This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

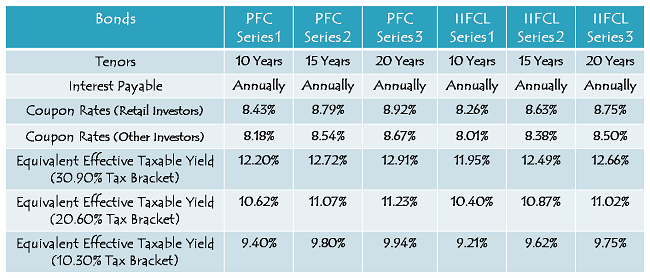

‘AAA’ rated REC issue offered 8.71% to its investors, ‘AA+’ rated HUDCO issue fixed it at 8.76% and then ‘AAA’ rated IIFCL issue managed to cross REC’s peak rate of interest with 8.75%, but now it is the turn of Power Finance Corporation (PFC) to surpass all previous rates to set this year’s highest interest rate on its tax-free bonds by offering 8.92% for a 20-year duration.

PFC would be the fourth company to launch its public issue of tax free bonds this year from Monday i.e. October 14th. The issue would run till fifth Monday i.e. November 11th. But, the company may extend it or preclose it, depending on the investors’ response to the issue.

Interest rates offered by PFC are the highest rates for all three tenors. PFC has set its coupon rates at 8.92% per annum for 20 years, 8.79% per annum for 15 years and 8.43% per annum for 10 years. This jump is due to a rise in the benchmark G-Sec rates in the last 10-15 trading days, after the Repo Rate hike by the RBI.

Size of the Issue – PFC has been authorised to raise Rs. 5,000 crore from tax-free bonds this financial year, out of which it has already raised Rs. 1,124.10 crore through a private placement on August 30th. The company plans to raise the remaining 3,875.90 crore from this issue, with the base issue size of Rs. 750 crore and the green-shoe option of Rs. 3,125.90 crore.

Like REC, if this issue gets subscribed to the tune of Rs. 3,875.90 crore, it will be the last issue of PFC this financial year.

Green Signal for NRIs – After IIFCL not allowing NRIs and QFIs to invest in its issue, PFC has decided not to do that. NRIs, on repatriation basis and on non-repatriation basis, are eligible to invest in this issue. Qualified Foreign Investors (QFIs) are also eligible to participate in this issue.

No Lock-in Period – Many people have been asking me about the lock-in period of these tax-free bond issues, but I don’t know how I missed to mention it here in all my previous posts that there is no lock-in period with these tax-free bonds. If you subscribe to these bonds in demat form, you can sell them anytime you want after their listing on the stock exchange.

These are not tax saving bonds, like 80CCF Infrastructure Bonds or 54EC Capital Gain Tax Saving Bonds, which carry a lock-in period of five years and three years respectively.

Listing – PFC will get these bonds listed only on the Bombay Stock Exchange (BSE). Investors can apply for these bonds either in demat form or in physical form, as per their choice. The company will get the bonds allotted and listed within 12 working days from the issue closing date.

Rating of the issue – Three credit rating agencies, CRISIL, ICRA and CARE have rated this issue and all of them have rated it as ‘AAA’, which is their highest rating to any debt issue. Also, these bonds are ‘Secured’ in nature against certain assets of the company.

Categories of Investors & Allocation Ratio – The investors again have been classified in the following four categories and each category has certain percentage of the issue reserved for the allotment:

- Category I – Qualified Institutional Bidders – 15% of the issue is reserved

- Category II – Non-Institutional Investors – 20% of the issue is reserved

- Category III – High Networth Individuals including HUFs, NRIs & QFIs – 25% of the issue reserved

- Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue reserved

Minimum & Maximum Investment – There is no change in the minimum investment requirement of Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest on Application Money & Refund – PFC will pay interest to the successful allottees on their application money at the applicable coupon rates, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Factors favouring investment in this PFC Issue…

* Highest Coupon Rates – Thanks to a sudden spike in the G-Sec yields in the last 10-12 trading days since the RBI raised the Repo Rate in its monetary policy of September 20th, PFC has been to offer the highest interest rates of the current financial year. I think with 8.92% or 8.79% tax-free rates, investors in the 30% or 20% tax brackets would not even think of going for a bank FD @ 9%.

* RBI cutting the MSF Rate – RBI has cut the MSF Rate by 50 basis points to 9% a couple of days back. The idea was to reduce liquidity crunch in the banking system and help banks in reducing their cost of overnight (very short-term) borrowings and also normalize the yield curve. This move makes market participants believe that the RBI will try to cap the rise in overall interest rates as much as possible.

* Fall in G-Sec Yield – As a result of the RBI’s move to cut the MSF Rate, the 10-year G-Sec yield has fallen from 8.68% to 8.46% in the last couple of days. If this fall is not temporary and continues for a little longer time, you would see a fall in the coupon rates of the upcoming tax-free bond issues.

* Postponement of QE3 Tapering & US Shutdown – US Federal Reserve’s decision to postpone QE3 tapering and a partial shutdown in the US have resulted in a fall in the 10-year bond yield there from 3%+ to 2.64% today. This should also keep the sentiment somewhat healthy here in the Indian bond market.

* Steep fall in September Trade Deficit – With a fall in gold & oil imports and a surge in exports, the Ministry of Commerce today announced a steep fall in our September trade deficit. The problem, which was becoming too burdensome for our economy, is finally getting controlled. This should strengthen the value of Indian rupee against the US dollar in the coming days and the bond yield should also move lower.

Factors against this PFC Issue – Though there are not many factors which come to my mind against this issue, but overall things are not very bright for the power financing sector here in India. PFC, REC and PTC India Financial Services are some of the companies which have been struggling to get their money back which they have been lending to the state electricity boards (SEBs) over the years.

These kind of events have resulted in its share price falling from Rs. 350+ during 2010-11 to below Rs. 100 this year and I think stock price performance is a good barometer to check a company’s current financial health and future prospects. So, this is one thing which you should consider before investing your money in this issue.

With PFC offering relatively higher interest rates and NHPC issue hitting the market only in the third week, I would prefer to invest my money in this issue as compared to HUDCO and IIFCL issues. With so many positives and a possible fall in inflation & interest rates, I think PFC’s rates would be the highest coupon rates offered by any ‘AAA’ rated issuer this financial year.

Application Form of PFC Tax Free Bonds

As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in PFC tax-free bonds, you can contact me at +919811797407