Over the past few days I’ve received a few comments whose central theme is safety of returns while providing moderate returns.

I think the bad performance of the stock market over the past few years has made people search for instruments where return of capital is more important than return on capital, and these questions are a result of that mindset.

In this post I’ll be listing out 10 instruments that I think are quite safe for investing along with their tenure, expected return, tax applicability and other notes. If you think something else should be on this list, please leave a comment.

| S.No. | Investment | Tenure | Expected Return | Tax Applicability | Comments |

| 1 | Bank Fixed Deposits | Few days to several years | Usually over 8% | Taxable at the investor’s slab | Bank failures are rare in India so bank fixed deposits are a very safe way to invest your money.You know the rates up front so there is no uncertainty there.Taxes can eat into your returns though, especially if you are in the high tax bracket, but even then a FD that compounds quarterly and is done for a long maturity will yield well.Here is a link to a post which has the list of some of the best bank fixed deposits that are available in India right now. |

| Â 2 | Tax Saver Bank Fixed Deposits | 5 years or more | Â Usually over 8.5% | The amount that you invest in tax saver FD is deductible from your taxable income up to a limit of Rs. 1 lakh under 80C. The interest income itself is taxable. | Like the bank fixed deposit, this is also a very safe and certain investment.The drawback is that money is locked in for at least 5 years, and the positive is that you get some tax benefit to juice up your return.Here is a link to some of the best tax saver fixed deposits available in India right now. |

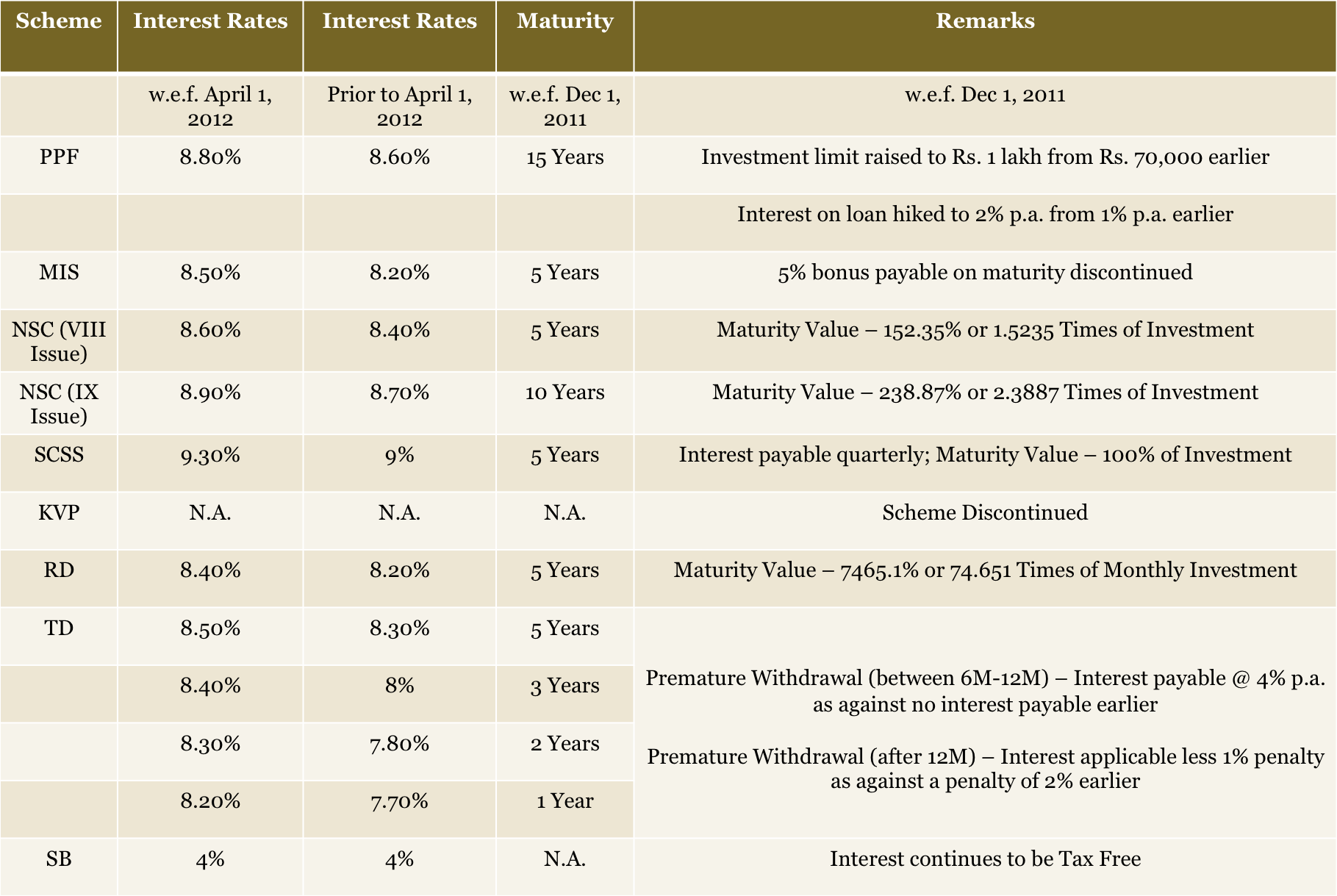

| Â 3 | Public Provident Fund | Â 15 years | 8.8% | The amount you invest is eligible for 80C deductions and the returns are tax free too. | This is also a very safe investment, and the returns are spectacular, specially for someone in the 30% tax bracket.If you don’t mind the 15 year wait period then no other fixed income investment can match the PPF return for the safety it offers. |

| Â 4 | NSC IX Issue | Â 10 years | 8.9% | Interest income is taxable. | This is another safe investment with decent returns.Here is a post with this and other post office scheme details. |

| 5 | Senior Citizens Savings Scheme | Â 5 years | 9.3% | Interest is taxable, investment amount is eligible for 80C deduction. | A lot of readers have commented here over the years about how useful the SCSS is along with the monthly income scheme of the post office for their parents, and relatives and this is a good option as well.Here is a link to an image that has the interest rates for this and comparison with other similar instruments. |

| Â 6 | Monthly Income Scheme | 5 years | 8.5% | Interest income is taxable | This is useful if you are looking for an instrument that gives you a monthly income.Here is link to a post about MIS. |

|  7 | Tax Free Bonds | They trade on the stock exchange so you can buy or sell any time. | Usually upwards of 8% | Income is tax free | I would say that these bonds aren’t as safe as a bank deposit or a post office deposit but they can still be categorized as fairly secure instruments.If you buy these bonds from the stock market right now, they are trading at higher than their face value so your effective yield will be less but then there is always a chance to make capital gains if interest rates come down.Here is a good link on the NSE website that has quotes of all these bonds. |

| Â 8 | Fixed Maturity Plans | 1 year or more | Not fixed but usually comparable to fixed deposits | This is tax efficient when compared with FDs. Read more for details. | Although these are fixed income instruments, there is absolutely no guarantee or indication of what the returns will be like.To that extent, they are very different from the other instruments mentioned in this list.Even then, they are specially attractive to people in the higher tax bracket due to their eventual FD like returns and tax advantage.Read more about FMPs here. |

| 9 | Debt mutual funds | Varying maturities and can be bought and sold anytime. | Not fixed. | Tax on capital gains and dividends. | These are like FMPs in the sense that the returns are not fixed, so they are not meant for you if you can’t handle the uncertainty.Their popularity stems from the fact that they are flexible to buy and sell and have given decent returns in the past. |

| 10 |  Corporate NCDs | Varying maturities |  Higher than fixed deposits. | Interest is charged according to your slab and capital gains are also applicable. | These are higher risk compared with the other instruments mentioned in this list, especially if you invest in a NCD of a company which doesn’t have robust finances.The higher risk means that their return is higher as well and they can be used to juice up your fixed income portfolio but you need to be careful while buying them.This post about 6 things to keep in mind while investing in company NCDs is a good way to get started on this topic. |

| 11 | Savings Account | No Maturity | 4 – 7% | Interest is tax free up to Rs. 10,000 and then charged according to your slab. | A reasonable place to keep your short term funds, but if you have a lot of money in a savings account then you need to consider a FD or some other instrument that can yield higher. |

{kind=link}

All these options are widely known and based on what you want to do and what the rest of your portfolio looks like, you can pick and choose one or more for safety and reasonable returns.

Finally, would you like to add anything to this list?

Update: Added Savings Account per Ankur’s suggestion, please excuse the inaccurate title.

My investment is in sahara plss advise

Useful information

That was a wonderful write-up. I have similar smart investing ideas. Please check the following link https://jagahuntblog.wordpress.com/2016/06/11/3-hotspots-to-invest-in-visakhapatnam/. You would be also glad to view my website http://www.jagahunt.com/site.htm?city=Visakhapatnam.

Hi there to every one, it’s truly a pleasant for me to go to see this website, it contains helpful Information.

dear sir,,

My name is lakhwinder singh ,my father is government employs. He will retired after two year. My question is how my father invest there money after retirement.

Dear friend

My name is Mr.George Wilson from England I have investment

plan in your country India please I need a genuine partner

that will partner with me if you are interested.

kindly contact me for more information

Email:mrgeorgewilson545@gmail.com

Regards

George Wilson

Hi George Wilson

Do you still need a partner if so can give a brief of the investment plan in India

Rgds

viru

SIR IAM INTERESTED IN SHARE MARKET. BUT I DO KNOW ANYTHING ABOUT THAT PLS HELP ME.

My investment is in sahara plz advise m

I want to know about 15 years bond ,what the minimum time period to withdrawal this bond,6time multiple bond .plz send me kind advise I want to withdrawal my money ,I’m in financial problem

Hi

Please suggest me a good plan for my Daughter age 4 years . I can invest per year Rs 24000/- my age is 37 years.

I need to 100% risk free plan which is having higher to higher returns,

Hi Manshu.. Great compilation. You may include Kisan Vikas Patra here.

However, if you are including NCD then you may also include corporate fixed deposits. But these instruments cannot be compared with something like NSC and PPF in terms of safety as they are always prone to default from issuing companies. In last year, we have seen various such cases of default especially coming form Real estate companies.