This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

After a reasonably good response to the REC tax-free bonds, the next eligible company to come up with such an issue is Housing and Urban Development Corporation Limited (HUDCO). The company will be launching its issue from the coming Tuesday, September 17.

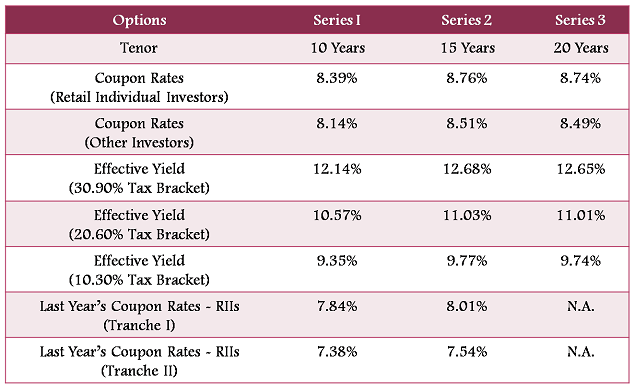

The rates the company is going to offer in this issue are higher than the rates offered by REC in its issue, which is still open and getting closed on September 16. There are two reasons for it, firstly, HUDCO issue is ‘AA+’ rated and that is why it can offer rates 10 basis points (or 0.10%) higher than any ‘AAA’ rated issuer. Secondly, the average G-Sec rates have been ranging higher in the past 10-20 days than they were earlier when REC came up with its issue.

As compared to REC’s 8.26% (10Y), 8.71% (15Y) and 8.62% (20Y), HUDCO is offering 8.39%, 8.76% and 8.74% rate of interest for the respective tenors.

Though the interest will be paid annually, I do not know the interest payment date as yet, as the final prospectus filed on September 11 is still not available on SEBI’s website, on BSE’s website, on HUDCO’s website and not even on any of the lead managers’ websites. It is quite disappointing for me not to have the prospectus available for public reference even three days prior to the issue opening date.

HUDCO is allowed to raise Rs. 5,000 crore from tax-free bonds this financial year, out of which it has already raised Rs. 190.80 crore through private placement. So, now it plans to raise the remaining Rs. 4,809.20 crore through this public issue, including the green-shoe option of Rs. 4,059.20 crore. The base issue size is Rs. 750 crore.

The official closing date of the issue is October 14 and the company may extend or preclose the issue, depending on the investors’ response to the issue.

There are many things which are common in this issue and the REC issue, so I will quickly state those features which are different in this issue.

Rating of the issue – CARE and India Ratings have assigned a rating of ‘AA+’ to this issue, which is also ‘Secured’ in nature. HUDCO is wholly-owned by the government of India, so the investors’ investment is quite safe.

Listing – HUDCO will get these bonds listed only on the Bombay Stock Exchange (BSE). The allotment and the listing will happen within 12 working days from the closing date of the issue. Investors can apply for these bonds either in physical form or in demat form, as per their comfort and requirement.

Interest on Application Money & Refund – The investors will get interest on their application money also, from the date of investment till the deemed date of allotment, at the same rate of interest as the applicable coupon rate is. Unlike REC issue which is to pay 5% p.a. interest on the refund money, HUDCO will pay the applicable coupon rate.

Categories of Investors & Basis of Allotment – The investors again have been classified in the following four categories and each category will have certain percentage of the issue reserved for the allotment:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 30% of the issue is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue is reserved

QIBs portion had 20% of the issue reserved in the REC issue and after observing their response in that issue, their reserved portion has been reduced to 10% in this issue. Category III HNI investors will get this 10% share of the pie. NRIs are eligible to invest in this issue as well, on a repatriation basis as well as on non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible.

Minimum & Maximum Investment – There is no change in the minimum investment requirement of Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest rates of this issue look very attractive to me. Earlier I used to say that the investors in the 30% or 20% tax bracket should consider these bonds, but now I advise investors even in the 10% tax bracket to go for these bonds. Though not strictly comparable, these bonds are attractive even against IIFL NCDs or Muthoot NCDs.

I think the way Indian rupee and the stock markets have recovered in the past 10 days or so, the G-Sec yields should also start falling soon. Going forward, I think the rates should not be higher than these HUDCO bonds, unless US Fed Reserve has something very dramatic in store for us in its meeting on September 17-18.

Link to Download the Application Form of HUDCO Tax-Free Bonds

If you need any further info or you want to invest in these bonds, you can contact me at +919811797407

Thanks Ramadas for your kind words!

IIFCL is expected to open for subscription in the 1st week of October and PFC is expected to open in the 2nd week. It is very difficult to guess the rates at this point of time, but it should be in the current range only, between 8.5% to 8.8%.

Thanks Shiv for the excellent article

Do you know when is IIFCL and PFC tax free bonds expected to hit the market?

What rates can be expected for 15 and 20 year tenures?

REC tax-free bonds to get listed on the stock exchanges on September 30th i.e. Monday.

Here are the BSE codes for the same:

8.26% 10-year bonds – BSE Code – 961778

8.71% 15-year bonds – BSE Code – 961779

8.62% 20-year bonds – BSE Code – 961780

How can i verify the subscription status?

Hi Phani… you can check this link & verify the status:

http://www.bseindia.com/markets/publicIssues/EODCumlativeShedule.aspx?ID=714

Day 8 (September 26) subscription figures:

Category I – Rs. 125.50 crore as against Rs. 480.92 crore reserved

Category II – Rs. 251.47 crore as against Rs. 961.84 crore reserved

Category III – Rs. 450.12 crore as against Rs. 1,442.76 crore reserved

Category IV – Rs. 834.15 crore as against Rs. 1,923.68 crore reserved

Total Subscription – Rs. 1,661.24 crore as against total issue size of Rs. 4,809.20 crore

Looks like subscription has slowed down.

Yes, your observation is correct.

Is the allotment based on 1st come 1st serve basis or any other procedure will be followed?

Hi Ravi… yes, it is “first-come-first-served” basis.

Day 7 (September 25) subscription figures:

Category I – Rs. 125.50 crore as against Rs. 480.92 crore reserved

Category II – Rs. 237.38 crore as against Rs. 961.84 crore reserved

Category III – Rs. 438.51 crore as against Rs. 1,442.76 crore reserved

Category IV – Rs. 783.71 crore as against Rs. 1,923.68 crore reserved

Total Subscription – Rs. 1,585.10 crore as against total issue size of Rs. 4,809.20 crore

Hi,

I want to know whether these tax free bonds can be bought both in physical form as well as in demat form? Is there any difference in these two with respect to the return i would get after completion of the investment tenure? In which form it would be preferable?

Hi Swagata,

Yes, you can buy these bonds in either of the forms – physical or demat. There is no difference with respect to the interest rates and you’ll get it annually paid into your bank account. If you intend to cash it out during your holding period or if you already have a demat account, then it is better to have it in a demat account. If you intend to hold it till maturity and if you do not have a demat account, then probably you should take it in physical form.

Hi Shiv,

How do we buy in Physical form? Where do we submit the application forms? Are there any banks/brokerage firms etc. who accept the application form? Can you please direct to any published info. on this?

Regards,

cvs77

Hi cvs77,

Sorry, I don’t have any published info on this, probably you can check the prospectus for the same. But, we (Ojas Capital), as a brokerage firm, help investors do it on a national level as we have physical presence only in Delhi/NCR. Here is the procedure to apply it in the physical form & the demat form as well:

* Download the physical form from the link pasted above in the article and duly fill it.

* Mail us the scanned copy of your duly filled form and we’ll do the bidding on the stock exchange, which is mandatory before banking the application form.

* We’ll tell you the BSE/NSE bidding code, which you’ll be required to manually write in front of the application form.

* After that you can either courier the form to us, along with your self-attested copies of PAN card, address proof and a cancelled cheque, or directly submit the form/docs at the designated bank branch nearest to your place. We’ll let you know the address of the designated bank branch nearest to your place.

I hope it helps! For any clarification or further info, you can contact me at +919811797407 or mail me at skukreja@investitude.co.in

Day 6 (September 24) subscription figures:

Category I – Rs. 75.50 crore as against Rs. 480.92 crore reserved

Category II – Rs. 231.59 crore as against Rs. 961.84 crore reserved

Category III – Rs. 427.88 crore as against Rs. 1,442.76 crore reserved

Category IV – Rs. 727.40 crore as against Rs. 1,923.68 crore reserved

Total Subscription – Rs. 1,462.36 crore as against total issue size of Rs. 4,809.20 crore

10 year g-sec yield is above 8.8% for last two days and there are talks of repo rate being increased again in october policy. So can we expect higher coupon rate in upcoming bonds?

What is the reference for 15 year bonds, as I see usually it carries highest coupon rate.

Hi Shashwat,

One more Repo Rate hike is already factored in the current bond yields. Yields are spiking due to high fiscal deficit expectations and high inflationary expectations. The way yields have spiked up in the last 2-3 days, it looks like the yields are not going to fall in a hurry. As of today, I think upcoming bonds should offer similar or lower rates than HUDCO bonds, but next 4-5 trading days are crucial for the rates to get determined.

Average of 15-year bond yield should be around 9.16% for the rates to get fixed at around 8.76%.

Hi Shashwat/Shiv

How do you’ll check YTM for benchmark 10 yr Gsec?

I’ve used nse trade data and did YTM calculation – but its tedious – is there an online resource?

Thanks

http://www.bloomberg.com/quote/GIND10YR:IND

Thank you for the useful information you present in this site.

Do you have the latest subscription status figures from today?

Do you expect this bond to fully subscribe and close much early as REC did?

Hi Subbu,

As of today, I don’t see this issue closing before its official closing date of October 14th.

Day 5 (September 23) subscription figures:

Category I – Rs. 70.50 crore as against Rs. 480.92 crore reserved

Category II – Rs. 221.51 crore as against Rs. 961.84 crore reserved

Category III – Rs. 376.32 crore as against Rs. 1,442.76 crore reserved

Category IV – Rs. 641.53 crore as against Rs. 1,923.68 crore reserved

Total Subscription – Rs. 1,309.85 crore as against total issue size of Rs. 4,809.20 crore

I am in mood of investing in HUDCO Tax Free Bonds. But I am scared of any losses in the market. Please suggest me whether these are as safe as Bank FDs or not. I don’t want any risk. Moreover, if being a Government company there is no risk, why ratings are different for REC and HUDCO. In case of any untoward incident with REC or HUDCO, will Government compensate them? In my understanding, Tax free bonds are those where principle amount shall be refunded by the company on maturity and interest shall continue to be paid at regular annual intervals. Please clarify…

Hi Anurag,

There is no way I can measure whether these bonds are more safe than the Bank FDs or less safe. Bank FDs are insured to the extent of Rs. 1 lac, whereas these bonds are not. But, at the same time, these companies are PSUs and quite big & favoured PSUs, Navratnas & Mini-Ratnas of India. One of these companies is National Housing Bank (NHB), which is also the regulator of housing finance companies. So, these are big companies and carry some good reputation in the market.

Security wise, my feeling is that these companies are not going to default on their principal & interest payments. Their ratings depend on many factors, which one needs to analyse before coming to any conclusion. Personally, I think HUDCO’s business model at present is better than REC’s.

In case of any dip in their financial conditions, personally I want government not to intervene in such matters as it is not government’s job to oversee their day to day business operations. But still I think because it is India, the government will most likely come to their rescue.

My point of investing in these bonds is, even if you are a risk averse investor, then invest in these bonds considering them “tax-free fixed deposits” and don’t follow their price movement. If you get price appreciation in these bonds, then it is a bonus for you. If you see price trading below its issue price, just ignore it and enjoy the tax-free interest. I personally see many positives of these bonds over bank FDs.

Yes, your understanding is correct, “tax free bonds are those where principal amount shall be refunded by the company on maturity and interest shall continue to be paid at regular annual intervals”.

I tried to write in Hindi but your site did not accept that, I think. I really congratulate you for timely replying almost all queries of all readers. I do also blog on internet. Some pages do also I run on Facebook but never respond to all queries. It is practically not possible. I really wish you my best wishes for such a job.

Thanks a lot for your kind words Anurag !! I truly wish we are able to keep doing this quality work for the investing community living here in India or abroad!

Dear Shiv,

How are you doing?

Any idea on the Tax liability of these Bonds for NRI’s in their Home Country?

For instance, if I am an NRI from USA; what would be my tax liability in the USA?

Kindly advise.

Regards,

Prem

Hi Prem,

I am doing good, thanks !!

Sorry Prem, I am not 100% sure about the taxation laws for NRIs as far as these tax-free bonds are concerned, including the US based NRIs.

dear mr Singh and Mr Prem,

this is regarding income tax liability of NRIs in USA.

in USA you have to pay taxes on your global income. thus you have to pay taxes for your interest earned in both tax free bonds and your deposits in NRE deposits! These are tax free in India only but not in USA.

this is what I think, though I am no tax expert.

If that is true why would an NRi invest in tax free bonds at 8% and pay taxes in US?

can some tax expert confirm what Ramesh has suggested above.

Dear Sir,

I am a novice to the bond market, i have the following questions.

Could you please throw the light on the cess on the tax free bonds?eg. If i invest 5 lacs in the bond as a retail investor, how much cess i have to pay to the government.

If i do not sell the bonds and retain for the tenure period of (10/15/20 years), is there any appreciation/depreciation on the initial investment?

Thanks in advance.

Ravi

Hi Ravi,

There is no cess that you are required to pay to the government if you decide to invest in these bonds. What kind of cess you have in mind?

On the date of maturity, there is no scope of any appreciation or depreciation.

Day 4 (September 20) subscription figures:

Category I – Rs. 50.50 crore as against Rs. 480.92 crore reserved

Category II – Rs. 204.24 crore as against Rs. 961.84 crore reserved

Category III – Rs. 321.72 crore as against Rs. 1,442.76 crore reserved

Category IV – Rs. 506.90 crore as against Rs. 1,923.68 crore reserved

Total Subscription – Rs. 1,083.35 crore as against total issue size of Rs. 4,809.20 crore

Any AAA rated or PSU bonds for non tax paying people with interest rate better than bank FD?

SBI Bonds are ‘AAA’ rated with coupon rate of 9.95% & YTM of approximately 9.55% – http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=SBIN&series=N5

Is this SBI bonds are tax free? I see the price is 10.72 as per above link. So, if I have to buy from open market I assume that I have to pay 10.72 for Rs 10 bond. Are there any other charges like commissions / trade fees? I see the interest rate is 9.55, how many years that this interest will be available? How to buy these bonds? I will be interested only if they are tax free and long term. Please let me know. Thanks for your help.

Regards,

Sundar.

These SBI NCDs are taxable, so I think there is no point mentioning other details here.

I read in newspaper that PFC has filed draft prospectus with SEBI. so we should see the issue this month end.

I think IIFCL issue should hit the markets before the PFC issue.

thanks sir. when is the issue expected?

I think it should hit the markets within the next couple of weeks.

Will the IIFCL issue open before the HUDCO closes ? 🙂

🙂 Yes, I hope so!

We should be able to witdraw from hudco and appl for IIFCL then right if interest are better in IIFCL ?

Sorry Pradeep, I didn’t get you. Can you please reframe your query?

Trading website allow us to withdraw bid for IPO. I am guessing similarly we can withdraw our money for bond issues needed. I have never tried this. Will this work ?

Yes Pradeep, you can withdraw/modify your application for NCDs/Bonds as well.

http://www.financialexpress.com/news/iifcl-to-raise-rs-7000-crore-through-taxfree-bonds/1174225

IIFCL to open in Oct

Looks like 10 yr ROI will be around 8.25 % p.a ?

I think it should come in the 1st week of October.

sir,

What do you think ROI will be ?

It is very difficult to make a guess at this point. Still I think, for retail investors, it should be between 8.2-8.4% for 10 years.

Hi

How do we get the tax exemption for these bonds while filing for IT returns. Do these fall under the 80 (C) category?

Regards

spd

Hi spd,

There is no tax exemption under any section of the IT act on the principal amount of these bonds. Only the interest earned on the investments made is tax-free.

Hi Shiv – With RBI increasing Repo rate today, do you see any increase in coupon rate being offered by any of the upcoming bond issues?

Hi Jitendra,

Not yet. I don’t think the coupon rates are going to go beyond HUDCO’s rates, unless the 10-year G-Sec rate once again crosses the 9% mark.