This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

SBI Life Insurance Company Limited is all set to enter the primary markets through its initial public offer (IPO) of Rs. 8,400 crore from September 20. The IPO is an offer for sale (OFS) by SBI Life’s promoters, State Bank of India (SBI) and BNP Paribas Cardif S.A. The company has fixed its price band in the range of Rs. 685-700 a share. Subscription to the issue will remain open for three days to close on September 22.

The offer would carry 12 crore shares for subscription and constitute up to 12% of SBI Life’s post-offer paid-up equity share capital. Though the company offers no discount to the retail individual investors, there will be a discount of Rs. 68 a share for the employees of the company. Moreover, around 1.40 crore shares have been reserved for the SBI shareholders and the employees of the company.

Here are some of the salient features of this issue:

Size & Objective of the Issue – SBI and BNP Paribas Cardif S.A. are collectively selling their 12% stake in SBI Life in this IPO to raise Rs. 8,400 crore. SBI Life will not get any proceeds from this offering.

Price Band – SBI Life has fixed its price band to be between Rs. 685-700 a share and the company has decided not to offer any discount to the retail investors.

Discount of Rs. 68 for Employees – The company has decided to offer a discount of Rs. 68 a share to its employees, which is approximately 10% to the issue price.

No Discount for Retail Investors – The company has decided not to offer any discount to the retail investors.

Retail Allocation – 35% of the issue has been reserved for the retail individual investors (RIIs), 15% for the non-institutional investors (NIIs) and the remaining 50% shares will be allocated to the qualified institutional buyers (QIBs).

Reservation for SBI Shareholders & SBI Life Employees – SBI Life has reserved 1.20 crore shares for the existing shareholders of its parent company, State Bank of India (SBI), and 20 lakh shares for the employees of SBI Life.

Multiple Bids by Employees & SBI Shareholders Allowed up to Rs. 2 lakh – SBI Life employees and SBI shareholders placing their bids up to Rs. 2 lakh can place their bids in the retail individual investors (RII) category as well. Technically these seem to be multiple bids, but it is allowed to place multiples bids in such a manner.

However, you need to be careful that your bid amount in each of the categories does not cross the limit of Rs. 2 lakh. If your bid amount as an SBI Life employee or as an SBI shareholder crosses Rs. 2 lakh and you place one more bid as a retail investor as well, in that case your multiple bids are liable to get rejected.

Bid Lot Size & Minimum Investment – Investors need to bid for a minimum of 21 shares and in multiples of 21 shares thereafter. So, a retail investor would be required to invest a minimum of Rs. 14,700 at the upper end of the price band and Rs. 14,385 at the lower end of the price band.

Maximum Investment – Individual investors investing up to Rs. 2 lakh are categorised as retail individual investors (RIIs). As a retail investor, you can apply for a maximum of 13 lots of 21 shares each @ Rs. 700 a share i.e. a maximum investment of Rs. 1,91,100. At Rs. 685 per share also, you can apply only for 13 lots of 21 shares, thus making it Rs. 1,87,005.

Listing – The shares of the company will get listed on both the stock exchanges i.e. National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) within 6 working days after the issue gets closed on September 22nd. Its shares are expected to get listed on October 3rd.

Here are some other important dates as the issue gets closed on September 22:

Finalisation of Basis of Allotment – On or about September 27, 2017

Initiation of Refunds – On or about September 28, 2017

Credit of equity shares to investors’ demat accounts – On or about September 29, 2017

Commencement of Trading on the NSE/BSE – On or about October 3, 2017

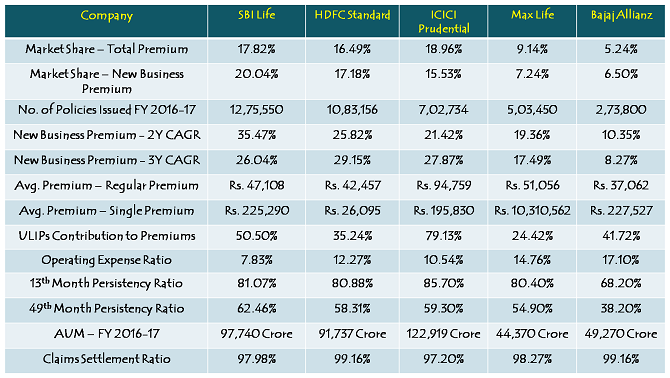

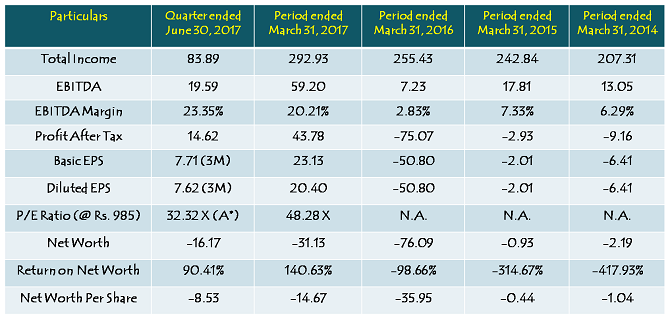

Peer Comparison