This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

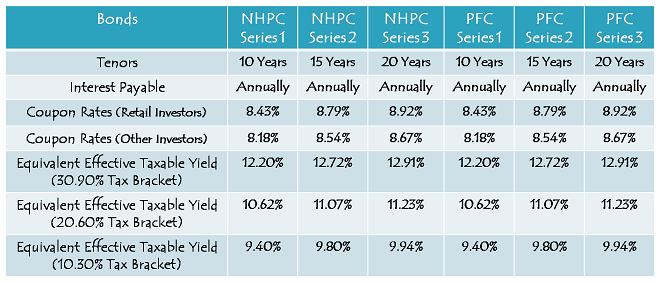

NHPC Limited (formerly National Hydroelectric Power Corporation) will launch its issue of tax-free bonds from October 18th, the coming Friday. Coupon rates of NHPC are absolutely same as they are offered by PFC in its issue which is getting open for subscription from today i.e 8.92% per annum for 20 years, 8.79% per annum for 15 years and 8.43% per annum for 10 years.

NHPC has decided to run this issue till November 11th, the same date on which the PFC issue is also slated to get closed. But, in case of oversubscription or undersubscription, the company has the authority to preclose the issue or extend the issue closing date.

Size of the Issue – The base size of the issue is Rs. 500 crore and there is a green-shoe option with the company to retain oversubscription of an additional Rs. 500 crore, thus making this issue of Rs. 1,000 crore the smallest of all the tax-free bond issues launched this financial year so far.

Rs. 1,000 crore is the total amount NHPC has been authorised to raise from tax-free bonds this financial year. I think NHPC will not be required to do any private placement to raise money from tax-free bonds as there is enough appetite for its high yielding bonds in the market.

Red Signal again for NRIs – Like IIFCL did that first, NHPC has also decided not to offer these bonds to the non-resident Indians (NRIs) and qualified foreign investors (QFIs). So, if any of the NRIs wants to invest in the tax-free bonds yielding as high as 8.92%, then he/she will have to opt for the PFC issue.

Rating of the Issue – Like PFC issue, NHPC issue is also ‘AAA’ rated. ICRA, CARE and India Ratings have assigned ‘AAA’ rating to this issue, which is their highest rating to any debt issue. Also, the bonds will be ‘Secured’ by a pari passu first charge on specific assets of the company, with an asset cover of one time of the total outstanding amount of bonds.

Listing – NHPC has become the first company to propose and obtain the necessary approval to get its tax-free bonds listed on the National Stock Exchange (NSE) as well as on the Bombay Stock Exchange (BSE) this financial year.

Investors can apply for these bonds either in demat form or in physical form, as per their choice. The company will get the bonds allotted and listed within 12 working days from the issue closing date.

No Lock-in Period – As these bonds get traded on the stock exchanges and do not provide any tax deduction u/s 80CCF or 54EC, there is no lock-in period with these bonds. The investors are allowed to sell these bonds at the prevailing market rate whenever they want to do so. There are no charges involved with premature encashment and there will not be any tax penalty payable to the tax authorities.

No TDS – As these are tax-free bonds, there is no question of TDS getting deducted, whether you take them in physical form or demat form.

Interest Payment Date & Record Date – NHPC has decided to fix April 1, 2014 as the first interest payment date. For subsequent years also, interest will be paid on April 1st every year. The record date for payment of interest or the maturity amount will be 15 days prior to the date on which such amount is payable.

Categories of Investors & Allocation Ratio – The investors again have been classified in the following four categories and each category has certain percentage of the issue reserved for the allotment:

- Category I – Qualified Institutional Bidders (QIBs) – 15% of the issue is reserved

- Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved

- Category III – High Networth Individuals (HNIs) including HUFs – 25% of the issue is reserved

- Category IV – Resident Indian Individuals (RIIs) including HUFs – 40% of the issue is reserved

Allotment on FCFS Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Minimum & Maximum Investment – Investors are required to apply for a minimum of five bonds of Rs. 1,000 face value each, thus making Rs. 5,000 as the minimum investment to be made. An applicant may choose to apply for these bonds of the same series or across different series also.

Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest on Application Money & Refund – NHPC will pay interest to the successful allottees on their application money at the applicable coupon rates, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Though the issue is getting launched four days after the PFC issue, I think it is very important for the investors, who are planning to invest in PFC and NHPC both or only in NHPC, to first go for the NHPC issue as soon as possible because the issue size in itself is relatively much smaller. Retail investors will have only Rs. 400 crore to be invested in this issue as compared to Rs. 1,550.36 crore to be invested in the PFC issue.

Also, I think the spillover portion of the non-retail investors is unlikely to fall into retail investors’ kitty this time around. As compared to the PFC issue, I think there is a high probability that this issue will get a better response from the non-retail investors also, as they would like to diversify their investments across different companies and this is the first time NHPC has been issuing these tax-free bonds through a public issue.

That is why, I think this issue will get preclosed much earlier than its official closing date of November 11th. I am expecting this issue to get oversubscribed very soon and get closed in October itself.

Application Form of NHPC Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHPC tax-free bonds, you can contact me at +919811797407

Shiv,

Is the interest received on application money in these tax free binds also tax free or is that treated as normal income and hence taxable

Hi Vivek,

Interest received on the application money in these tax free bonds is taxable and TDS will get deducted, if applicable.

Hello Shiv,

Thanks!

One more query pl – in case NHPC suffers bad losses in future (15/20 yrs is a long time), are the investors still guaranteed of this interest for full term and principal back?

Regards.

Hi Mithun,

Interest rate is fixed and not guaranteed by either NHPC or the government of India. But, at the same time, the probability of a default is very low and the govt. is expected to back NHPC in case there is any default.

This is what International Rating Agency S&P had to say about NHPC in 2009 – “There is a high likelihood that the government of India would provide extraordinary support for the company in the event of any financial distress”.

http://www.onemint.com/2013/10/17/comparative-analysis-pfc-8-92-vs-nhpc-8-92-which-tax-free-bonds-issue-is-better-to-invest/

Hello Shiv,

Thanks for all the wonderful information!

I am planning to invest in such tax free bonds for the first time.

One query – the interest (every year) would be directly credited to my a/c, or thru cheque?

Same for principal post maturity? I use ICICI Demat.

Thanks much,

Mithun.

Hello Mithun,

You’ll get the interest directly credited to your bank A/c. which is linked to your demat A/c. as you get dividends on shares you’ve invested in.

Hi Shiv

Many thanks for your in-depth analysis and clear,informative answers to all queries here.

I have few questions regarding this :

1) Where can I buy this TF Bond from? Online is it,do you have a link ? Online search brought me to One Mint,but couldn’t find a direct link.

2) I have ICICIDirect Demat account – Can I buy through them ? Can I buy in the after-market hours/weekend( Saturday evening/Sunday morning ), as me being an Orthopaedic Surgeon,won’t get time otherwise.

3) With regards to TF Bonds, especially for CPSEs, I find it difficult to comprehend, which to go for – buy now or wait for another one with better interest rate or better rating etc.

What is the correct approach in this regard ? What I mean is, almost all Bonds on their way,would have similar interest rates with a little +/-, so what should be the approach to find the real Gem from a Lemon ?

Thanks a lot again

Hello Dr Datta,

1 & 2. You can apply for it online with your ICICI Direct A/c. Just login into your A/c. & check whether ICICI Direct’s platform allows you to apply for it on the weekend. Most likely it will.

3. Rating cannot be better than ‘AAA’, but a company can. NHPC is a good company, NTPC is a good company, IIFCL is also good and there are other good companies also. Interest rates move up or down and like stock market, nobody can forecast their exact movement.

You’ll have to keep a track of certain things to be more familiar with all these things or probably hire an unbiased financial adviser who can advise you in all these matters.

Day 1 (October 18th) subscription figures:

Category I – Rs. 420 crore as against Rs. 150 crore reserved

Category II – Rs. 632.63 crore as against Rs. 200 crore reserved

Category III – Rs. 390.89 crore as against Rs. 250 crore reserved

Category IV – Rs. 171.82 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 1,615.34 crore as against total issue size of Rs. 1,000 crore

Bumper opening day subscription figures due to huge investments by Category I, Category II & Category III investors.

Issue is still open or closed? Retail portion is still unde -subscribed, so can we apply now?

Yes, it is still open, no announcement of early closure by the company so far. Retail Investors can still apply.

Applied. Hopefully broker will place the order on Monday morning. Thanks!

Great !!

i have applied for 10 yrs bond.

That’s good, but why 10 years? Don’t you think it is better to go for 15 years or 20 years?

Sir,

I am some how not comfortable with long tenure. We cannot predicate how company will perform over such a long term.

When is NTPC issue coming up?

hmm.. ok.. no idea of NTPC issue as yet.

Any other issue coming up ?

Hi Pradeep,

No company is planning to launch an issue before Diwali. NHB & NTPC are lined up with their issues in November some time.

Hi, here is a useful snippet from the NHPC prospectus: “For each Portion, all Applications uploaded into the electronic system of the Stock Exchanges in the same day would be treated at par with each other. Allotment within a day would be on proportionate basis, where Bonds applied for exceeds Bonds to be allotted for each Portion respectively. Minimum allotment of One Bonds and in multiple of One Bonds will be made in case of each valid Application.”

This seems to imply that allotments would approximately be made for category III in the proportion of 250:391, that is, ~64% of applied for bonds. Would this be a correct deduction?

Thanks Ramachandran

A follow-up question: if (hypothetically), there were to be a level of oversubscription in Category III such that proportional allotment leads to bonds of less than Rs 10 lacs for some individual investors, would they automatically move to the retail investor category?

This is the most intelligent query I have received so far Mr. Ramachandran! Though I am not 100% sure about it, but all logics suggest me that yes, they would automatically move to the retail investors category as the interest payment is made as per the no. of bonds held in your name on the “Record Date” based on your PAN number.

Thanks for such a query, I really appreciate it!

Hi Shiv,

When NHAI and PFC had come out with the first tax free issue (the ones that offered 8.2% and 8.3% respectively with no step down feature), I had applied for both in the HNI category (>5L) on Day 1 itself but did not receive full allotment and my allotment in each was less than the retail limit of 5L. However, this did not upgrade me to the Retail category of 8.3%. I was recorded as a HNI investor and receive 8.2% against 8.3%.

I am not sure if this will be the same case now but stating this personal experience as you also mentioned you were not 100% sure.

Hi Sanjay,

With NHAI bonds, there was no difference in the rate of interest among Retail Investors, HNIs & Institutional Investors. There were categories of investors only for the allotment purposes. 8.20% was for 10 years and 8.30% was for 15 years.

With the current offers, my reasoning still remains the same. Even further buying or subsequent selling will move an investor to different categories for the interest payment purposes.

Yes, you are right Mr. Ramachandran, it would be in the ratio of 250:391.

Sir,

Is it possible to invest in the tax-free bonds in the name of the minor? When the minor attains majority will the bonds will be in the name of the minor and guardian jointly or will it be in the name of the minor only? (assuming the bonds are in physical form)

Secondly are these bonds transferable? I want to invest some money for the benefit of my child who is a minor now and will attain majority in November 2014. Can I apply the amount in my name now and transfer the money in her name and my name (with option either or survivor) after she attains majority?

Thanks

Jayashree

Hi,

Yes, you can make this investment in the name of a minor. Also, it will remain in the name of your daughter only when she becomes a major child. Moreover, these bonds are transferable also, but not sure if it is possible to do that in the same manner as you have mentioned in your query.

Your posts are very useful for info & analysis. There have been 4 tax-free bonds during last 2 months & still IRFC ++ are expected. Any idea when these annual interests are payable – Financial year-end?

Thanks Easwaran!

Different companies fix different dates for making interest payments, like REC has fixed it as December 1st, NHPC has fixed it as April 1st, HUDCO, IIFCL & PFC have not declared their interest payment dates as yet and their dates would be as per the deemed date of allotment.

regarding the NCD tax free bonds, kindly clarify one doubt, is it over subscription portion is also alloted on proportionate basis. is it retail investors(below 10 lakhs) will get 40% of share on entire issue size or only original portion.

Hi Raja,

40% reservation for the retail investors is there on the total issue size. As with NHPC, the total issue size is Rs. 1,000 crore, so Rs. 400 crore is for the ratail investors. In case of undersubscription in any of the categories below the portion reserved for it, first preference goes to the retail investors. With REC, Category I was undersubscribed, so the retail investors got full allotment, even beyond 40%.

If all the categories get oversubscribed to the maximum extent, then only the portion reserved for each category will get allotted.

Hi Shiv,

Below link gives info about 10 yr Govt bond yield.

http://www.bloomberg.com/quote/GIND10YR:IND/chart

As seen from the chart, yield was highest on 19-Aug-2013. Due to this, REC, HUDCO were able to offer good interest rates. I think these companies offer interest considering last 2 weeks yield. Is it correct?

How come recent bond (PFC, NHPC) offers more interest when yield is actually falling?

Thanks,

Amit.

This is an interesting question. Even I would like to know the answer of the same…

Hi Amit, Hi Deepak,

Yes, you are right, it is two week. Here is the exact wordings of the CBDT notification – “The reference G-sec rate would be the average of the base yield of G-sec for equivalent maturity reported by Fixed Income Money Market and Derivative Association of India (FIMMDA) on a daily basis (working day) prevailing for two weeks ending on Friday immediately preceding the filing of the final prospectus with the Exchange or Registrar of Companies (ROC) in case of public issue”.

As you can observe it yourself from the link pasted, the rise of 19th August in the yield was very steep and the two week average on Friday before the prospectus filing date would be lower for REC as compared to PFC and NHPC. That is the reason, why their yields are higher than REC.

The coupon difference between REC & PFC/NHPC is more in the 15-year and 20-year bonds, as the recent Repo Rate hike has pushed yields higher for the longer duration bonds.

Hi Shiv,

I have 2012 REC bond (paper document), as you know the interest rate is more than 1% less than current offerings. I would like to sell that and plan to invest that in current tax free bonds. I know it may be at loss, but thinking of 10/15 years, I think that will be big benefit. How long it will take to sell that and what is the procedure to do that? Can you let me know? Thanks

Regards,

Sundar.

Hi Sundar,

If you have a demat account, get your physical bonds dematerialised. It depends on your broking house & its staff how soon they are able to get it done for you, without any rejection by the broking house itself and then the Registrar of REC.

If the whole process gets executed superfast, then it should take a minimum of 10-15 days for your bonds to get dematerialised. Once that is done, you can sell your bonds that day itself.

I don’t have a demat account. Is it required to sell the bonds? Will it take that long? Is there a way without demat account that I can sell these bonds? Please let me know. Thanks

Regards,

Sundar.

Hi Sundar,

It is not mandatory to have a demat account to sell these bonds, but it is mandatory to have a demat account to sell them on the stock exchanges where there is a liquidity for these bonds. If you are able to find out a buyer for your bonds privately, which I think is extremely difficult, then only you can sell these bonds in the physical form.

With repo rates set to rise, it might be wise to put 50% of yr tax free bonds allocation now and wait for reminder 50% for some more issues to come out. IRFC, NHAI are the 2 big issues which will come out. Complete list of guys authorised to raise is as below

REC( 5000 crores)

HUDCO( 5000 crores)

IIFCL( 10000 crores)

PFC( 5000 crores)

NHPC( 1000 crores)

NHAI( 5000 crores)

IRFC( 10000 crores)

National Housing Bank( 3000 crores)

Ennore Port( 500 crores)

NTPC( 1750 crores)

IREDA( 1000 crores)

AAI( 500 crores)

Cochin Shipyard( 250 crores)

Total( 48000 crores)

Hi Shiv and thanks for your continued support. Just want to ask you with inflation rising and bond price dropping, markets are expecting few more rate increases till mid of next year. Do you think it’s still wise to invest in current TFB issues or better we should wait for upcoming issues later or early next year for higher yields ?

Hi, I think the rates have been rising in a panic and are not coming down due to rupee fall & high inflation. Some factors suggest me that inflation/rates should moderate, but how & when, it is difficult to tell. So, I don’t want to wait for rates to rise more, that is why I am putting my money in these two issues.

Are these bonds available to U.S. retail investors via self-manged accounts at discount brokerage firms? Also, does the underwriting allow for additional issues if the existing series is exhausted?

Hi AWB,

Persons resident outside India and foreign nationals (including Non-Resident Indians (NRIs), Foreign Institutional Investors (FIIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this NHPC issue.

These companies are allowed to raise certain amount from the markets. For NHPC, the amount is Rs. 1,000 crore which it plans to raise in this issue itself.

http://www.onemint.com/2013/08/16/tax-free-bonds-notification-fy-2013-14/

Thanks Shiv!

You are welcome Jitendra!

Hi Shiv,

Do these bonds have a call option? I mean, can the company call the bonds back by paying the investor – or will this run for full 20 years(or I can sell in market)?

If I am purchasing these bonds later from market(less than 10 lakh) will I be treated as Retail investor and get the higher interest rate?

Hi Paul,

There is neither a call option with the company nor a put option with the investors in this issue. You can sell these bonds in the market.

If your investment is less than Rs. 10 lakh on the record date, you’ll be treated as the retail investor and entitled to a higher rate of interest, even if buy these bonds from the open market.

Hi Shiv,

Are there any more TF bonds expected in this financial year?

Which ones are those and around which month are they expected?

Thanks in advance…

Regards,

Deepak

Hi Deepak,

These companies are allowed to raise Rs. 48,000 crore with tax-free bonds this financial year, out of which approximately Rs. 12,000-15,000 crore have been raised by them so far. They are still to raise the remaining amount of Rs. 33,000-36,000 crore. So, you can expect many such issues in the days & months to come.

I have information of only one more company so far and that is National Housing Bank (NHB). I think it will be issuing its bonds in November. Don’t know the rate of interest.

Sir, can we apply multiple times for an issue subject to overall limit of 10L?

e.g. 50k on 18th and then 25k on 22nd or so..

Hi Ashish,

Yes, you are allowed to submit multiple applications within the overall limit of Rs. 10 lakh under the retail individual investor category. But, if you are applying for it online, then you should check with your broker first about their policies regarding this.

Thanks Shiv for the details on NHPC TFB!

You are most welcome Amlan!

Hi Shiv,

Have been always saying this and I say it once again, one mint and you have helped in making us more knowledgeable and have always given great advise. Thanks !!

Wanted to check few things on this issue:

1. If I sell these bonds after a couple of years in the market and if I make a profit – will I need to pay income tax on the profit amount ?

2. My father is a NRI – if he invests in the PFC NRI category issue and again sells these in the market – will he need to pay income tax on the profit ?

Thanks a lot Kunal for your motivating words !!

1. Yes, if there is any long term capital gain, then you’ll have to pay LTCG tax at flat 10% of the capital gain. e.g. if you sell any of these bonds at Rs. 1,050 each after 2 years, then you’ll have to pay Rs. 5 as LTCG tax.

2. For NRI taxation, read this text from the PFC prospectus, as I am not 100% sure about its exact treatment.

“Under section 195 of the Income Tax Act, Income Tax shall be deducted from sum payable to non residents on the long term capital gain at the rate of 20% (plus applicable surcharge and education cess) and short term capital gain at the normal rate of tax (plus applicable surcharge and education cess) arising on sale of bonds.

As per section 90(2) of the IT Act, the provision of the IT Act would not prevail over the provision of the tax treaty applicable to the non-resident to the extent such tax treaty provisions are more beneficial to the non resident. Thus, a non resident can opt to be governed by the beneficial provisions of an applicable tax treaty”.

So, I think TDS will get deducted @ 20% and the exact taxation is country specific.

Thanks for the timely post,

2 questions

1.Any drwaback/negative factor in NHPC like you mentioned in PFC?

2.Any advantage/difference/benefit of one over the other?

Hi Saurabh,

I am trying to do a comparative analysis between the two, let’s see if I am able to do that in time.