This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

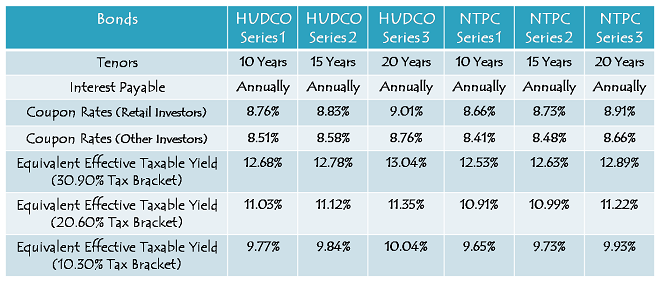

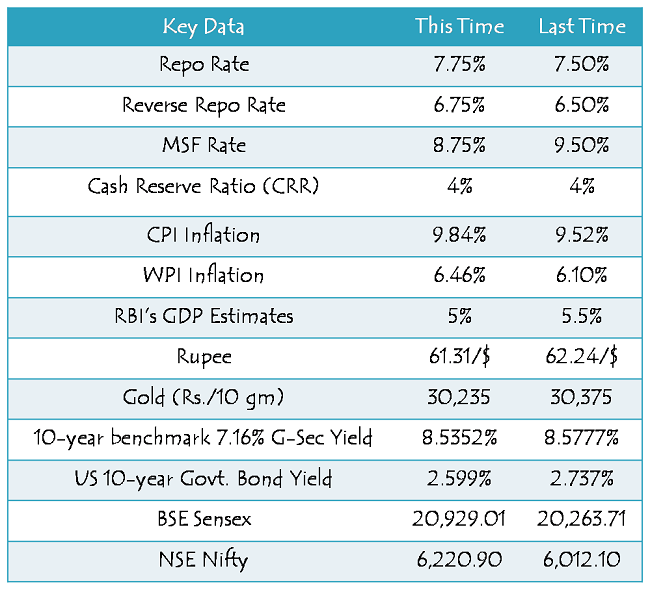

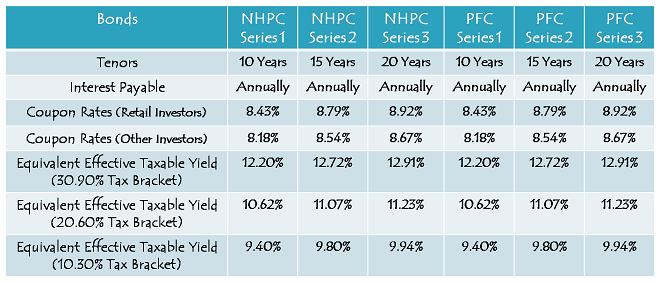

After a month long break, tax free bond issues are back and the 10-year options are looking much healthier now carrying annual coupon rates of 8.76% and 8.66% for ‘AA+’ rated HUDCO issue and ‘AAA’ rated NTPC issue respectively, as against its previous highs of 8.43% for ‘AAA’ rated PFC & NHPC issues and 8.39% for ‘AA+’ rated HUDCO issue.

While this jump has come due to a consistent rise in the yield of the benchmark 7.16% 10-year government bond, the coupon rates with 15-year option and 20-year option have been the highest ever with the HUDCO issue as it is rated ‘AA+’ and carries a leverage of 10 basis points (or 0.10% per annum). I’ll cover the HUDCO issue today and the NTPC issue tomorrow.

HUDCO is launching the second tranche of its tax free bonds from Monday, December 2nd and it will be the first ever tax free bond issue to cross the psychological mark of 9% coupon rate.

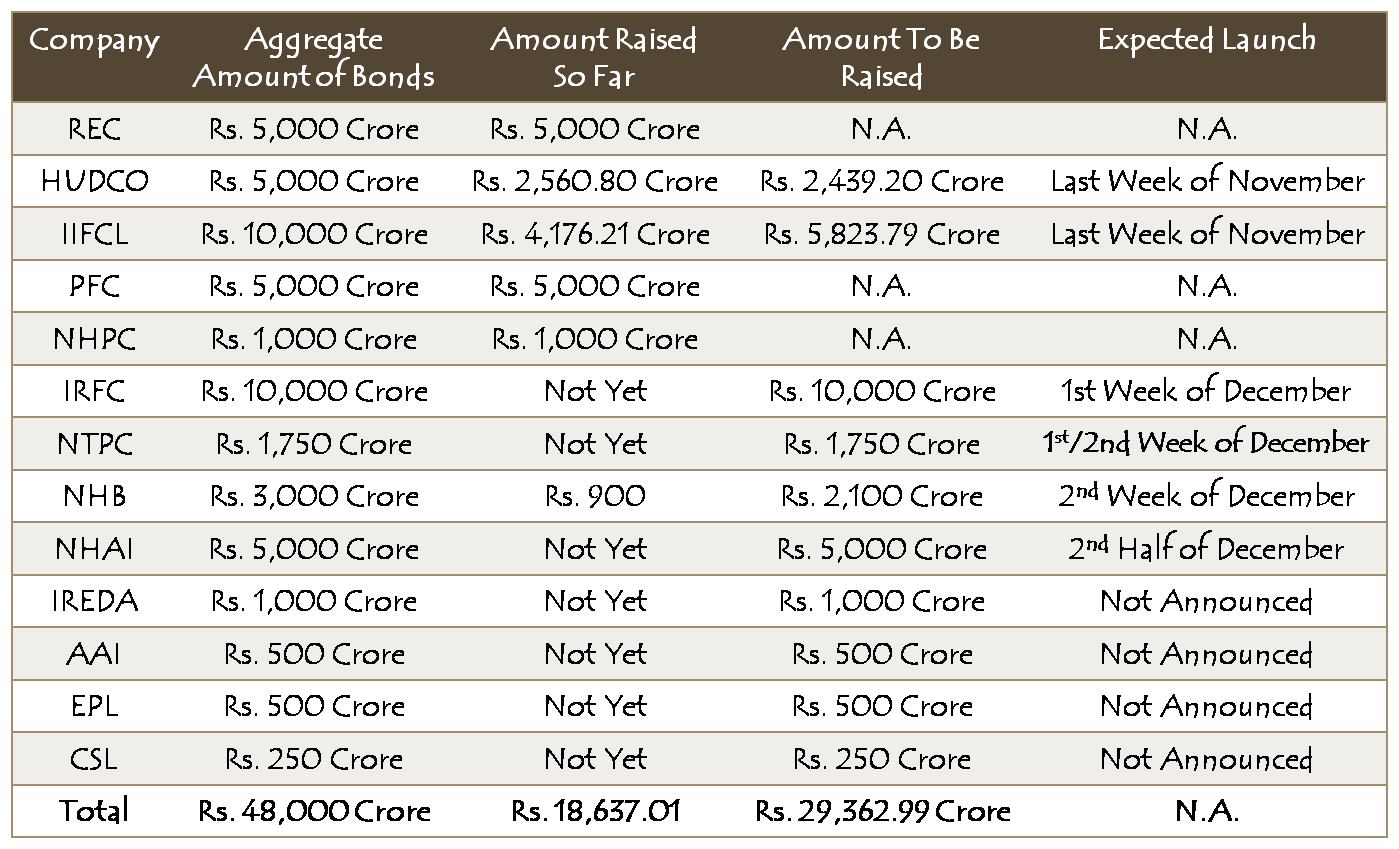

Size of the Issue – HUDCO has set the base issue size at Rs. 500 crore with an option to retain oversubscription up to Rs. 2,439.20 crore. The company has already raised Rs. 2,560.80 crore in its first tranche and through a private placement. I think this issue is attractive enough for it to become the last issue from HUDCO’s stable.

Rating of the Issue – Like Tranche I, this issue has also been rated ‘AA+’. CARE and India Ratings are the two companies which have passed their opinion to assign this rating to the current issue.

Again, the bonds are ‘Secured’ in nature as certain receivables of the company will be charged to the extent of amount to be mobilized under the issue. Also, as HUDCO is wholly-owned by the government of India, I would consider the investors’ investments to be comfortably safe in the issue.

OK to NRI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible.

Investor Categories & Allocation Ratio – As always, the investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved for the allocation:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 30% of the issue is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue is reserved

First Come First Served Allotment – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing – Bombay Stock Exchange (BSE) is the only exchange on which these bonds will get listed and the exchange has given its in-principle listing approval to the bonds issued under this tranche. As with all the recent issues, these bonds also will get allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Investors can apply for these bonds either in physical form or in demat form, as per their comfort and requirement.

No Lock-In Period – These bonds are offering good rate of interest which is tax-free also under Indian taxation laws. As your investment does not provide any tax deduction, there isn’t any lock-in period with these bonds. As these bonds get listed on the BSE, you may sell them whenever you want at the market price.

Interest on Application Money & Refund – HUDCO is the only company which pays the same rate of interest as the applicable coupon rate is on the application money as well as on the money due for a refund. So, with the 20-year option, you’ll get 9.01% as the rate of interest on your application money as well as the refund amount.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest Payment Date – HUDCO has not announced the interest payment date of this issue as yet. I will update this post as and when it gets announced at the time of listing.

While it will be a bonanza for the fixed income investors, I’ll consider this to be a bad situation for the commercial banks, the government and the borrowers. Let’s check how.

Many people have been breaking their fixed deposits to invest in these tax free bonds. It is putting a lot of pressure on the banks to either hike their deposit rates or increase premature withdrawal charges.

As the money is moving out of taxable instruments like fixed deposits, post office schemes etc., the government is also losing out a big amount in tax revenues.

Higher rate of interest will force banks to hike their lending rates also in order to maintain their net interest margins (NIMs) and this outcome will put an additional burden on the borrowers.

With a huge difference between the 10-year interest rate and the 20-year or 15-year rates, I used to prefer the 20-year or 15-year options earlier. But, as the difference has narrowed down considerably, the 10-year option has also become quite attractive now. However, I still prefer the longer duration options as I think it is better to stay invested with longer duration bonds when the interest rates get higher.

Though the issue is scheduled to get closed on January 10, 2014, I really doubt that it would continue that long. I expect it to get closed earlier than that given other companies don’t offer a similar or higher rate of interest.

With coupon rate crossing 9% now on these tax free bonds, there is no reason for the investors to ignore such high rate of interest and keep investing their fresh money into fixed deposits or keep their money invested in it.

Application Form of HUDCO Tax Free Bonds

HUDCO Tax-Free Bonds – Bidding Centres

HUDCO Tax Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in HUDCO tax-free bonds, you can contact me at +919811797407

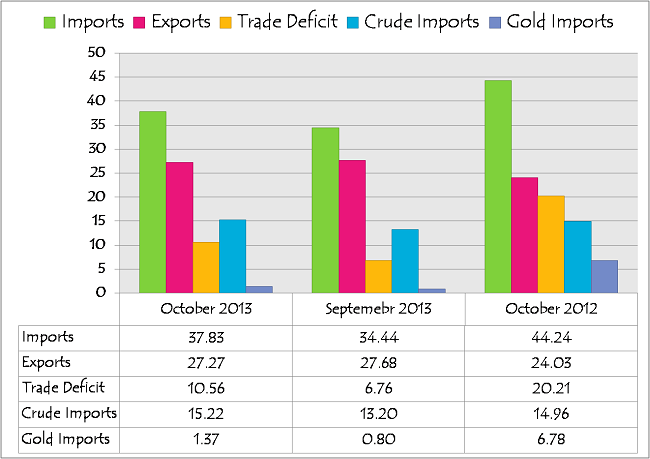

(Note: Figures are in US $ billion)

(Note: Figures are in US $ billion)

18.1 km/L 105bhp 7-speed(A) DSG

18.1 km/L 105bhp 7-speed(A) DSG

{kind=link}