This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

IRFC 7.64% Tax-Free Bonds Issue – Tranche II – March 2016 Issue

It has been a very long time since NHAI filed the draft shelf prospectus for its tax-free bonds issue in the first week of October. Investors have been desperately waiting for a bigger issue as all the previous issues by NTPC, PFC and REC have left them fairly disappointed.

All these issues were of smaller sizes of Rs. 700 crore each and got hugely oversubscribed on the first day itself. But, before NHAI could make it, IRFC has taken the lead to launch its tax-free bonds from the coming Tuesday i.e. December 8th.

As the issue size is quite big, I hope it does not get oversubscribed on the first day itself and the retail investors get full allotment at least this time around. The issue is scheduled to get closed on December 21st.

Before we analyse it, let us first quickly check the salient features of this issue:

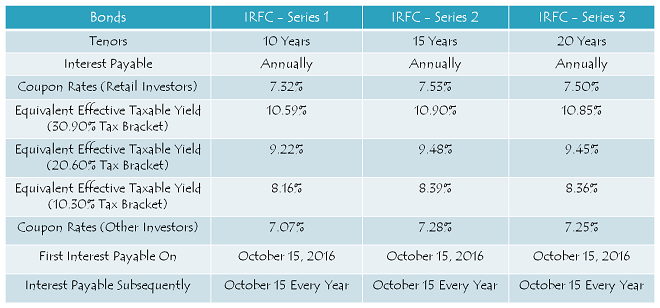

Size of the Issue – IRFC is authorized to raise Rs. 6,000 crore from tax free bonds this financial year, out of which the company has already raised Rs. 1,468 crore by issuing these bonds through private placements. The company will raise the remaining Rs. 4,532 crore in this issue.

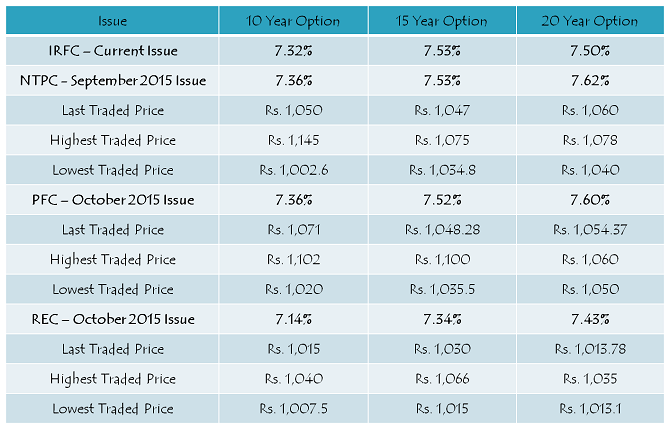

Coupon Rates on Offer – REC offered 7.43% as its highest rate of interest for the 20-year investment period. Due to a sharp reversal in G-Sec rates, coupon rates for this issue have risen by 0.07% to 0.19%. IRFC will offer yearly rate of interest of 7.32% for its 10-year option, 7.53% for the 15-year option and 7.50% for the 20-year option to the retail investors investing less than or equal to Rs. 10 lakh.

As always, these rates would be lower by 25 basis points (or 0.25%) for the non-retail investors.

Rating of the Issue – CRISIL, ICRA and CARE consider investing in these bonds to be safe and as a result, have assigned ‘AAA’ rating to the issue. Also, these bonds are ‘Secured’ in nature and in case of any default, the bondholders would carry a right to make claim on certain assets of the company.

NRI/QFI Investment Allowed – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as non-repatriation basis. Unlike earlier issues, Qualified Foreign Investors (QFIs) are also allowed to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 15% of the issue is reserved i.e. Rs. 679.80 crore

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved i.e. Rs. 906.40 crore

Category III – High Net Worth Individuals including HUFs & NRIs – 25% of the issue is reserved i.e. Rs. 1,133 crore

Category IV – Resident Indian Individuals including HUFs & NRIs – 40% of the issue is reserved i.e. Rs. 1,812.80 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing & Allotment – IRFC has decided to get these bonds listed on both the stock exchanges, National Stock Exchange (NSE) as well as Bombay Stock Exchange (BSE). The company will allot the bonds and get them listed within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – It is not mandatory to have a demat account to apply for these bonds. Investors have the option to subscribe to these bonds in physical form as well. Whether you apply for these bonds in demat or physical form, the interest payment will still get credited to your bank account through ECS.

Also, even if you get these bonds allotted in an electronic form, you have the option to rematerialize your holding in physical/certificate form if you decide to close your demat account in future.

No Lock-In Period – These tax-free bonds are freely tradable and do not carry any lock-in period. The investors may sell them at the market price whenever they want after these bonds get listed on the stock exchanges within 12 working days of the closing date.

Interest on Application Money & Refund – Successful allottees will earn interest at the applicable coupon rates on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of face value Rs. 1,000 each. There is no upper limit for the investors to invest in this issue. However, an investor investing more than Rs. 10 lakhs will be categorized as a high networth individual (HNI) and will get a lower rate of interest as applicable.

Interest Payment Date – IRFC will make its first interest payment on October 15 next year and subsequent interest payments will also be made on October 15 every year.

Record Date – For the payment of interest or the maturity amount, record date will be fixed 15 days prior to the date on which such amount is due to be payable.

Should you invest in this issue?

Long-Term Potential – While the sentiment for real estate and gold investments has already been pretty negative, stock markets are once again testing risk appetite of the retail investors. Conservative investors can do nothing but invest in fixed deposits or explore some other relatively safer options like debt funds or tax-free bonds.

A sharp reversal in the G-Sec yield has again given an opportunity to the investors to invest at higher coupon rates. I personally think that India should have a relatively lower inflationary scenario in the next 3-5 years as compared to the previous few years. If you also have the same view and if you want to earn tax-free interest on your investments for the longest possible period of time, then I think you should opt for the 20-year bonds which carry 7.50% rate of interest. The 15-year option with 7.53% is also equally attractive with a relatively shorter investment period.

Listing Gains – IRFC is offering 7.53% rate of interest for its 15-year option, which is also the highest rate of interest for its bonds across all three options. NTPC issue also carried the same 7.53% rate of interest for its 15-year option. As you can check from the table above, NTPC 15-year bonds last traded at Rs. 1,047 on Friday on the NSE i.e. a 4.7% premium to its issue price. Even if I consider Rs. 12-15 premium to be the accrued interest for the 2-month period since listing, these bonds are still earning a natural premium of approximately 3-3.50%.

Even the REC 15-year bonds, which got listed on November 5th on the BSE and carried a lower rate of interest of 7.34%, got traded at Rs. 1,030 on Friday i.e. a premium of 3% including one month’s accrued interest. This observation makes me believe that there is a scope of making some quick short-term listing gains with IRFC bonds as well.

Application Form for IRFC Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IRFC tax-free bonds, you can contact me at +919811797407

Thanks for the information!

Hi Shiv,

I invested in both NTPC and IREDA and was allotted some share of my Applied number of bonds. But when these bonds are listed in my Demat Account, it is showing a NAV of zero (0) whereas for bonds like NHAI etc. it is showing values like 1029/1030 etc. All the bonds are issued in 2015-16. Can you let me know if there is any discrepancy? and if yes, whether it is from Bank end or NTPC/IREDA end.

Thanks,

Amit

I want to understand on the liquidity part of these tax free bonds.

IRFC is offering 10 years – 7.29% p.a. & 15 years – 7.64% p.a.

My concern is that though this is beneficial for me being in the 30% income bracket but otherwise the returns are too low . What if i want to sell them after 3-4 years if i get a better opportunity due to increase in interest rate cycle or due to other opportunities. Is there any liquidity risk because i can hardly see any buyer or seller on the exchanges in retail category.

NABARD Tax-Free Bonds Issue Update:

Issue opens – 9th March, 2016, Issue closes – 16th March, 2016, Issue Size – Rs. 3,500 crore

Interest Rates for Retail Individual Investors investing upto Rs. 10 lacs:

10 years – 7.29% p.a.

15 years – 7.64% p.a.

HUDCO Tranche II update:

Issue opens – 2nd March, 2016, Issue closes – 10th March, 2016

Interest Rates for Retail Individual Investors investing upto Rs. 10 lacs:

10 years – 7.29% p.a.

15 years – 7.69% p.a.

Total Issue Size – Rs. 1,788.50 crore, including Green-Shoe Option to retain Rs. 1,288.50 crore

Shiv, Is IRFC also coming out with bonds in March ?

Yes Raj, IRFC will be launching its second issue of tax-free bonds in March.

NHAI Tranche II update:

Issue opens – 24th February, 2016

Issue closes – 1st March, 2016

Interest Rates for Retail Individual Investors investing upto Rs. 10 lacs:

10 years – 7.29% p.a.

15 years – 7.69% p.a.

Total Issue Size – Rs. 3,300 crore, including Green-Shoe Option to retain Rs. 2,800 crore

IRFC will raise an additional Rs. 3,500 crore by issuing tax-free bonds this financial year – http://www.financialexpress.com/article/economy/indian-railway-finance-corporation-gets-rs-3500-crore-more-tax-free-bond-limit/211014/

HUDCO 7.64% Tax-Free Bonds Review – http://www.onemint.com/2016/01/21/hudco-7-64-tax-free-bonds-tranche-i-january-2016-issue/

HUDCO tax-free bonds issue update:

Issue opens – 27th January

Issue closes – 10th February

Base Issue Size – Rs. 500 crore

Total Issue Size – Rs. 1,711.50 crore

Interest Rates for Retail Individual investors investing upto Rs. 10 lacs:

10 years – 7.27% p.a.

15 years – 7.64% p.a.

IREDA 7.74% Tax-Free Bonds Issue – http://www.onemint.com/2016/01/02/ireda-7-74-tax-free-bonds-january-2016-issue/

Hi Shiv,

I regard you as an expert in Bond Market.

You had following expectations from IRFC.

“Listing Gains – IRFC is offering 7.53% rate of interest for its 15-year option, which is also the highest rate of interest for its bonds across all three options. NTPC issue also carried the same 7.53% rate of interest for its 15-year option. As you can check from the table above, NTPC 15-year bonds last traded at Rs. 1,047 on Friday on the NSE i.e. a 4.7% premium to its issue price. Even if I consider Rs. 12-15 premium to be the accrued interest for the 2-month period since listing, these bonds are still earning a natural premium of approximately 3-3.50%.”

Now, Actual Listing must hav surprised you, like most ppl.

How would you understand this ??

Where this Natural Premium vanished away ??

Asking, just to understand this Bond market in a better way.

it is because 760 nhai 30 was available to invest in the mean time. moreover the interest being paid was more

look at the above mentioned comment of jason. you will get the answer.

Hi Rohit,

NTPC 7.53% bonds today last traded at Rs. 1,036 with only 32 bonds traded on the NSE. Please check this link – http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NTPC&series=NC

This shows the yield of these bonds has gone up and demand has also decreased in the last 20-25 days. Pricing is a matter of demand & supply and alternate opportunities elsewhere. With IRFC bonds, demand is low at its current yield as investors are getting higher coupon with NHAI and people who invested for listing gains are ready to sell even at their cost. Moreover, bad political scenario with GST not getting passed in the Winter session of Parliament also had its negative side effects on the bond yields. But, I think we should have a gradual recovery going forward.

Good analysis Shiv. You have summed it up very well. Markets are vulnerable due to micro and Macro economic reasons. But still the TFB are a good bet considering tax free coupon assured at reasonable rates. Definitely current issues are not going to help those who are looking for quick bucks soon after listing. I sold few of my NTPC bonds for 1065 after listing, I had opportunity to sell it at 1075 later but still retained remaining. At the end of the day investor goal defines his intent.