This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

As the NHAI issue opens today, many investors have not been able to decide which issue they should go for – NHAI 8.75%, 8.52% or IRFC 8.65%, 8.48%. This comparison also becomes significant as no other company has even filed the draft prospectus for its issue. Before I do the comparative analysis, let’s check once again why these tax free bonds have become so popular with the investors.

Investors’ response to the tax-free bonds this financial year has been quite better as compared to the last financial year. The reasons are simple:

Higher Rate of Interest – Last year, these tax-free bonds were carrying lower rate of interest rates, broadly in the range of 7-8%. This year, their interest rates have been higher by around 1%. At the same time, interest rates on other saving instruments, like bank fixed deposits (FDs), post office schemes, company FDs etc., are more or less stable or just slightly higher.

Thanks to the higher G-Sec rates, it is natural for the investors to opt for 9.01% tax free bonds from the National Housing Bank (NHB) as against 9% fixed deposit interest rates from the State Bank of India (SBI) or from some other banks.

Removal of “Step Down” Clause – Till last year, these bonds carried the “Step Down” clause, as per which the buyer(s) of these bonds from the secondary markets are entitled to a lower rate of interest as compared to the first allottees. This is not applicable with the bonds issued during the current financial year.

This is also the reason why the bonds issued last year attract a very low trading interest, which I think should not be the case with this year’s tax free bonds going forward.

Lower Rate Differential – Differential between the rates offered to the retail investors and the non-retail investors got fixed at 0.25% per annum this year, which stood at 0.50% till last year. Non-retail investors considered it to be on a higher side and their participation was quite limited last year. This year, non-retail investors’ participation has been considerably better, especially with NHPC, NTPC and NHB.

Losses in Gilt/Income Funds – Bloodbath in the debt markets or a steep fall in the NAVs of debt mutual funds, due to some incorrect policy measures by the government and the RBI and also QE3 tapering announcement by the US Fed, also led to a shift in the investors’ interest towards these tax free bonds.

Investors of these tax free bonds know that they are going to get at least some fixed interest income every year in their bank accounts, even if there is no capital appreciation or even if the interest rates move higher from the current levels, resulting in a notional capital loss.

So, with very few options left available for the current financial year, the investors at present are asking themselves:

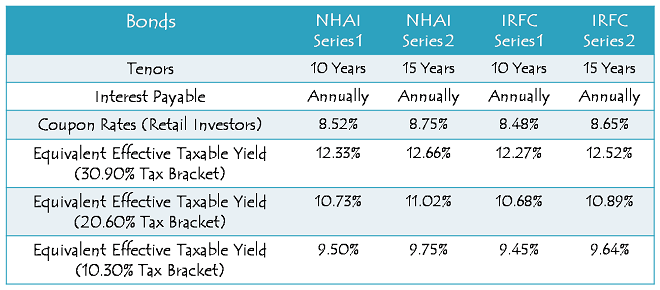

NHAI 8.75% or 8.52% vs. IRFC 8.65% or 8.48% – which issue should I invest in?

In terms of interest rates, it is very much clear that NHAI is offering higher rate of interest than IRFC, so it is relatively better. But, is it that simple? Certainly not, at least not for a common investor. How are these two companies different and which company is fundamentally better? Let us try to do some analysis.

Though not strictly comparable, I’ve tried to do a comparison between IRFC and NHAI on certain parameters. While IRFC is the wholly-owned financial arm of Indian Railways, NHAI is an autonomous body of the Government of India. Both these companies are strategically important for the Government of India (GoI).

IRFC got constituted in December 1986 for the purpose of raising the necessary resources for meeting the developmental needs of the Indian Railways. NHAI got operationalised in February 1995 for the development, maintenance and management of India’s national highways.

While IRFC has been classified as the Infrastructure Finance Company (IFC) by the RBI, NHAI is the nodal agency for the development and maintenance of national highways across the country, which makes it an infrastructure developer itself.

Financial Position of IRFC and NHAI

IRFC has a net worth of Rs. 5,794.28 crore as on March 30, 2013, whereas the same stands at Rs. 81,053.11 crore for the NHAI. As IRFC lends almost all its borrowings to the Indian Railways for financing rolling stocks, it has zero non-performing assets (NPAs).

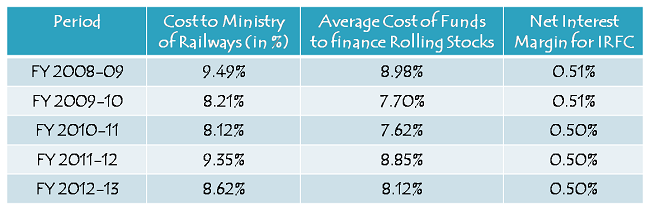

IRFC, on an annual basis, enters into a standard lease agreement with the MoR and earns an assured net interest margins from the MoR which has remained 0.50-0.51% in the last five fiscal years. MoR also bears the interest rate risk as well as the exchange rate risk. As it also gets regular capital infusion by the government of India, it got Rs. 600 crore during FY 2013.

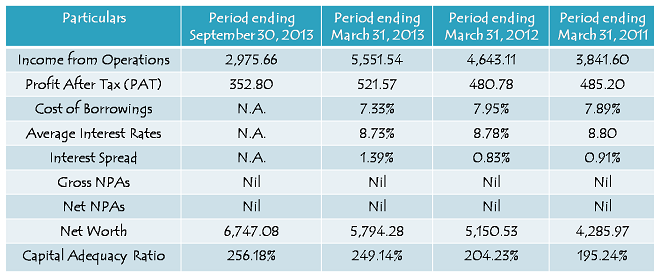

Also, here are certain financial numbers of IRFC over the past few years:

As NHAI has been running into operational losses for the last few years, it is not practical to analyse its profitability position and make a comparison with that of IRFC. But, NHAI is a bigger organisation and has a total capital employed at Rs. 1,13,331 crore and capital work in progress (CWIP) at Rs. 1,06,440 crore as on March 31, 2013.

NHAI has been mandated by the GoI to implement National Highway Development Project (NHDP) with an estimated investment of about Rs. 2.48 lakh crore, spread over seven phases. NHDP envisages improvement of approximately 54,500 kms of national highway network.

As it is very difficult to conclude which organisation is better between the two in terms of overall financial performance and operational efficiency, personally I think NHAI issue is a better one as it offers a higher rate of interest, the size of the organisation can be considered as too big to fail and its strategic importance in India’s road & highways development is too significant to ignore.

Which one do you think is better between the two and how long do you think the NHAI issue will last? Please share your views.