This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

“Beti Bachao, Beti Padhao” is the mantra with which Prime Minister Narendra Modi launched Sukanya Samriddhi Yojana on January 22nd this year. Later on, the government issued a notification to allow 80C exemption equal to the amount invested in the scheme up to Rs. 1,50,000, which is also the maximum amount one can invest in this scheme in a financial year.

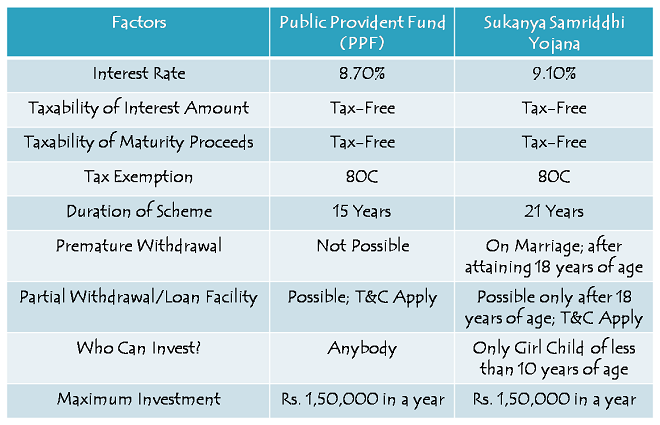

Now, the Finance Minister in his budget speech has proposed to make the interest component as well as the maturity proceeds as tax-free. I think this proposal has made this scheme to be the best small savings scheme available to the Indian investors. Yes, even better than our golden scheme of Public Provident Fund (PPF). So, what is this scheme all about? Let’s check.

Sukanya Samriddhi Yojana is a small savings scheme which can be opened by the parents or a legal guardian of a girl child in any post office or authorised branches of some of the commercial banks. The girl child is called the “Account Holder” and the guardian is called the “Depositor” in this scheme.

Before I compare this scheme with PPF, let us first check the important features of this scheme.

Salient Features of Sukanya Samriddhi Yojana

Who can open this account? – Parents or a legal guardian of a girl child who is 10 years of age or younger than that, can open this account in the name of the child. For initial operations of the scheme, one year grace period has been provided to make it 11 years of age. With this one year grace period in age, which is valid up to December 1, 2015, you can get this account opened for a girl child who is born between December 2, 2003 and December 1, 2004.

9.1% Tax-Free Rate of Interest – This scheme has been flagged off with a 9.1% rate of interest, higher than that of PPF which stands at 8.7%. But, this rate is not fixed at 9.1% for the whole tenure and is subject to a revision every financial year like all other small savings schemes, including PPF.

Prior to the budget announcement, 9.1% annual return seemed unattractive, but not anymore, as it has been made tax exempt now. Interest amount gets added to your balance amount in the account and compounded either monthly or annually, as per your choice. Monthly interest compounding will be done only on your balance amount on completed thousands.

Duration of the Scheme – The scheme will mature on completion of 21 years from the date of opening of the account. If the account is not closed on maturity after 21 years, the balance amount will continue to earn interest as specified for the scheme every year. In case the marriage of your daughter takes place before the maturity date i.e. completion of 21 years, the operation of this account will not be permitted beyond the date of her marriage and no interest will be payable beyond the date of marriage.

Deposit for 14 years only – Though the scheme has a duration of 21 years, you are required to make contributions only for the first 14 years, after which you need not deposit any further amount and your account will keep earning the interest rate applicable for the remaining 7 years.

Premature Closure – The account can also be closed prematurely as your daughter completes 18 years of age provided she gets married before the withdrawal. As the maximum permissible age of the girl child is set as 10 years, the scheme effectively carries a minimum duration of 8 years i.e. 18 years of exit age – 10 years of entry age.

Partial Withdrawal – It is also allowed to withdraw 50% of the balance standing at the end of the preceding financial year, but only after your daughter attains the age of 18 years. So, effectively it has a complete lock-in period of at least 8 years, before which you cannot take out any money for any purposes.

Minimum/Maximum Investment – You need to deposit a minimum of Rs. 1,000 in a financial year to keep your account active. Failure to do so will make your account inactive and it could be revived only after paying a penalty of Rs. 50 along with the minimum amount required to be deposited for that year, which currently stands at Rs. 1,000.

Also, you can invest a maximum of up to Rs. 1,50,000 in a financial year. You can make your contribution to this account in as many number of times as you like.

How many accounts can be opened? – You can open only one account in the name of one girl child and a maximum of two accounts in the name of two different children. However, you can open three accounts if you are blessed with twin girls on the second occasion or if the first birth itself results into three girl children.

Nomination Facility – Nomination facility is not available in this scheme. In an unfortunate event of the death of the girl child, the account will be closed immediately and the balance will be paid to the guardian of the account holder.

Documents Required – Birth Certificate of the girl child, along with the identity proof and residence proof of the guardian, are the mandatory documents required to open an account under this scheme. You can approach any post office or authorised branches of some of the commercial banks to get this account opened.

Sukanya Samriddhi Yojana vs. Public Provident Fund (PPF)

Budget 2015 has made this scheme quite attractive for the investors. If you’ve already exhausted your PPF deposit limit, want to save for your girl child’s marriage or higher education and have spare money to invest in this scheme, then this scheme provides you one more excellent avenue of safe investment with high returns. You can wait for the next financial year’s rate of interest to get announced anytime this month, if it remains higher than PPF, just go for it.

Application Form to open a Sukanya Samriddhi Account

List of authorised commercial banks where you can get this account opened

Hi,

My daughter is 9 yrs old ,if i have to pay for 14 yrs ,she will be 23 yrs.Or i have to pay till her age 21 yrs?Is it mandatory to pay for 14 yrs?

hello sir,

my daughter is 2yrs old,so i will have pay for 14yrs under this scheme that means she turns 16.

i would like to no will the maturity amount wary according to your chart depending on the age of my daughter.

will acknowledge your reply.

Hi Samkit,

Maturity amount will vary as per the rate of interest, the amount of your contribution and the month of deposit. Your daughter’s age has no role to play in the maturity amount, if it is withdrawn after 21 years.

Hi sir i have two daughters can i open two

Hi Manju,

Yes, you can open two accounts.

I have just posted an article having a sample duly filled application form, please check – http://www.onemint.com/2015/03/12/sukanya-samriddhi-yojana-sample-filled-application-form/

Hi Shiv, I saw the sample application form but it doesnt answer my query on “Insurance” and “Committed Deposit”.

Santosh

Hi Shiv, nice presentation and of course it is one of the best saving scheme. As on date, since Banks are not opening this (I am more interested to open in bank for easy in online transfer), I will try to open in nearest post office and may be in future, Govt may come up with bank-post office transfer facility.

I am searching but could not get the answer on “insurance protection”. What happens if the depositor (suppose the sole earning member of the family) dies and the family unable to continue the scheme? Will the Govt waive the future payments or the account will be inactive in the due course? I think the “inactive” answer is correct?

Second, I feel, this scheme runs like PPF and not like RD. I mean to say, in RD (Recurring Deposit), we commit to pay a fix amount per month whereas in PPF, there is no monthly commitment and the depositor is free to deposit amount of his choice subj to min of 500 and max of 150,000 in a year. To keep PPF account active, one has to do minimum 1 deposit in a year and subject to minimum of Rs. 500/- yearly deposit. If this is the case also in Sukanya account, I dont think Death of sole earning member causes any problem. Family can continue one deposit (1000/-) in a year and keep the account active.

Am I right in my thought?

Regards

Santosh

Thanks Santosh,

1. Migration facility will definitely be there once the scheme becomes fully operational.

2. There is no insurance protection clause in this scheme and the government will not waive any future payments. Under special circumstances, like death or medical support in life-threatening diseases etc., you can make a request to prematurely close the account and withdraw the amount.

3. This scheme is very much similar to PPF. You can keep the account active by depositing a minimum of Rs. 1,000 in a financial year. However, in case of guardian’s death, I think you’ll have to get the guardian’s name changed in the records of the post office/bank branch.

Hi Shiv Sir,

will the partial withdrawal be tax free?

Hi Vinay,

Yes, the partial withdrawal will also be tax-free.

Good morning sir,

my reletives very poor so-

main jaana chahta hu ki_ wo year main 1000rs. hi deposite ker sakti hain,

1- so minimum amount jo 1000rs. h se account open kerne k baad v unhe kya us year me 1000rs(minimum yearly amount) alag se deposite kerna hoga,

2- unki 4 daughters me se two daughters ten year k under age h so kya wo dono k lea is scheme me account open ket sakti h.

3- ak daughter 8 year ki h to or maan lo ki uski marriage 10 saal baad yani uske 18 year me kerna h to kya uske k lea 10 year baad Account close ker full amount withdrew ker sakte h.

pls reply sir….

Very vary Thank you..

Hi Rohit,

1. Nahin, ek saal mein bas ek deposit karna hoga.

2. Haan, das saal se neeche account open kar sakte hain.

3. Haan, marriage hone par account close kar sakte hain.

Sir greetings,

Myself santosh singh,

I wanted to know the amount that I have to invest and how many times I have to pay until the scheme come up to maturity.

In other word basic detail of the scheme so that I can plan this for my two years daughter. What is the maturity amount I will receive when I can plan to invest 1000 per month.

Hope u will reply soon.

Thanks

Santosh

Hi Santosh,

All the details have been mentioned above in the article. You can invest a minimum of Rs. 1,000 and a maximum of Rs. 1.5 lakh. You need to deposit money only once a year and there is no cap on the number of deposits.

Please check this post for the maturity amount after 21 years – http://www.onemint.com/2015/03/09/sukanya-samriddhi-yojana-calculating-maturity-value-after-21-years/

Hi,

Will we get the full amount?.Is it tax free?

Hi Baiju,

Yes, it is tax-free.

Are you telling us that the girl child scheme provides an additional Rs 150,000 deduction under 80c ?

i.e.

PPF Rs 150,000

+

SSY Rs 150,000.

I think it is PPF + SSY <=150,000

please confirm.

No Chirag, 80C deduction is limited up to Rs. 1,50,000 only.

Sir,

How much money required to pay per year

Hi Pushkar,

It is minimum Rs. 1,000 and maximum Rs. 1.5 lakh.

Sir.

Meri beti ki age 15-jan-16 ko 10 yrs ki hogi kya ssy le sakta hun.jab yo 21 ki hogi uski sadi me 500 ke hisab se kitne amt milegi.

Hi Ganesh,

Aap apni beti ke liye SSY account khol sakte ho. Maturity ka paisa rate of interest aur deposit month pe depend karega.

hi,

my girl child borned in 2007 oct , is she eligible?

Hi Sri,

Yes, she is eligible.

Sir

Can father and mother open 2 different account for same girl child.

No, only one account per girl child.

Hello sir,

I want to know will it give benefit in income tax

Hi Vaishali,

Yes, your contribution will be eligible for tax deduction u/s 80C.

Hello sir,

I want to know will ssf provide any benefit to income tax

hi, I have three daughters(triplets). now they are 6 years n 9 months old. one son also there for us aged 4 years. please suggest

1.How much amount to be paid maximum for three account totally in a year in ssa, ?

2.If I take 50% of amount after their 18 years for education, what will be the exact amount I can get after 21 years for one account, eg: im investing rs.150000 yearly?

3.can I open ppf for my son under my wife name?

4.any other investments for my son for his education and marriage?

Hi Mani,

1. Rs. 4.5 lakh is the maximum amount you can contribute in three of your SSA accounts.

2. Calculating the exact amount is not possible, so it is only a tentative figure which can be calculated.

3. Yes, you can open a PPF account for your son. But, maximum contribution in PPF is limited to Rs. 1.5 lakh for son & the guardian.

4. We do not entertain individual personal queries here on this forum. We provide financial planning services to interested individuals – http://www.onemint.com/services/

thanks for the reply

You are welcome!

My daughter d.o.f is 06th November 2013 can I apply of this scheme

Plz send me reply to my mail id.

Hi Akhil,

Your daughter is eligible for you to get an account opened for her.

My daughter d.o.f is 10th November 2003 can I apply of this scheme

No, your daughter is not eligible for this scheme.

Hello shiv Ji,

1)Plz tell me the exact figure that I recieve after 21 years if I deposit 150000 rs per year for 14 yrs.

2) If I deposit 12000 per year then how you give the exact figure of 641092 rs that you mention in the vouchers after 21yrs

Hi Mr. Kulwinder,

1. Please check this post to check the tentative maturity amount you’ll get after 21 years – http://www.onemint.com/2015/03/09/sukanya-samriddhi-yojana-calculating-maturity-value-after-21-years/

2. Nobody can predict the exact maturity figure after 21 years. Whatever has been mentioned is only tentative, based on certain assumptions.