings bank account for contribution on the due date?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re. 1 to Rs. 10 per month as shown below:

(i) Re. 1 per month for contribution upto Rs. 100 per month

(ii) Rs. 2 per month for contribution upto Rs. 101 to 500 per month

(iii) Rs. 5 per month for contribution between Rs. 501 to 1,000 per month

(iv) Rs. 10 per month for contribution beyond Rs. 1,001 per month.

Discontinuation of payments of contribution amount shall lead to following:

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Post-Retirement Rate of Return – Considering a retirement corpus of Rs. 1.7 lakh and monthly pension of Rs. 1,000, this scheme is going to generate a return of 0.59% per month or 7.1% per annum for its subscribers. I think this return is also on a lower side.

Nomination Facility – This scheme will also provide the nomination facility to its subscribers. In case of the subscriber’s death after attaining 60 years of age, the whole corpus generating the pension income to the subscriber would be returned back to the nominee of the subscriber. In case of untimely death of the subscriber before 60 years of age, the balance would be returned back to the nominee of the subscriber.

Where to open APY Accounts – You need to approach points of presence (PoPs) and aggregators under existing Swavalamban Scheme. These agencies would enrol you through architecture of National Pension System (NPS).

Points of Presence & Aggregators

Application Form – Here you have the links to the application form for subscribing to Atal Pension Yojana – Application Form in English – Application Form in Hindi

I think a subscriber should opt for a minimum monthly contribution of around Rs. 167 or so, which would make it approximately Rs. 2,000 annual contribution. 50% of Rs. 2,000 i.e. Rs. 1,000 would be contributed by the government as well. So, the subscriber will get the maximum benefit of government funding.

As mentioned above, the scheme would start from June 1, 2015. So, interested people will have to wait till then to open an account. If you have any other query regarding this scheme, please share it here.

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Hi,

I am working in private sector and I am continuing LIC superannuation plan as per company policy.

May I eligible for this plan as superannuation plan is already exist.

please suggest..

Thanks in advance

Ash

Hi Ash,

You are eligible for this scheme, but you might not get the government contribution.

sir a friend of mine who is unemployed & her husband is working in private sector earning about Rs20,000 p.m wants to apply for APY is she eligible.

Yes Saroj, if your friend is younger than 40 years of age, then she is eligible for this scheme.

My DOB is 3rd June 1975 and My Age is 40 years One month and 14 days. I went to State Bank of India today with Atal Pension Yojana application but SBI is not accepting my application stating that I’m already crossed age 40. Is there any grace period after crossing age 40? Is there any rule? Please advice…

Hi Jayakanthan,

You should try some other bank. I think different banks are adopting different rules for opening these accounts.

dear sir,

This is Samiran from Howrah …

sir after maturity how can i get the pension & after my death how can my spouse can claim the amount? & how canshe get pension amount?

Hi Samiran,

You’ll get the pension amount in your bank account through ECS. After you, your spouse will get your pension amount transferred to her account by getting the bank details changed.

Hi Shiv, I had several e-mail interaction with CRA(i.e., NSDL) and they are not confirming on whether we get back Swavalamban amount on attainment of 60 years or not. Now my Swavalamban amount is stuck forever in APY after migration. No clarity is emerging on this issue either from PFRDA or NSDL.

Hi Ramprasad,

I don’t believe that the subscribers will not get their Swavalamban balance after 60 years of age. You’ll definitely get back your balance in the account.

It is unfortunate that neither CRA(i.e.,NSDL) nor PFRDA is confirming on this. What I heard from my aggregator is that Swavalamban amount will be paid only to nominee after the death of subscriber and not before that and this swalamban amount will not earn any additional pension after attainment of 60 years. This is very ridiculous.

Respected

Sir This is Anup from Kolkata

I have submitted Apy application on jun 16/2015,but no pension amount has been recovered from my account till to date.the Uco Bank kolkata Rajarhat branch told me that the amount will be deduct 1 june.also i am not any activation msg……

What should i do sir???????

Hi Anup,

You need to contact your bank for the same.

Please reply on my post

What is benefit if i migrate my swavalaban fund in atal pension yojna

There is no benefit. Your Swavalamban fund gets stuck in APY. Better would be to withdraw your funds from Swavalamban scheme by closing the account and then open APY account afresh.

Sir,

I hve two doubts,

1. Now i am opening APY in bank of baroda, if can not continue this bank account in future, can i convert APY scheme from this bank account to another bank account in future.

2. I have only jan dhan yogana account. Can i open APY in this account.

Hi Murali,

1. Yes, you can transfer your account from BoB to some other bank in future.

2. Yes, you can open APY with Jan Dhan Yojana account.

Is there any difference between EPF & FP?

What is FP Arup?

What is the different between EPF & PF?

There is no difference between EPF & PF, these terms are used interchangeably for Employees’ Provident Fund.

I am a govt. employee and joined service after 1-jan-2004 and thus subscriber of NPS(National Pension System) and have PRAN no. as well as PRAN card alloted to me. I am also I. tax payer. Can I join APY and can anyone have 2 PRAN no.?

Hi Ravi,

You can join APY, but you won’t get the government contribution.

One question- is there any different between EPF & FP? or both are same.

dear shiv nhpc has already raised 1500 crore by issuing bonds tomorrow though private placement with coupon rate of 8.50 so can we accept similar coupon rates in upcoming taxfree bond 2015 I have invested heavily 13-14 taxfree bond of nhb tf2014 and is currently trading at a premium of 1200 per bond so I will need your advice this year also

Hi Nitesh,

It is PFC, and not NHPC, which has raised the money through a private placement. Also, I’ll cover these issues as their details get announced.

A word of caution and suggestion to subscribers who are intending to migrate from Swavalamban to APY. If you allow your account to migrate from Swavalamban to APY, the balance so transferred from Swavalamban to APY will be stuck forever and you will neither be able to withdraw that amount nor will earn any interest on that Swavalamban amount. The transferred amount will be kept separately in APY and will not be adjusted to monthly contribution under APY and will not be paid to subscriber. Whether the same will be paid to subscriber after 60 years is also not sure. CRA is not confirming on this. So your Swavalamban amount will be at risk of loosing. Hence it is my advise to all subscribers to withdraw their amount by closing NPS-Swavalamban account (opting out of NPS Swavalamban) and to open APY account afresh so that they can get back their entire amount balance accrued in their Swavalamban account.

Hi Ramprasad,

I don’t think the problem would be so severe. I think the amount would earn interest and you could withdraw the amount at the age of 60.

Hi Shiv, I had several e-mail interaction with CRA(i.e., NSDL) and they are not confirming on whether we get back Swavalamban amount on attainment of 60 years or not. Now my Swavalamban amount is stuck forever in APY after migration. No clarity is emerging on this issue either from PFRDA or NSDL.

I already exist swavalaban yojna and i have PRAN no. I will fill a form of atal pension yojna what to,do me

what wil happen, if ill break this scheme before completing 60 years?

what will be the next process for accumulated amount?

Hi Kanchan,

You cannot break this scheme before 60 years of age.

where can I get the physical statement of transaction of atal pension yojana?

Hi Avik,

You will either get the physical statement delivered at your address or you can get it from the aggregator.

Sir please tell me If I am not elligeble for govt contribution due to continuetion of provident fund, then there is any iffect on my pension figur for which I paid a determine figure.

Are there extra benifit if I pay in advance premium for 24 month

Hi Mr. Soni,

1. If your account doesn’t get the government contribution, then your pension amount will be lower than the pension amount you would have got had your account received the government contribution.

2. There is no option to make advance contributions.

We have started yojana scheme in our mother name she give her son name as nominee but now she wanted to change the nominee to her daughter name if we approach the bank the staff are not accepting to alter it ,but it’s our rights to do os help please

Hi Priya,

You need to approach the bank itself to get the nominee details changed. In case the bank doesn’t cooperate, you can approach PFRDA to register your complaint.

Dear Sir,

I would like to tell you that the Indian Government has been introduced a very good Scheme : (Atal Pension Yojana 2015) to our low income Indian citizen.

In order to avail this APY scheme, I have some below quires:

1. Currently I’m working with a Private company and they are deducting PF amount from my salary in every month, so, in that case, Can I avail APY Scheme 2015 ?

2. For financail issue if I can’t contribute to APY Scheme in future, in that case, Shall I get the scheme benefit and what is the procedure of the refund amount ?

Thanks & Regards

Parimal Das

Hi Parimal,

1. You can join APY, but you won’t get the government contribution.

2. You cannot withdraw money from this account before 60 years of age. In case you are not able to contribute on a regular basis, the account could become inactive.