This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

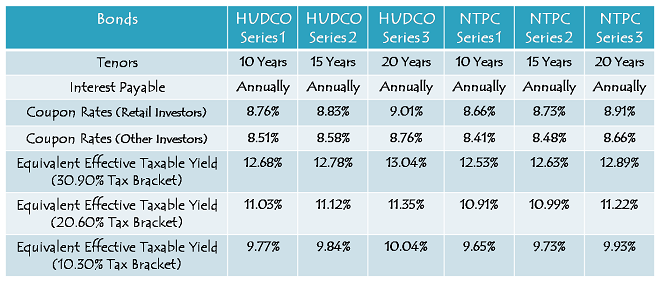

After a month long break, tax free bond issues are back and the 10-year options are looking much healthier now carrying annual coupon rates of 8.76% and 8.66% for ‘AA+’ rated HUDCO issue and ‘AAA’ rated NTPC issue respectively, as against its previous highs of 8.43% for ‘AAA’ rated PFC & NHPC issues and 8.39% for ‘AA+’ rated HUDCO issue.

While this jump has come due to a consistent rise in the yield of the benchmark 7.16% 10-year government bond, the coupon rates with 15-year option and 20-year option have been the highest ever with the HUDCO issue as it is rated ‘AA+’ and carries a leverage of 10 basis points (or 0.10% per annum). I’ll cover the HUDCO issue today and the NTPC issue tomorrow.

HUDCO is launching the second tranche of its tax free bonds from Monday, December 2nd and it will be the first ever tax free bond issue to cross the psychological mark of 9% coupon rate.

Size of the Issue – HUDCO has set the base issue size at Rs. 500 crore with an option to retain oversubscription up to Rs. 2,439.20 crore. The company has already raised Rs. 2,560.80 crore in its first tranche and through a private placement. I think this issue is attractive enough for it to become the last issue from HUDCO’s stable.

Rating of the Issue – Like Tranche I, this issue has also been rated ‘AA+’. CARE and India Ratings are the two companies which have passed their opinion to assign this rating to the current issue.

Again, the bonds are ‘Secured’ in nature as certain receivables of the company will be charged to the extent of amount to be mobilized under the issue. Also, as HUDCO is wholly-owned by the government of India, I would consider the investors’ investments to be comfortably safe in the issue.

OK to NRI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible.

Investor Categories & Allocation Ratio – As always, the investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved for the allocation:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 30% of the issue is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue is reserved

First Come First Served Allotment – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing – Bombay Stock Exchange (BSE) is the only exchange on which these bonds will get listed and the exchange has given its in-principle listing approval to the bonds issued under this tranche. As with all the recent issues, these bonds also will get allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Investors can apply for these bonds either in physical form or in demat form, as per their comfort and requirement.

No Lock-In Period – These bonds are offering good rate of interest which is tax-free also under Indian taxation laws. As your investment does not provide any tax deduction, there isn’t any lock-in period with these bonds. As these bonds get listed on the BSE, you may sell them whenever you want at the market price.

Interest on Application Money & Refund – HUDCO is the only company which pays the same rate of interest as the applicable coupon rate is on the application money as well as on the money due for a refund. So, with the 20-year option, you’ll get 9.01% as the rate of interest on your application money as well as the refund amount.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest Payment Date – HUDCO has not announced the interest payment date of this issue as yet. I will update this post as and when it gets announced at the time of listing.

While it will be a bonanza for the fixed income investors, I’ll consider this to be a bad situation for the commercial banks, the government and the borrowers. Let’s check how.

Many people have been breaking their fixed deposits to invest in these tax free bonds. It is putting a lot of pressure on the banks to either hike their deposit rates or increase premature withdrawal charges.

As the money is moving out of taxable instruments like fixed deposits, post office schemes etc., the government is also losing out a big amount in tax revenues.

Higher rate of interest will force banks to hike their lending rates also in order to maintain their net interest margins (NIMs) and this outcome will put an additional burden on the borrowers.

With a huge difference between the 10-year interest rate and the 20-year or 15-year rates, I used to prefer the 20-year or 15-year options earlier. But, as the difference has narrowed down considerably, the 10-year option has also become quite attractive now. However, I still prefer the longer duration options as I think it is better to stay invested with longer duration bonds when the interest rates get higher.

Though the issue is scheduled to get closed on January 10, 2014, I really doubt that it would continue that long. I expect it to get closed earlier than that given other companies don’t offer a similar or higher rate of interest.

With coupon rate crossing 9% now on these tax free bonds, there is no reason for the investors to ignore such high rate of interest and keep investing their fresh money into fixed deposits or keep their money invested in it.

Application Form of HUDCO Tax Free Bonds

HUDCO Tax-Free Bonds – Bidding Centres

HUDCO Tax Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in HUDCO tax-free bonds, you can contact me at +919811797407

Day 12 (December 17) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 342.63 crore as against Rs. 487.84 crore reserved

Category III – Rs. 526.79 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,121.26 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,037.71 crore as against total issue size of Rs. 2,439.20 crore

Day 11 (December 16) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 342.13 crore as against Rs. 487.84 crore reserved

Category III – Rs. 521.01 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,107.33 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,017.51 crore as against total issue size of Rs. 2,439.20 crore

today’s subscription numbers ?

Hi Shiv

I am not sure this is the time to ask you.

I want to know is there any Tax Free Bonds coming in the month between May 2014 to August 2014.

Hi Paresh,

As of now, it is not possible for anybody to tell you anything about it. The quantum of tax-free bond issues get announced only in Budget every year. Next year there is no certainty that these bonds would get issued or not.

Day 10 (December 13) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 338.58 crore as against Rs. 487.84 crore reserved

Category III – Rs. 508.86 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,083.12 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,977.59 crore as against total issue size of Rs. 2,439.20 crore

Day 9 (December 12) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 330.08 crore as against Rs. 487.84 crore reserved

Category III – Rs. 504.25 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,064.30 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,945.67 crore as against total issue size of Rs. 2,439.20 crore

Please advise why there is difference in your subscription figures vs bse website figures like in cat III bse website shows 3.24 times subscription whereas above figures are different.

3.24 times is as per the base issue size of Rs. 150 crore applicable to Category III.

Hi Shiv,

Nov CPI data is 11.24 percent – do you think that RBI governor would still “surprise” markets by keeping status quo on repo rate? Thanks

No, not now. CPI Inflation is on a higher side and deeply disappointing. 25 basis points Repo Rate hike is a done deal now. If Dr. Rajan does not hike it, then it would be difficult for us to understand his reasons behind it. This again puts the government in an extremely difficult position now. Its a wake up call for Mr. Chidambaram !!

Hi Shiv,

So higher coupon rates in the offering – for forthcoming bonds ?

Yes, it seems so.

Hi Shiv,

Any news at all on IRFC\NHAI\NHB ? Possibly higher g-sec yields now makes these issues interesting with higher coupon rates possible as you stated

Hi Aditya,

I’ve been told that IRFC is getting ready to launch its issue anytime on or after December 23rd. NHB has also filed its Draft Shelf Prospectus on December 13th, so you can expect its issue to hit in the last week of December or 1st week of January.

Thanks Shiv – useful info

Hi Shiv,

Is it possible to check allotment status for a physical application for hudco bonds? If so, pls could you advise how and when it can be tracked? Thanks in advance.

Hi Jayaram,

You can check the allotment status from the below pasted link after the bonds get allotted:

http://mis.karvycomputershare.com/ipo/

Day 8 (December 11) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 328.77 crore as against Rs. 487.84 crore reserved

Category III – Rs. 494.95 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,039.73 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,910.48 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv,

Do you expect RBI to hike repo rate this time and if it does will the coupon for future bonds increase?

Hi Jay,

Personally, I think Dr. Rajan would like to surprise the markets by not raising the Repo Rate this time. But, if the Repo Rate gets increased, then I think G-Sec yields will rise and future coupon rates would get fixed higher.

I also think Raghuram Rajan (who incidentally also happens to be my classmate) likes to surprise the markets and he may not change the rates contrary to the 25 bps hike that the market is expecting.

That is great to know Mr. Ram Mohan !! So, if we want to meet Dr. Rajan some day, I hope we can always contact you ??

Also, even I would like Dr. Rajan to give Repo Rate hike a miss this time and give growth a chance to revive. In fact, it is the government’s duty to take steps to control inflation.

Mr. Ram Mohan, your classmate has actually left the markets pleasantly surprised. 🙂

Yes he has Shiv. Even when he was the CEA before becoming the RBI Guv, ie when he was on the other side of the fence, so to speak, and voicing views of the Finance Ministry, he used to say that the RBI needs to surprise the markets at least once in a while. This would put all the speculators on guard. Raghuram Rajan has been a good event for the markets ever since he took over in September. Since then on, his exemplary achievement has been to bring the Rupee back to stability and that singular achievement has brought in confidence in the markets especially for the overseas markets, who were worried whether they would earn far less when the time actually comes to withdraw the money. His other achievement has been to reverse the inverted yield curve. When he took over the short term debt yields were higher than long term yields, a sure recipe for economy stagnation. Now the yield curve has straightened and that is good.

Yes, you are absolutely right! He has been smarter and fortunate also. He has been successfully able to reverse the measures taken by the RBI earlier and correct the yield curve.

But, at the same time, I would fully support the ex-Governor of RBI, Dr. Subbarao. Whatever he did, it was done under finance ministry’s undue pressure. I think the rupee got stabilized due to deferment of QE tapering and improvement in the market sentiment.

Whatever wrong is there in the economy, it is due to the government’s incorrect policies and unreasonable arrogance.

Hi Shiv,

Excellent coverage and you do take pains to respond to each and every query.

I have also subscribed to hudco bonds under retail category. The advantage with this issue is that the interest rate is very high and it is unlikely that any other issue will be offering this high an interest, at least in the near future. And as the interest rates start falling in the future, one can get handsome listing gains. However, the disadvantage with this issue, as with other tax free bonds is the virtual absence of liquidity in the secondary market. Some bonds such as NHAI get traded frequently, while most other do not get that heavily traded. However, looking at the size of this issue, I am hopeful that there is a good liquidity when the bonds get listed on the BSE. My suggestion is that the financial intermediaries should trade in these bonds more frequently so as to provide the desired liquidity to the small investors.

Ram Mohan

Thanks Mr. Ram Mohan for your inputs !!

There are many factors which affect liquidity for a specific issue and you are right NHAI has liquidity which is good enough for a bond. I too hope this issue will have a better liquidity than the previous issue by HUDCO.

Financial intermediaries don’t find any profitable opportunities in trading unnecessarily in the bond market. That is why they don’t do that.

Thanks Shiv for your comments. I have actually made a model for calculating the effect of yields on the capital values of long term bonds. The longer the tenure the greater is the impact due to changes in yields. For instance, for a 20 year bond, which is the longest available now, a 1% change in yield affects the price by 10%. This provides the greatest leverage. Naturally, the leverage decreases with decrease in tenure. Thus, with the HUDCO bond which is available at 9% yield, the price would increase by 10% if the yield goes down to 8%. This change in yield may not happen overnight, but even if it happens over a 2 year period, this effectively translates into a capital appreciation of 10% over 2 years, or 5% per year. This is in addition to the 9% interest that one gets from the bonds, which means one can get a 14% virtually risk-free return per year. And one can exit after the 2 years.

Hi Mr. Ram Mohan,

Your model is called the duration effect. The higher the duration (volatility), the higher is the change in the bond prices. I am sure 1% fall in the YTM (yield) of a 20-year tax-free bond would result in a more than 5-10% increase in its prices.

Hi Shiv

I have one question for HUDCO 9.01 % Bond. On day 7 [ Dec 10 ] Category II – Rs. 321.13 crore as against 487.84 crore.

So now if apply on day 8 [ Dec 11 ] and category II is not fully subscribed up to 487.84 crore there are chances of full allotment what i apply.

What i understand is that in Category II i can apply up to the day it fully subscribe up to 487.84 crore and in that case i will get the full allotment what I apply.

Please explain me. Because i am gettimg some fund on 13 th December.

That is correct Paresh. If you apply for it today and if it does not get oversubscribed by 5 p.m., you’ll get full allotment.

Hi Shiv

That doesn’t sound right to me. First come first serve basis is applicable to respective category in my view. If a Cat II investor applies for their quota any day before HUDCO decides to close the offer so long they have the limit availability they should get their allotment. How can a Cat 4 investor who’s applying over their reserved limit get an allotment from Cat 2 reserved limit in such a case?

Hi Subbu,

Paresh wants to apply in Category II itself (not in Category IV) and you are absolutely right that each category is going to get its own allocation. If Category II remains unsubscribed, then whatever portion remains unsubscribed will go to the Category IV investors first.

Day 7 (December 10) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 312.13 crore as against Rs. 487.84 crore reserved

Category III – Rs. 485.05 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,004.64 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,848.85 crore as against total issue size of Rs. 2,439.20 crore

Seems that HUDCO is oversubscribed now in the Retail category

That’s correct, it has got oversubscribed in the retail category.

Hi,

By saying “Category IV should get oversubscribed tomorrow.” , is that I cannot invest in this Bond after its over subscribed ?

Thanks & Regards

Devan.

It is not like that Devan. You can very well invest in Category IV even after it gets oversubscribed. But, as it is on a “first come first served” basis, there is no guarantee of allotment if you invest after its over-subscription.

Day 6 (December 9) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 301.97 crore as against Rs. 487.84 crore reserved

Category III – Rs. 464.52 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 934.37 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,747.89 crore as against total issue size of Rs. 2,439.20 crore

Category IV should get oversubscribed tomorrow.

Dear Mr Shiv

Thanks for your quick response. By allotment status I meant a website where I could feed my application number and demat details & know if indeed I have got full allotment.

As of now it is not possible. It will be declared only once the Basis of Allotment gets finalised.

You’ll get to check it on this link: http://mis.karvycomputershare.com/ipo/#

Dear Mr. Shiv

I have applied online today under category IV ( <10 lakhs). I believe that I will get full allotment. Kindly advise on subscription figures for today Day 6. Kindly also advise as to how to check allotment status online and when would the allotment take place.

Many thanks for your support and co-operation.

Hi NKN,

Though it is quite close to getting fully subscribed in the retail investors’ category, it doesn’t look like that it will get fully subscribed today itself. I think you’ll get the full allotment.

Hi Shiv,

Will HUDCO wait for all categories to get subscribed fully ? Or they might call an early close to the issue ? considering this is tranche 2 of their bond issue and those who have already invested in Tranche 1 may not be interested here.

Hi Aditya,

As the retail investor category (Category IV) is already close to getting fully subscribed, HUDCO will now wait for only the issue to get fully subscribed and not each category. As soon as the subscription figures cross Rs. 2,439.20 crore mark or reach very close to it, HUDCO should decide to close the issue the very next day.

Here is the link to check the allotment status:

http://www.bseindia.com/markets/publicIssues/BSEcumu_demand.aspx?ID=740

Allotment will take place within 12 working days from the issue closing date. If the issue gets closed on say 18th December, you’ll get allotment within 12 working days from December 18th.

Day 5 (December 6) subscription figures:

Category I – Rs. 22.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 288.48 crore as against Rs. 487.84 crore reserved

Category III – Rs. 341.81 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 770.70 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,423.03 crore as against total issue size of Rs. 2,439.20 crore

Category IV should get oversubscribed in a couple of days time.

You have not posted Day 5 (December 6) subscription figures.

When will PGCIL fix the price? How many shares can I get for 2L application if issue is subscribed 2.17 time? I will get 6 lots minimum- how much more?

Thanks Vivek for reminding me !! I’ll do it right away. I was under the impression that I did that yesterday.

Basis of Allotment system has been changed for the IPOs/FPOs Vivek. Though I analysed it last year, I don’t remember how exactly it works. But, one thing is for sure – every valid application will get at least one lot of 150 shares allotted. I am working on a post with many such queries about Power Grid FPO.

Dear Shiv,

I heard that Tata Sons is going to come out with 300 Crore debt issue soon – do you have any update if NRI’s can invest and if there will be cumulative option?

Dear Jayaram,

Most of these deals happen through private placement. So, general public cannot participate in these issues.