This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Having gained 20-30% on their investments made in tax-free bonds a couple of years back, investors’ hunger for tax-free bonds has grown considerably. With IRFC issue worth Rs. 4,532 crore getting 2.38 times oversubscribed on the first day itself, there seems to be no slowdown in the subscription demand for these bonds.

To cash-in on this huge demand and ending a long wait for its tax-free bonds, NHAI, which filed its draft shelf prospectus in the first week of October, will be launching its first tranche of tax-free bonds from the coming Thursday i.e. 17th December. As the issue size is considerably quite big at Rs. 10,000 crore, I hope most of the retail investors are able to get their share of bonds allotted at least this time around. The issue is officially scheduled to remain opened for two weeks and will get closed on December 31st.

Before we analyse it further, let us first quickly check the salient features of this issue:

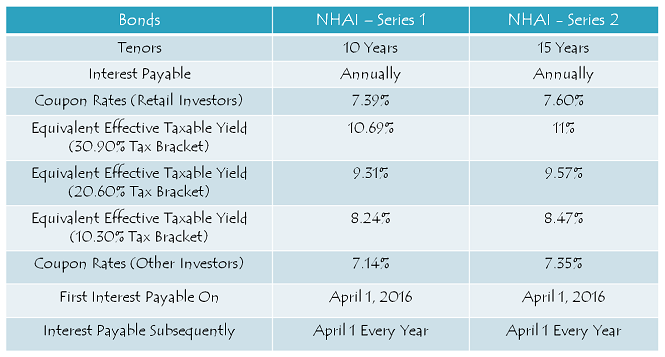

Size of the Issue – NHAI is authorized to raise Rs. 24,000 crore from tax free bonds this financial year, out of which the company has already raised Rs. 3,872 crore by issuing these bonds through a private placement. Out of the remaining Rs. 20,128 crore, the company will raise Rs. 10,000 crore in this issue.

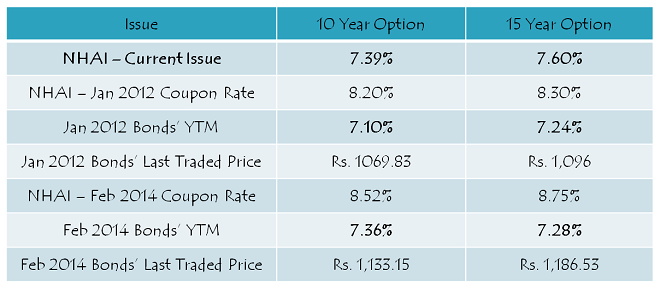

Coupon Rates on Offer – With rising G-Sec yield, earlier IRFC and now NHAI, both have been able to offer higher coupon rates as compared to PFC and REC. While IRFC offered 7.53% for the 15-year period and 7.36% for the 10-year period, NHAI is offering an even higher rate of interest at 7.60% for 15 years and 7.39% for 10 years.

For the non-retail investors, these rates would be lower by 25 basis points (or 0.25%).

Rating of the Issue – CRISIL, ICRA, CARE and India Ratings consider investing in these bonds to be safe and as a result, have assigned ‘AAA’ rating to the issue. Also, these bonds are ‘Secured’ in nature i.e. in case of any default, the bondholders would carry a right to make claim on certain assets of the company.

NRI/QFI Investment NOT Allowed – Unlike PFC, REC & IRFC issues, Non-Resident Indians (NRIs) won’t be able to make investment in this issue. Qualified Foreign Investors (QFIs) are also not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 20% of the issue is reserved i.e. Rs. 2,000 crore

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved i.e. Rs. 2,000 crore

Category III – High Net Worth Individuals including HUFs – 20% of the issue is reserved i.e. Rs. 2,000 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 4,000 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing & Allotment – NHAI has decided to get these bonds listed on both the stock exchanges, National Stock Exchange (NSE) as well as Bombay Stock Exchange (BSE). The company will allot the bonds and get them listed within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – It is not mandatory to have a demat account to apply for these bonds. Investors have the option to subscribe to these bonds in physical form as well. Whether you apply for these bonds in demat or physical form, the interest payment will still get credited to your bank account through ECS.

Also, even if you get these bonds allotted in your demat account, you have the option to rematerialize your holding in physical/certificate form if you decide to close your demat account in future.

No Lock-In Period – These tax-free bonds are freely tradable and do not carry any lock-in period. The investors may sell them at the market price whenever they want after these bonds get listed on the stock exchanges within 12 working days of the closing date.

Interest on Application Money & Refund – Successful allottees will earn interest at the applicable coupon rates i.e. 7.39% p.a. for 10 years and 7.60% p.a. for 15 years, on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of face value Rs. 1,000 each. There is no upper limit for the investors to invest in this issue. However, an investor investing more than Rs. 10 lakhs will be categorized as a high networth individual (HNI) and will get a lower rate of interest as applicable.

Interest Payment Date – NHAI will make its first interest payment on April 1st next year and subsequent interest payments will also be made on April 1 every year, except the last interest payment, which will be made to the bondholders along with the redemption amount on the maturity date.

Record Date – For the payment of interest or the maturity amount, record date will be fixed 15 days prior to the date on which such amount is due to be payable.

Should you invest in this issue?

NHAI tax-free bonds issued in February 2014 are quoting at a yield to maturity (YTM) of 7.28% with the closing market price of Rs. 1,186.53. Also, bonds issued in January 2012 are carrying 7.24% yield and last traded at Rs. 1,096 on Friday.

Taking a clue from these already listed bonds, I think subscribing to the 15-year option makes more sense. Risk-averse investors with a long term view should definitely invest in these bonds. In the short-term as well, you can expect some listing gains with these bonds.

Application Form for NHAI Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHAI tax-free bonds, you can contact me at +919811797407

got them in my demat

That’s great! So, trading should start by Wednesday I guess.

Hi Shiv,

In Demat account under ISIN description something is mentioned like this “SR IIB 7.6 BD 11JN31 FVRS1000”

Can you please spare some time to explain the meaning of these terms?

Thanks in advance.

Regards,

Vineet Garg

Hi Vineet,

It is “Series IIB 7.60% Bond 11th January, 2031 Maturity Date Face Value Rs. 1,000”.

just got message from cdsl applied for 150 bonds and get full allotment and plus my agent will give back me rupees 500 as intensive to me so it is far better to get full allotment at 7.60 rather than 7.74 with only 55% allotment only .14 paisa is the difference between nhai triple rated & irdea double rated company what you say dear shiv

not much difference interest

Hi Nitesh,

No comments on the agent commission you have received. But, personally I prefer a better company to invest my money, so I think between NHAI and IREDA, I would go with NHAI.

Hi Shiv, by when do you think the allotted bonds should get credited to the demat account (with ICICI Direct in this case)?

Thx.

Hi SG,

Allotment will start from today evening and the bonds should start reflecting in your demat/trading account as soon as the trading starts. However, for ICICI Direct, I have heard that you need to get your bonds credited to your trading account for selling them. I don’t know the exact procedure though.

Any news on NHAI trabche 2 for fy 2015-16 yet? When are they getting announced and expected rate of interest will be ?

Hi RS,

There is no info provided by NHAI about its 2nd tranche of tax-free bonds. I’ll keep this post updated as soon as I have any info. But, don’t expect that issue to come soon, as the company is yet to allot bonds for its 1st tranche. Also, NHAI doesn’t seem to be over enthusiastic about raising huge money going forward.

NHAI has allotted the bond. Amount has been deducted which was on hold. 100 % allotment.

Thanks Pankaj for this info!

Hi Shiv,

I am Comparing NHAI issue & IREDA issue, wrt Subcription numbers.

On Day1 of NHAI, Institution Subscription was 4 times, while in this issue its till now less than 0.7 times.

Why institutions are staying away from this small issue.. while they were madly interested in bigger issue of NHAI ?? when its offering higher rate.

Hi Rohit,

QIBs normally prefer bigger issuers to invest their money, like NTPC, NHAI, IRFC, REC etc. A slightly higher rate of interest does not matter much to them.

Hi Shiv

I have applied for NHAI Tranche-I Series 2B Tax Free Bonds, whose last date of submission was 31.12.2015. May I know its allotment status.

Regards.

Anjan

Hi Anjan,

Allotment will start from tomorrow or Monday, so you’ll get message from the company as & when the allotment happens.

When will be the NHAI bond allocated. Say we get the bonds allocated in the Demat account and hold it till it matures will the bond will be automatically redeemed or need to sell to the company on the maturity date

Hi Vinod,

NHAI bonds are expected to get allocated by tomorrow or Monday. Also, you need to do nothing on maturity, bonds will automatically get extinguished on maturity and maturity proceeds will get credited in your bank account.

Hi Shiv – the Retail Category (IV) is not subscribed fully. This means everyone will get the allocation.

Hi Parag,

Yes, every successful applicant will get full allotment.

Sir maine nhai bond me 120 bond ke liye apply kiya hua hai .kya aap bata sakte hai ki iski listing date kab hai aur kitna premium milne ki sambhavna hai

Hi Rajneesh,

NHAI bonds ki listing date abhi announce nahin ki gayi hai, but I think by Tuesday or Wednesday listing ho jaani chahiye. Also, I think NHAI bonds mein maximum 1-2% listing gain hoga. Kam bhi ho sakta hai.

Hi Shiv,

The issue was closed on 31st Dec, do you know when the allotment of bonds will take place

thanks

Hi Parag,

NHAI allotment should happen by tomorrow or Monday.

HDFC’s Keki Mistry, media entrepreneur Raghav Bahl, Bollywood bid for Rs 10,000-crore NHAI bonds

http://economictimes.indiatimes.com/articleshow/50460497.cms

Reliance invested Rs. 350 crore, SBI Rs. 3,000 crore, Akshay Kumar Rs. 65 crore and Kareena & Karishma Rs. 25 crore between them. Axis Bank, IDFC Bank and Yes Bank put in between Rs. 500 crore to Rs. 1,500 crore.

Tax free bonds..

Chirag Gandhi 07:22AM

To: skukreja@investitude.co.in

Hello,

I am a subscriber of One Mint.

I had been alloted 791 bonds from the IPO.

I wish to know if I buy more IRFC bonds from the market will I get the same rate of Interest at 7.5 percent or less?

Can I buy any number of bonds or my total holding has to be less than 1000 to be considered as a retail investor?

I am a bit confused whether I should subscribe for new offers which are yet to come or are there any existing bonds available in the market whose effective yield is better?

I am interested in buying bonds with highest possible tenure say 15-20 yrs.. And which offer best net effective yield.

Can u pls guide me on this.

Thanking you,

Regards,

Chirag Gandhi

Hi Chirag,

1. You’ll get 7.50% rate of interest if your total holding does not exceed 1,000 bonds in the IRFC issue.

2. I think you can subscribe to the IREDA bonds issue which is opening on 8th of January – http://www.onemint.com/2016/01/02/ireda-7-74-tax-free-bonds-january-2016-issue/

Hi Shiv,

I hold 200 NHAI bonds (for 10 years) allotted from 2013-2014 Tranch 1. I have applied for 1000 bonds (for 15 years) as part of retail category in NHAI Tranch 1 (Dec 2015). Will I get the same rate of interest as that of retail investors – 7.6%?

Hi Janaki,

Yes, you’ll get 7.60% rate of interest.

IREDA 7.74% Tax-Free Bonds Issue – http://www.onemint.com/2016/01/02/ireda-7-74-tax-free-bonds-january-2016-issue/

Final Day (December 31) subscription figures:

Category I – Rs. 8,160.04 crore as against Rs. 2,000 crore reserved – 4.08 times

Category II – Rs. 7,081.32 crore as against Rs. 2,000 crore reserved – 3.55 times

Category III – Rs. 3,494.16 crore as against Rs. 2,000 crore reserved – 1.74 times

Category IV – Rs. 3,420.07 crore as against Rs. 4,000 crore reserved – 0.84 times

Total Subscription – Rs. 22,155.60 crore as against total issue size of Rs. 10,000 crore – 2.22 times

last time ireda was triple rated then why this time A is company is making some losses or something else and dear shiv which one you will prefer hudco or ireda as both are known A

Yes Shiv, would be great if you can give some insight on this. Both IREDA and HUDCO have A+ rating. Which one would you give more preference to?

Hi Nitesh & Nishi,

IREDA is AA+ and not A/A+ as you mentioned. No doubt ‘AAA’ rated bonds are considered to be the safest of the lot, but I don’t think it is a matter of huge concern to have AA+ rating for a PSU. Moreover, I don’t have any personal bias for or against IREDA & HUDCO, I think both are equally good companies to invest in.

Please let us have full detail on IREDA & HUDCO tax free bond..opening date with interest rate for category IV-retailors..

Dear Shiv Happy new year

Good news Ireda 7.74%,thanks for update

and also kindly clarify New irfc 7.53% trading in Nse NJ series.This 7.53% in retail category issued.when we buy in secondary market (Nse or Bse) same 7.53% interest we can get?

Thank you Raju, you too have a wonderful 2016!

Yes, you’ll get 7.53% interest with IRFC bonds if your investment amount does not exceed Rs. 10 lakh on the Record Date.

Good Morning Shiv

Actually i received 791 bonds in first allotment.and i want to buy in secondary market (Nse or Bse).Showing 7.53% irfc Nj series.already record date is Dec 21st 2015.

Now i need clarification there is any limit is there for get 7.53%interest when we buy in secondary market.

Good Afternoon Raju!

Yes, there is a limit of Rs. 10 lakh for you to get 7.53% interest. If your investment in this issue exceeds Rs. 10 lakh, then you’ll get 7.28% interest.

IREDA (AA+) coming on 8th Jan…Retail 7.74% 15 Years and 7.68% 20 Years

Thanks for the update.. helps!!

thanks.. helps to plan

Thanks Sanjay for the update!

Just as a piece of information.

I checked yield of various tax free bonds (including recently issued) and all trade around 7.30%, only exception to this is NEW 7.53% IRFC bond which is trading at pat i.e. 7.53% (Listed on 28th Dec).

Old IRFC trades at 7.30%.

Hope New NHAI doesn’t follow this exception New IRFC.

Been a long time since i invested in one of these.. But the concept is of interest on allotment money.. From the date of debit to your account to the allotment date.

The tax free interest starts from the date of allotment of bonds.

It is just a matter of time that new IRFC bonds will also start trading at par with other/older tax-free bonds.

Tax-free bonds give better returns than tax-saving FDs – http://www.business-standard.com/article/pf/tax-free-bonds-give-better-returns-than-tax-saving-fds-115122900709_1.html

Dear Mr. Shiv, I had applied for Bonds in HNI category. However very few bonds were eventually allocated for less than 2L value. Since amount of allotment is less than the 10L limit I was classified as HNI. If I buy other bonds of same company from Retail Investors from Market which were at higher coupon rate, I understand I will get lower rate of HNI due to clubbing through PAN. Is this accurate? In case I buy other TFB’s Series of same company in retail category from open market will I again get lower coupon rate?

Hi S.K.,

You would get higher coupon rate in both the cases above.