This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

The Finance Ministry on March 31st announced the applicable interest rates for all the Post Office Small Savings Schemes, including PPF, Sukanya Samriddhi Yojana (SSY) and Senior Citizens Savings Scheme (SCSS). Except for SCSS and SSY, the government has kept all other interest rates unchanged, including 8.7% for its most popular scheme, PPF.

To encourage more and more people to get the Sukanya Samriddhi Account (SSA) opened, the Government has decided to ride against the tide and has increased its interest rate to 9.20% from 9.10% earlier, an increase of 0.10%.

As the interest rate on Sukanya Samriddhi Yojana is subject to a revision every financial year, this rate of 9.2% will remain applicable only for the current financial year, 2015-16 and will be further revised in March 2016 for the next financial year, 2016-17.

But, this move of keeping its interest rate higher makes me feel that the Modi Government will continue to keep its interest rate higher going forward as well. I think, like the current financial year, they will try to keep a differential of approximately 0.50% between PPF and Sukanya Samridhi Yojana.

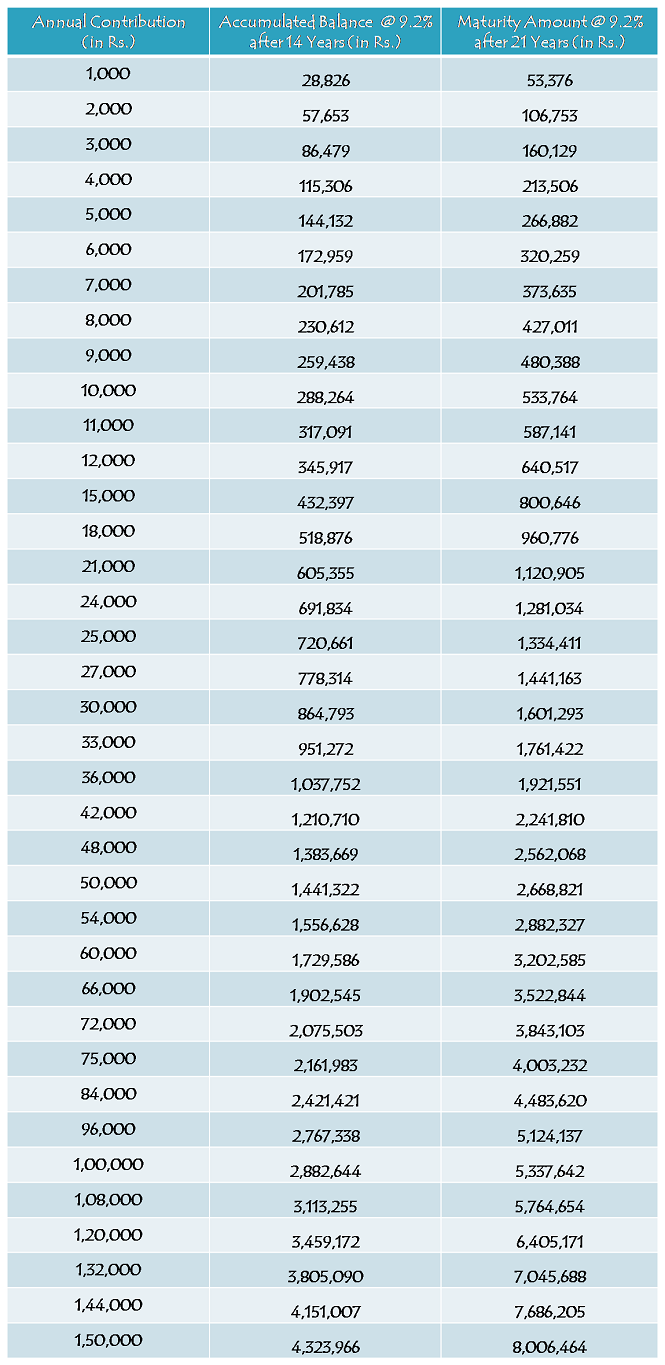

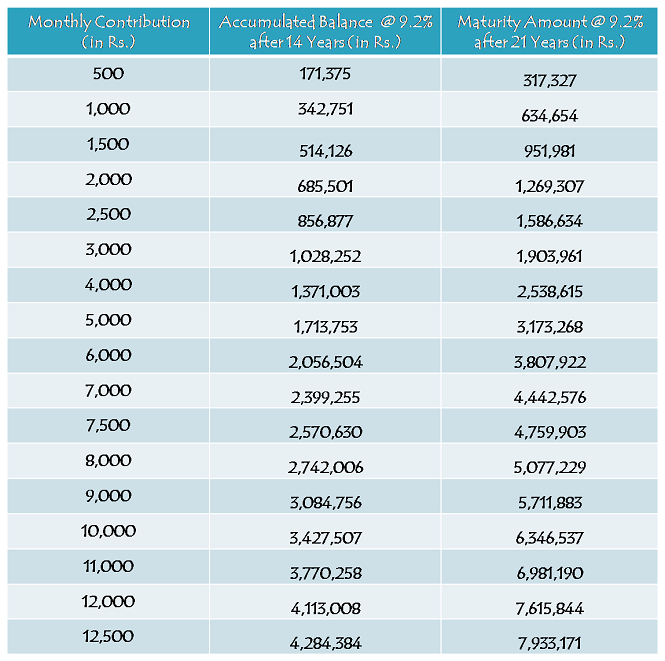

I had posted an article last month in which maturity values were calculated with 9.1% rate of interest throughout its tenure of 21 years. But, as the interest rate has been updated to 9.2% and as most of the investors are yet to open this account, I thought there is a need to have a new post having maturity values calculated as per the new rate of 9.2%.

So, here you have the tables in which maturity values are given as per your annual contributions as well as monthly contributions:

Yearly Contribution Table

Monthly Contribution Table

As different investors will have have different amounts and different timings of their deposits, it is natural that their maturity values will also be different. So, these maturity values are only indicative based on certain assumptions and here you have those assumptions:

* Rate of Interest has been assumed to remain 9.2% for all these 21 years.

* Yearly contributions have been assumed to be made on April 1 every year i.e. the beginning of the financial year.

* Monthly contributions have been assumed to be made on 1st day of every month.

* Although it is not mandatory, a fixed amount of yearly/monthly contribution has been assumed.

* It is also assumed that no withdrawal is made throughout these 21 years.

As people are looking for more and more information about this scheme, I would like to again highlight the main features of this scheme here:

Who can open this account? – Parents or a legal guardian of a girl child up to the age of 10 years, can open this account in the name of the girl child. So, if your daughter is born on or after December 2, 2003, you can get this account opened for her in a post office or an authorised bank branch.

Which documents are required to open this account? – You need birth certificate of the girl child, along with the identity proof, residence proof and two photographs of the parents/legal guardian, to open an account under this scheme. You can approach any post office or a branch of any of the authorised banks to get this account opened.

9.2% Tax-Free Rate of Interest for FY 2015-16 – As mentioned above, this scheme will carry 9.2% rate of interest for the current financial year and it was 9.1% for the previous financial year. Similarly, interest rate will be revised every year in March and will be applicable for the applicable financial year afterwards.

Scheme Matures in 21 years or on Girl’s Marriage, whichever is earlier – The scheme gets matured on completion of 21 years from the date of opening of the account or as the girl child gets married, whichever is earlier. Please note that the girl attaining the age of 21 years has no relevance to maturity period of this scheme.

Deposit for 14 years only – You need to deposit a minimum of Rs. 1,000 and a maximum of Rs. 1,50,000 only for the first 14 years, after which you are not required to deposit any amount. Your account will keep earning the applicable interest rate for the remaining 7 years or till it gets matured on your daughter’s marriage.

NRI/OCI Investment – It is still not clear whether Non-Resident Indians (NRIs) or Overseas Citizens of India (OCI) are allowed to open an account under this scheme or not. But, as it is not allowed with most of the post office small saving schemes, I think the government will not allow them to invest in this scheme either. I’ll update this post as soon as I get any information regarding the same.

Partial Withdrawal – It is allowed to withdraw 50% of the balance for higher education as the girl child attains the age of 18 years. Except for this period, it is not allowed to withdraw any amount during the whole tenure of this scheme.

Nomination Facility – Nomination facility is not there with this scheme. In an unfortunate event of the death of the girl child, the balance amount will be paid to the parents/ legal guardian of the girl child and the account will be closed immediately.

You can check all the features of this scheme from this post – Sukanya Samriddhi Yojana – Tax-Free Small Savings Scheme for a Girl Child

You can also check the updated list of banks and download the application form to open an account from this post – Sukanya Samriddhi Yojana – Updated list of Authorised Banks to Open an Account, Specimen Application Form & Passbook. If you have any query or something related to all these posts, please share it here.

If I pay Rs 12000/- every month & if I discontinue paying after 7-8 years, due to some reasons, What will happen to the my already paid amount for 7-8 years, will it fetch interest @ 9.2%, if the withdraw is on maturity after 21 years of my daughters age.

Hi Amar,

Maturity will not happen when your daughter turns 21. It is 21 years from the account opening date or whenever your daughter gets married, whichever is earlier. If you do not deposit money every year till 14 years, your account will become inactive. However, whether it will earn interest or not, it is still not clear.

Hi sir,

meri ek ladki hai (DOB – 03-03-2015)

me par year ssy me 12000 thousand deposit karuga to 21yer me ladki ko kya maturity milengi aur Kitane saal tak amount deposit karna hoga .

Hi Suraj,

Aapko 14 saal tak amount deposit karna hoga aur maturity pe aapko approximately Rs. 640,517 milenge.

Sir at present my daughter is 7 yrs after 14 yrs she will turn 21.Plz tell me whether she will get the benefit after 14 yrs or on when she gets married say 24 yrs.

Hi Sangeeta,

Your daughter’s account will mature in 21 years from the account opening date (2036) or whenever she gets married (say when she turns 24), whichever is earlier.

Nice scheme

sir

iam one daughter only 2years monthly 1000 rupess wait for 21 years

Dear sir iam Rajkumar, iam interested to join the good scheme but my daughter nearly reached age of15, so pls advise any kind of scheme .

Hi Mr. Rajkumar,

Your daughter is not eligible for this scheme. But, if you can take risks, you can invest in good diversified equity mutual funds.

Can we deposit different amt. in every month for e.g. in this Rs.1000 next I want to deposit Rs.5000.

Yes Rashmi, you can do so. However, it is not compulsory to deposit money on a monthly basis.

sir 18 04 2011 meri betiya ki dob hai , or mera account open hua hai jan 2015 m , meri maturity date 2036 m ho gyi agr meri betiya ki Sahdi 2030 m ho jati hai to mujhe sare paise vapis mil jaye gye or kya rate of interest mila gya with thanks mukesh

Hi Mr. Mukesh,

Agar aapki beti ke shaadi 2030 mein ho jaati hai, to aap balance amount with interest 2030 mein withdraw kar sakte hain.

Sir, I opened sukanya account in post office at my native , now I shifted to city, can I transfer account to any bank in city.

Sir

Mai army mai hu or mane apni bacchi ka account ghar pr khulva rekha hai kya mai uski paymnt apne field post office se kr skta hu kya ya fr all indiaa ke kise bhi post office mai jma kra skte hai kya

Vasudevji, jis post office mein account open hua hai, usi post office mein paise jama karwaane honge.

Meri beti ka DOB 05/09/2004 hai.kya uska SSY Account open ho sakta hai.pls tell me.

Yes Sangeeta, aapki beti is scheme ke liye eligible hai.

Sir yadi parents ko kuch ho jata hai to baki installment ki responsibility kiski hogi indl ya phir post office

Post office ki koi responsibility nahin hogi instalment deposit karne ki. Legal guardian ya aapki beti is scheme ko continue kar sakte hain ya amount withdraw kar sakte hain.

Dear sir,

meri pass 2 ladki he or

ek 5 saal ki or dusri 2 saal inke naam me per month 1000/- jama karta hu

5 saal ki ladki ki saadi me usko 18 saal pure hote hi karne ka plan he

to kya iski saadi par ye sari payment sukanya se mujhe mil jayega ya nahi

Yes Mr. Rajesh, 18 saal poore hone ke baad aap jab bhi apni beti ke shaadi karte hain, tab aap apni jama raashi interest ke saath nikaal sakte hain.

Sir, sir my two girls first 7years old and second 4years old .sir me janana chahata hu ki meri badi daughter ki age after 14 years 7years+14 years-21yeara sir to kya mujhe pura benifeet milega.please inform me.

Hi Mr. Manoj,

Maturity will happen after 21 years from the account opening date or when your daughter gets married, whichever is earlier. Your daughter’s age of 21 years has nothing to do with the maturity of this scheme.

i am nizamuddin A. i am intresting in sukanya samridhi yojana but just i want conform it if after start this scheme payer will death or daughter then how to pay or how to gets please.

Sir,

We have two daughter, one is 6 years old and other is 2 years old

1. If we deposit Rs. 1000 per year for first daughter for 14 years. At that time my daugher will become 20(14+6) years old and we will wait only for 1 year.

2. If we deposit Rs. 1000 per year for second daughter for 14 years. At that time my daugher will become 16 (14+2) years old and we will wait for 5 year.

We just connfirm, What is the deference b/w first and second daugher’s amount at the age of 21 years and Remaining 1 year for first daugher and 5 years for second are interestable or not.

Please reply as soon as possible.

Thanks,

Vijay Kumar

Hi Mr. Vijay,

Maturity will happen after 21 years from the account opening date and not when your daughters turn 21.

Sir, very sorry to say that maturity will be at the age 21 years of child, not 21 years from the date of account opening.

If child age is 6 years, then deposite period will be 14-6, that is only 8 year, after that total amount will be treated as FD amount for next 7 years. Finally at the age 21 years of child the policy become mature.

Sir,

yadi main 14 yrs tak installment pay nahi kar paya to mujhe kis intrest rate se paisa wapas milega aur kab milega

Hi Shailendra,

14 saal agar aap paise jama nahin karenge to account inactive ho jaayega.

When contributing 1000 per yr how is the figure coming to 28000 it would be 14*1000=14000.the interest will be calculated after v pay for 14 yrs I.e from 14 to 21 yrs not from the first yr of payment …..if im not right please let me know I have the post office image which does not match with ur figures

Hi Swapna,

Your deposited amount will start earning interest from the day/month you make your first contribution.

HI,

The date of birth of my daughter is 17th April 2014. Is she eligible under Sukanya Samriddhi Yojana ?

regards

Sukanta

Yes Sukanta, your daughter is eligible for this scheme.

Is shukanya samriti yojna maturity amount tax free?

Yes Sunil, maturity amount you get in Sukanya Samriddhi Yojana would be tax-free under section 10(11A) of the Income Tax Act, 1961.

hi sir

mai ssy a/c pnb mai open krna chahta hoon. post office or bank k benifit mai koi anter hai.pls advise

montly 1000 to kitna paisa maiximum jama kr sakte hai pls reply

Hi Suman,

Bank ya post office, is scheme ke benefits mein koi difference nahin hai. Ek saal mein maximum Rs. 1.50 lakh jama karwa sakte hain.