This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

It seems like the hunger for tax-free bonds is just growing unabated and whatever the issue size be it would be gobbled up by the investors on the first day itself. HUDCO will launch its second issue of tax-free bonds from 2nd of March i.e. the coming Wednesday and though the company has fixed March 10 to be the closing date of this issue, I think there is no need to emphasize here on this forum that nobody should expect to get any allotment if the bid is not made on the first day itself.

It will be the ninth such issue of tax-free bonds for the current financial year, but none of the issues has lasted for more than one day to get oversubscribed, except for the NHAI Tranche I in December. Though I think for any issue to last for more than one day the quota for the retail investors has to be more than Rs. 2,000-2,500 crore, this issue has only Rs. 715 crore for the individual investors investing Rs. 10 lakhs or less.

Here are the main features of HUDCO Tax-Free Bonds Tranche II:

Size of the Issue – Out of Rs. 5,000 crore allocated to HUDCO to be raised this financial year, 70% i.e. Rs. 3,500 crore should be raised through public issues. HUDCO raised Rs. 1,711.50 crore through its first public issue in January and it will raise the remaining Rs. 1,788.50 crore in this issue.

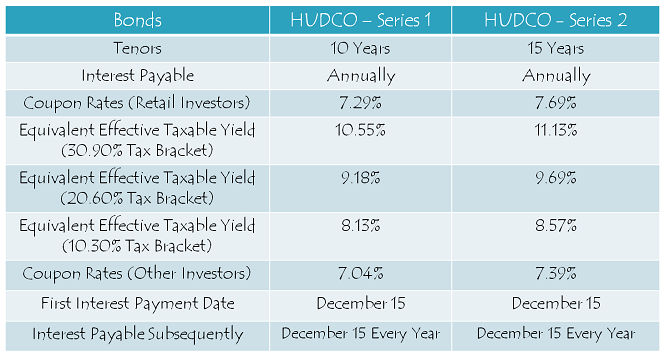

Coupon Rates on Offer – HUDCO issue will carry coupon rates which are absolutely same as offered by NHAI in its issue which got closed yesterday – 7.29% for the 10-year option and 7.69% for the 15-year option. Like the NHAI issue, this issue also will not offer the 20-year option.

For the non-retail investors, coupon rate will be lower by 25 basis points (or 0.25%) for the 10-year option and 30 basis points (or 0.30%) for the 15-year option, as it was the case in the NHAI issue as well.

Rating of the Issue – CARE and India Ratings have assigned ‘AAA’ rating to the issue, indicating that the issue is quite safe to invest and the company is highly likely to pay its debt obligations in a timely manner. Also, these bonds are ‘Secured’ in nature and in case of any default, the bondholders would carry a right to make claim on certain assets of the company.

NRI/QFI Investment Not Allowed – Again, Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 20% of the issue is reserved i.e. Rs. 357.70 crore

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved i.e. Rs. 357.70 crore

Category III – High Net Worth Individuals including HUFs – 20% of the issue is reserved i.e. Rs. 357.70 crore

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved i.e. Rs. 715.40 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first-come-first-served (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing & Allotment – HUDCO bonds will get listed only on the Bombay Stock Exchange (BSE). The company will allot the bonds and get them listed within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – It is not mandatory to have a demat account to apply for these bonds. Investors have the option to subscribe to these bonds in physical form as well. Whether you apply for these bonds in demat or physical form, the interest payment will still be credited to your bank account through ECS.

Also, even if you get these bonds allotted in an electronic form, you have the option to rematerialize your holding in physical/certificate form if you decide to close your demat account in future.

No Lock-In Period – These tax-free bonds are freely tradable and do not carry any lock-in period. The investors may sell them at the market price whenever they want after these bonds get listed on the stock exchanges within 12 working days of the closing date.

Interest on Application Money & Refund – Successful allottees will earn interest at the applicable coupon rates on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of face value Rs. 1,000 each. There is no upper limit for the investors to invest in this issue. However, an investor investing more than Rs. 10 lakhs will be categorized as a high networth individual (HNI) and will get a lower rate of interest as applicable.

Interest Payment Date – HUDCO will make its first interest payment on December 15 this year and subsequent interest payments will also be made on December 15 every year, except the last interest payment, which will be made to the bondholders along with the redemption amount on the maturity date.

Record Date – For the payment of interest or the maturity amount, record date will be fixed 15 days prior to the date on which such amount is due to be payable.

Should you invest in this issue?

Budget 2016 will be presented in the parliament on February 29 and we will get to know whether we will have these tax-free bonds available or not for the next financial year. In case the finance minister Mr. Arun Jaitley decides against extending this facility to these public sector units, then I think there will be a rise in the demand for the already listed tax-free bonds and hence, we can expect a rise in their market value as well.

Also, a higher fiscal deficit number will result in an increase in bond yields, which in turn will result in a higher coupon rates for the IRFC and NABARD issues. So, in case there is a jump in bond yields, then you should wait for the these two issues to decide on your final investments. I’ll update this post on March 1 after the climax of Budget 2016 gets revealed.

Expected Launch Date of IRFC and NABARD Issues – 2nd week of March

Application Form for HUDCO Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in HUDCO tax-free bonds, you can contact me at +919811797407

Very good response is seen. Can the retail investors hope to get 50% allotment. I am happy that I did not wait for future TSBs. Also your advice in time helped to participate in NHAI.

I think retail category should get around 50-53% allotment.

Thank you, that is good news. Suddenly the demand has gone up.

I find the retail category 4 2000000 14018853 7.01 times. What does it mean?

It means the issue has got oversubscribed by 7.01 times on the base issue size of Rs. 200 crore for Category IV.

Very good response is een. Can the retail investors hope to get 50% allotment. I am happy that I did not wait for future TSBs. Also your advice in time helped to participate in NHAI.

i think full response is going on.

chances are very hard in retail to get 25 to 30 %..

let us wait and watch at 5 pm..closing figure.

As per ET, retail portion is subscribed about 2 times on day-1. So 50 % allotment can be expected in retail category.

Dear Shiv kukreja ji,

Is it possible to see subscribed values

live (real time) on some NSE, BSE Websites?

I would like to invest in retail ct.

awaiting your early reply

thanks

Hi PS,

Please check this link for Live subscription figures – http://www.bseindia.com/markets/publicIssues/BSEcumu_demand.aspx?ID=1069

As per a news item in Times of India (1.3.2016), Govt will not issue TFBs from next FY onwards.

Clarity is still awaited regarding that Vin, let’s see when the government clarifies about it.

Dear Mr. Shiv

Pl advise me whether it is advisable to invest in current HUDCO TFB or wait for RFC and NABARD TFBs or wait for next FY 2016-17.

A.K. Jain

Dwarka

Hi Mr. Jain,

We still don’t know whether tax-free bonds will be there next fiscal year or not. Moreover, the 10-year govt bond yield has fallen to 7.608% from 7.876% in the last three days. So, I think going forward there will be a fall in the coupon rates of these bonds and their demand will rise. Considering these two things, one should definitely invest in this issue. In all likelihood, you won’t get full allotment for these bonds. You can invest the refund amount in IRFC and NABARD issues.

Unless you have boatloads of ready cash, it may be difficult to invest in the other bonds. Correct me if I am wrong, but the refunds are expected in approx 12 days from the closing.

I am following a different (risky) strategy..don’t know if it will work. Let the oversubscription play out for HUDCO and then hit NABARD. A 5-10 bps reduction in interest rate would not matter as long as one gets a higher percentage of allocation since it averages out on the higher allocation.

Hi nn,

Considering 50%+ allotment, I would have applied for the HUDCO bonds as I think refund would be available for at least one of the next two issues. But, if a lower rate of interest is not an issue, then probably one should wait for the next issue.

Expecting both of them to launch approx 9/10 with a max 5bps cut.

Let us hope i an wrong on the dates..

Expecting both of them to launch approx 9/10 with a max 5bps cut.

Let us hope i am wrong on the dates..

Dear Mr. Shiv Kukreja,

Please inform where exactly & how precisely are TFB’s sale STCG/STCL are to be shown in I.T.R. Form while filing tax returns.

Please explain Taxation on STCG (less than 1 year of holding) & LTCG (after 1 year of holding).

Hi S.K.,

LTCG on these bonds is taxed @ 10% (flat) and STCG is taxed as per your tax slab. Moreover, please consult your tax advisor for ITR treatment of these bonds.

nabard credit ratings please

NABARD issue would be rated ‘AAA’.

Very informative

Thanks Paulose!

I don’t hv deemat acount. Still I can purchase tax free bonds..pl help..

how can I. .

thanku.

Hi Anoop,

Please mail me your requirements on skukreja@investitude.co.in, I’ll try to help you buy these bonds from an interested seller.

Thanku sir..for helping me

I placed a bid on 10 am through hdfc security. May I lucky 1.?..

Hi Anoop,

You should get proportionate allotment.

I want to purchase current or old tax free

bonds..can u help me to get..

Shiv

Can you confirm hudco are available on “certificate” basis. It may be a good idea to purchase for some family members.

Yes nn, you can apply for these bonds in physical/certificate form.

Is it good idea to wait for IRFC and NABARD and will have better coupon or no point in waiting and they might have low coupon

Hi Vinod,

After a lower than expected fiscal deficit target of 3.5% announced in today’s budget, 10-year banchmark bond yield has fallen sharply to 7.626% from 7.783% on Friday. If IRFC & NABARD issues get delayed by 5-7 days, then I think they would carry a lower rate of interest than this issue.

Thanks Shiv

You are welcome Vinod!

What time in the morning of 2nd March does the issue open up for subscription ?

Hi Mr. Joshi,

Bidding will start at 10 a.m. in the morning.

POST BUDGET – whether we will have these tax-free bonds available or not for the next financial year. ??

THANKS

I think it will be there. Some 33kcrore. Sir , can you please confirm

I had Mr. Jetali’s Budget Speech in Loksabha on 29.2.2016. He clearly said there won’t be TFBs for the next year.

I heard Mr. Jetali’s Budget Speech in Loksabha on 29.2.2016. He clearly said there won’t be TFBs for the next year.

Dear Shiv,

Is there any announcement for new Tax free bonds for the financial year 2016 & 17 ?

Hi Nishar,

There is no clear announcement about tax-free bonds in the Budget. But, there are two statements in the Budget speech which indicate that these bonds have been allowed to get launched:

1. “To augment infrastructure spending further, Government will permit mobilisation of additional finances to the extent of `31,300 crore by NHAI, PFC, REC, IREDA, NABARD and Inland Water Authority through raising of Bonds during 2016-17”.

2. “This will be further topped up by additional Rs. 15,000 crore to be raised by NHAI through bonds”.

Thanks a lot . If any clarity after few days pls do let us know…

Sir,

If I am sell Tax free Bonds after 02 years from the date of Allotment ,Thus Long term capital gain tax is apply for Capital Appreciation or not..If Ltcg Apply ,what is the tax rate..

Sir,

If I am sell Tax free bonds after 02 years of Allotment date..thus Long term capital gain Tax apply for the Capital Appreciation or not..If Apply What is the Tax rate..

Hi Madhu,

LTCG tax for listed bonds is 10% (flat).

Dear Mr. Shiv,

In case TFB’s are in DEMAT joint names, & first holder passes away, to whom will the Bond holdings pass on to? Will it be to the 2nd Joint holder in the Demat Account or to the Registered Nominee in the Account? Will submitting the death certificate be adequate for the transmission of all Demat Holdings? Please clarify in some detail & oblige?

Thank you.

Dear Mr.Shiv,

Is there any announcement for Tax Free bonds by Finance Minister for the Financial year 2016 and 17?

Hi S.K.,

In case the first holder passes away, the 2nd holder will become the only beneficial owner of these bonds. A fresh demat account in the name of the 2nd holder will have to be opened and a death certificate will have to be deposited along with the transmission form to get the holdings transferred.

Dear Mr. Shiv Kukreja,

Is only death certificate adequate in above case. I happen to read ICICI’s transmission form online, where lots of other documentation like succession certificate, letter of administration etc are indicated. I am somewhat confused why so many unnecessary requirements. Could you please clarify in detail .

Hi S.K.,

Different documentation is required for different situations. Please get in touch with ICICI Direct people to have a checklist as per your situation.

1- In case of the death of First holder the death certificate is sufficient, no other documentation is required for second holder. It may require a change in Demat Account Number from the

2-ICICI Securities has given you a common form. You should delete the inapplicable caluses and submit.

Hi Shiv,

Looking at the size of issue, this issue will also oversubscribe on the first day isn’t it?

Regards,

CVS

Yes CVS, most likely this issue will also get oversubscribed on the first day itself.

saving ideas. com is showing 15th dec every year of payment of interest for this bonds actual interest payments date please shiv

Thanks Nitesh for pointing it out, I have corrected it above in the post.

Thanks for this info … KS

You are welcome KS!